When Numbers Miss the Bigger Picture

Commentary

Gross Domestic Product, or GDP, has long been treated as the cornerstone of national economic progress, measuring the total market value of all goods and services produced within a country over a specific period. The concept of GDP was introduced during the Great Depression in 1937, when economist Simon Kuznets presented it to the U.S. Congress as a tool for assessing national output. It was later adopted globally as the standard measure of economic performance, according to the World Economic Forum.

Yet even Kuznets warned that “the welfare of a nation can scarcely be inferred from a measure of national income”. His caution proved prophetic. GDP captures production but not the pollution it creates or the resources it depletes. It records spending and investment but not the quality of life they deliver. It reflects activity, but not necessarily progress.

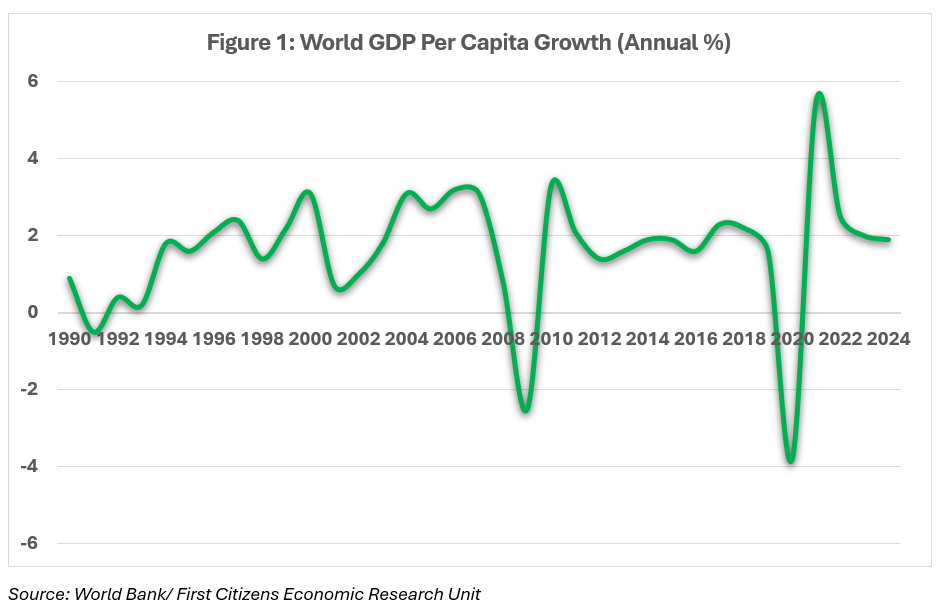

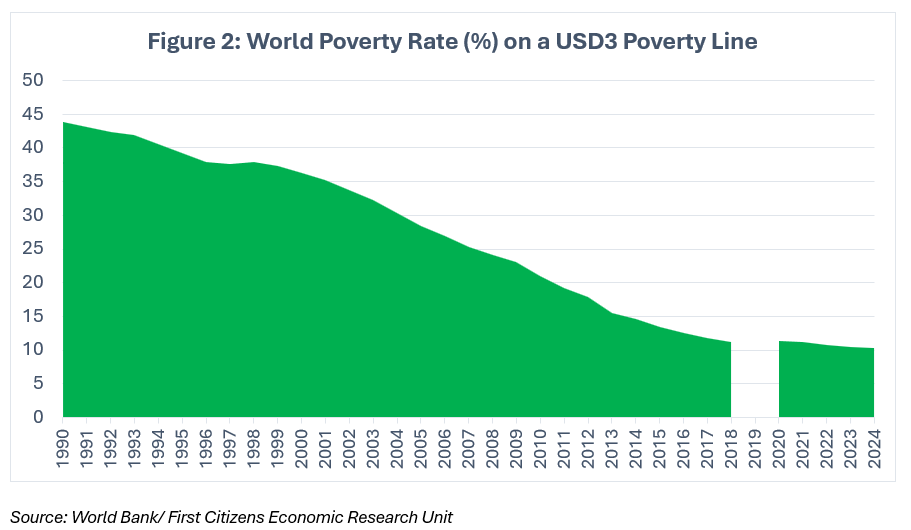

Based on World Bank data, global GDP per capita has more than doubled since 1990 (Figure 1). Yet, as of 2025, an estimated 831mn individuals (10% of the global population) still live in extreme poverty, surviving on less than USD3 per day (Figure 2).

Rising output does not necessarily mean rising welfare. GDP counts the cost of rebuilding after a hurricane as “growth”, but not the homes, lives, or ecosystems lost. It measures the value of oil extracted, but not the depletion of the resource left behind.

