Windfall Revenues and the Eastern Caribbean Challenge

Commentary

Windfalls, Volatility, and the Policy Dilemma

What should governments do when windfall revenues surge beyond their expectations, but cannot be relied upon to persist? Do they expand spending in real time, or treat these inflows as temporary and uncertain? This tension sits at the centre of fiscal policy, especially for small, open economies where external shocks are amplified and buffers are limited.

Windfall revenues, whether derived from commodities, financial flows, or non-traditional sources, often create a misleading sense of fiscal space. During upswings, government expenditure tends to expand while fiscal positions temporarily appear strengthened due to the windfall revenue. However, when these inflows moderate, the adjustment is rarely gradual. Instead, it manifests through widening deficits, increased borrowing, and heightened macroeconomic volatility.

The issue is not the windfall itself, but how it is managed. Thus, institutional design becomes critical. Well-calibrated fiscal frameworks tend to play an integral role in insulating budgets from volatile revenue streams and limiting procyclical policy responses. Without such mechanisms, temporary gains risk translating into permanent vulnerabilities.

It is within this context that Sovereign Wealth Funds (SWFs) have emerged as a central policy tool. At their core these frameworks are designed to separate volatile revenues from recurrent expenditure, allowing governments to smooth spending, accumulate financial assets, and strengthen macroeconomic stability over time. A SWF is a state-owned investment vehicle that manages financial assets derived from exceptional or non-recurring revenues. These revenues may originate from commodity exports, privatisation, balance of payment surpluses, or other windfall sources.

Global Concentration and Institutional Design

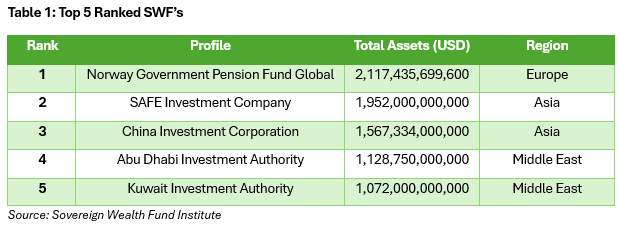

SWFs are highly concentrated across a few regions, particularly Europe, Asia and the Middle East, reflecting the accumulation of sustained external surpluses. According to the Sovereign Wealth Fund Institute, Europe leads the global ranking through the Norwegian Government Pension Fund Global (GPFG), which stands as the largest SWF worldwide, with assets exceeding USD2.1 trillion (Table 1). This is followed closely by Asia, where China’s SAFE Investment Company and China Investment Corporation collectively account for a significant share of global sovereign assets, supported by persistent current account surpluses and reserve accumulation strategies. The Middle East also features prominently with funds such as the Abu Dhabi Investment Authority, and the Kuwait Investment Authority, largely financed by hydrocarbon revenues.

The regional distribution highlights a key point. While the sources of inflows differ, ranging from oil revenues in the Middle East to export-driven surpluses in Asia, the accumulation of sovereign wealth ultimately depends on the ability to sustain these inflows and manage them within a coherent institutional framework.

The Norwegian Model

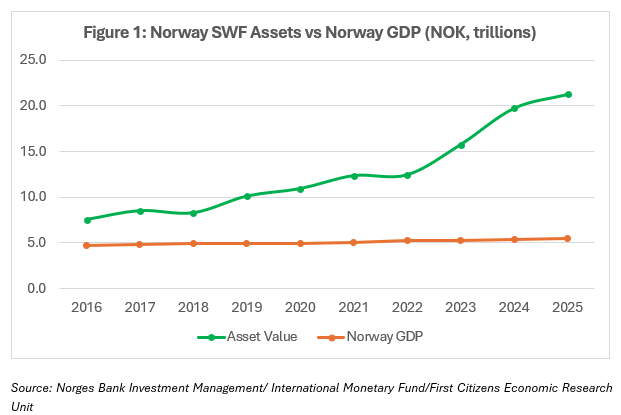

The Norwegian model remains particularly instructive. According to the Norges Bank Investment Management, the fund value for 2025 stood at approximately NOK21.3 trillion (approx. USD2.2 trillion), the fund exceeds almost four times Norway’s GDP as at 2025 (Figure 1), illustrating the scale at which resource revenues have been transformed into financial wealth. This outcome reflects institutional design rather than revenue size alone. Petroleum revenues are channelled into the fund and invested externally, while fiscal withdrawals are governed by a rules-based framework linked to expected long-term returns limiting the transmission of commodity price and volatility into the domestic economy.

The fund’s asset value has followed a sustained upward trend between 2016 and 2025, despite periods of global financial volatility. This reflects a combination of continued inflows and investment performance, but more importantly, adherence to a disciplined fiscal framework. The Norwegian case demonstrates that while windfalls create opportunity, it is institutional structure that determines whether these inflows translate into long-term macroeconomic resilience.

CBI Volatility and the Case for a Regional Savings Mechanism

Given this context, can a SWF be meaningfully applied to economies whose windfalls are not generated by oil, but by the sale of citizenship rights? This question is specifically relevant for the Eastern Caribbean Currency Union (ECCU), where five member states currently operate Citizenship-by Investment (CBI) programmes: Antigua and Barbuda (A&B), Dominica, Grenada, St. Kitts and Nevis (SKN), and St. Lucia (SLU).

CBI programmes allow foreign investors to obtain citizenship in exchange for qualifying investments, typically though direct government contributions, approved real estate, or other designated development projects. For small economies, with narrow tax bases and high exposure to external shocks, these programmes have become an important source of non-tax revenue. However, they also introduce a policy dilemma: the revenues are large enough to shape fiscal outcomes, but too volatile to be treated as permanent income.

The Scale of the CBI Issue

According to the IMF, CBI revenues across ECCU jurisdictions averaged approximately 6.5% of GDP between 2019 and 2023, rising to nearly one-third of total non-grant government revenue in 2023. At the aggregate level, estimates suggest total inflows were equivalent to around one-fifth of the ECCU’s GDP, highlighting the extent to which these programmes have become embedded in fiscal frameworks.

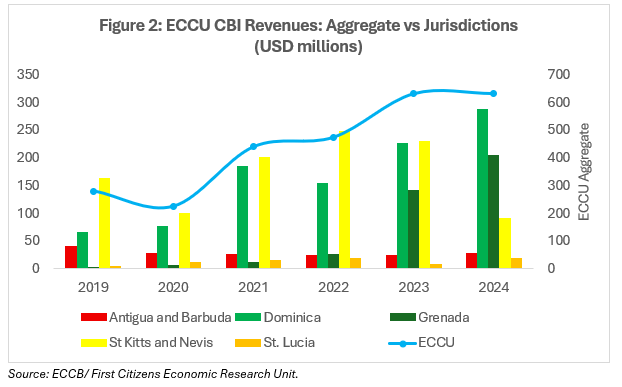

Data from the Eastern Caribbean Central Bank (ECCB) indicate that total CBI receipts reached approximately XCD1.7 billion (USD632.1million) in 2024, however, aggregate figures obscure the underlying volatility.

While total ECCU CBI inflows exhibit a broadly upward trend over the period 2019-2024 (Figure 2), this masks significant divergence at the country level. SKN and Dominica account for a substantial share of total inflows, with pronounced surges in 2021-2023 followed by visible moderation. Grenada’s inflows display a sharp acceleration post-2021, while A&B remains comparatively stable but at lower levels relative to its peers. SLU, while a later entrant, has maintained comparatively modest CBI inflows relative to its regional peers, reflecting a smaller programme scale and more limited fiscal reliance.

Structural Limitations of Current CBI Frameworks

This variation emphasizes a deeper structural issue. While CBI programmes generate substantial inflows, the frameworks through which these revenues are managed remain primarily development-oriented rather than stabilisation-focused. Across the ECCU, governments have established designated funds to receive and allocate CBI proceeds, including Grenada’s National Transformation Fund (NTF), Dominica’s Economic Diversification Fund (EDF), St. Lucia’s National Economic Fund (NEF), Antigua and Barbuda’s National Development Fund (NDF), and St. Kitts and Nevis’ Sustainable Island State Contribution (SISC)

These mechanisms play an important developmental role. They channel foreign capital directly into priority areas such as infrastructure, healthcare, education, tourism, and renewable energy. For instance, contributions to Grenada’s NTF, currently set at a minimum of approximately USD235,000 per applicant, are directed toward public investment projects, supporting tangible improvements in economic capacity.

However, from a macro-fiscal perspective, these funds differ fundamentally from SWFs. Development funds are designed to spend inflows, often within relatively short time horizons. SWFs, by contrast, are designed to invest and preserve capital, generating returns over time and smoothing fiscal outcomes across economic cycles. The distinction is critical. When CBI revenues are fully absorbed into current or near-term expenditure, the fiscal system remains exposed to abrupt declines in inflows. In effect, the entire windfall is consumed rather than partially transformed into a financial buffer.

Volatility, Pro-Cyclicality, and Fiscal Risk

The volatility of CBI revenues reinforces this vulnerability. Application volumes are highly sensitive to geopolitical developments, regulatory scrutiny in source markets, due diligence requirements, and competition across jurisdictions. The tightening of European Union oversight, alongside harmonisation efforts among ECCU programmes, including minimum pricing agreements and proposals for a regional regulator, has already contributed to fluctuations in demand.

This introduces a procyclical dynamic into fiscal policy. During periods of strong inflows, governments may expand capital expenditure or increase recurrent spending, supported by elevated revenues. However, when application volumes decline, as observed in recent years in several jurisdictions, fiscal balances weaken, and financing gaps emerge. Without pre-existing buffers, adjustment tends to occur through increased borrowing, delayed investment, or expenditure compression, amplifying macroeconomic volatility.

This is particularly relevant given existing fiscal constraints. Public debt levels across several ECCU economies remain elevated, often exceeding the regional benchmark of 60% of GDP, while exposure to natural disasters and climate-related shocks further compounds fiscal risk. In this context, reliance on volatile CBI inflows without a stabilisation mechanism can exacerbate, rather than mitigate, underlying vulnerabilities.

Policy Shifts

Recent policy developments suggest a gradual shift in how these revenues are being conceptualised. In March 2026, SKN passed the Sovereign Wealth and Resilience Fund Bill, becoming the first CBI-based economy in the Caribbean to establish a statutory sovereign wealth-type framework backed by CBI revenues and prospective geothermal energy income.

Similarly, SLU has moved beyond preliminary discussions, with authorities approving the establishment of a SWF financed by CBI proceeds. While still at an early stage of implementation, this represents a clear policy shift toward institutionalising the management of volatile inflows and strengthening fiscal resilience over the medium term.

The Case For A Sovereign Wealth Framework

The case for a sovereign wealth or stabilisation-type fund in the ECCU becomes increasingly compelling. The argument is not that development spending should be curtailed, such investments are critical, but rather that a portion of windfall inflows should be systematically saved and invested.

Even modest allocations can have meaningful effects over time. A framework that channels, for example, 15–25% of annual CBI revenues into a rules-based investment fund could gradually build financial buffers, reduce reliance on borrowing during downturns, and enhance fiscal credibility. Unlike development funds, which are inherently procyclical, a sovereign wealth framework would operate countercyclically, accumulating assets during periods of strong inflows and providing support when revenues weaken.

CBI revenues should be treated as windfall income, rather than a stable source of recurrent financing, to reduce fiscal procyclicality. A rules-based stabilisation mechanism, through a sovereign wealth-type fund could help smooth revenue volatility and build buffers over time. Given the regional nature of these programmes, greater coordination across ECCU jurisdictions would also support more stable and sustainable inflows.

Conclusion

For small, shock-prone economies in the ECCU, the question is unavoidable: when the next downturn in CBI inflows arrives, as it inevitably will, will governments be adjusting in real time, or drawing from buffers built in advance?

CBI programmes have become a material pillar of fiscal performance across the region, yet their volatility introduces clear macroeconomic risks. Without appropriate institutional mechanisms, these inflows can reinforce procyclical policy and expose economies to abrupt adjustment when conditions weaken. While recent policy developments signal a shift toward more structured management, the effectiveness of these frameworks will ultimately depend on their design, discipline, and integration into broader fiscal strategy.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.