Limitations of Gross Domestic Product

Growth that Draws Down Natural Capital

GDP is often seen as a measure of progress, yet it frequently rewards activities that weaken the very foundations of future growth. One of its deepest flaws lies in its inability to distinguish between income earned through sustainable production and income generated by exhausting natural resources. When forests are cleared, minerals extracted, or coral reefs removed to make way for construction, national output rises, but the natural wealth that sustains future prosperity quietly diminishes.

According to the World Bank, global renewable natural capital, i.e. the world’s supply of natural resources that can regenerate if managed responsibly, has declined by more than 20% per capita over the past 25 years. This reflects unsustainable use of forests, fisheries, and other ecosystems that support livelihoods, particularly in developing economies. The World Bank warns that if key ecosystem services such as pollination, carbon storage, and fisheries collapse, the global economy could lose up to USD2.7tn in annual output by 2030, with low-income countries seeing GDP decline by about 10%.

For resource-rich and climate-vulnerable economies, this presents a clear dilemma. In the short term, higher extraction and land conversion can lift GDP and fiscal revenues, while reconstruction following disasters temporarily boosts output. Over time, however, the erosion of natural capital and the cost of repeated rebuilding weaken fiscal resilience and heighten long-term vulnerability to future shocks.

For instance, After Hurricane Maria, Dominica recorded losses of approximately USD1.37bn or 226% of Dominica’s 2016 GDP, according to the Post-Disaster Needs Assessment. Reconstruction raised GDP in the following years, yet the recovery masked deeper damage. The forests, soils, and coastal ecosystems that once protected the island were severely degraded, leaving the economy more vulnerable to the next storm.

Growth that Widens Inequality

According to the Harvard Business Review, GDP does not account for inequality, a limitation that has become more significant as income gaps widen across both advanced and developing economies. In simple terms, GDP measures the size of the pie but not how it is shared. Two countries may report the same level of output, yet in one, growth reaches most citizens, while in the other, prosperity pools at the top.

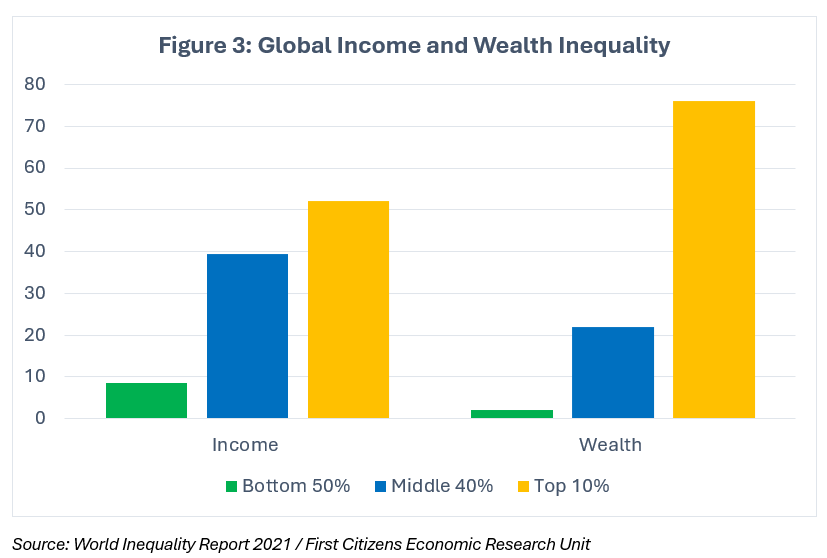

The most recent World Inequality Report, published in 2022, highlights the extent of this divide. The richest 10% of the global population earn more than 52% of total income, while the poorest half share just 8.5% (Figure 3).

As income becomes concentrated among higher earners who tend to save more of their income, growth in overall spending (a key driver of economic growth) diminishes. Over time, inequality can also undermine human capital formation, as lower-income households often have limited access to quality education and health care, slowing productivity and long-term potential output. The result is an economy that looks healthy in aggregate but fragile beneath the surface. Rising inequality undermines social cohesion, complicates policy effectiveness, and increases fiscal pressure when governments resort to subsidies and transfers to ease the gap.

South Africa offers a sobering example. Despite being one of the continent’s most industrialized economies, it remains among the most unequal. According to the World Inequality Database the wealthiest 10% capture about 65% of national income, while unemployment and poverty remain persistently high. Sluggish growth, fiscal strain and corruption have limited the government’s capacity to address these imbalances, deepening social tensions and eroding confidence in the economy.

The Caribbean Perspective: Growth vs. Well-Being

In the Caribbean, GDP growth often tells a story that appears stronger on paper than it feels in everyday life. The numbers suggest a strong recovery from the COVID-19 pandemic, yet many citizens continue to face rising prices, stagnant real wages, and increasing debt burdens.

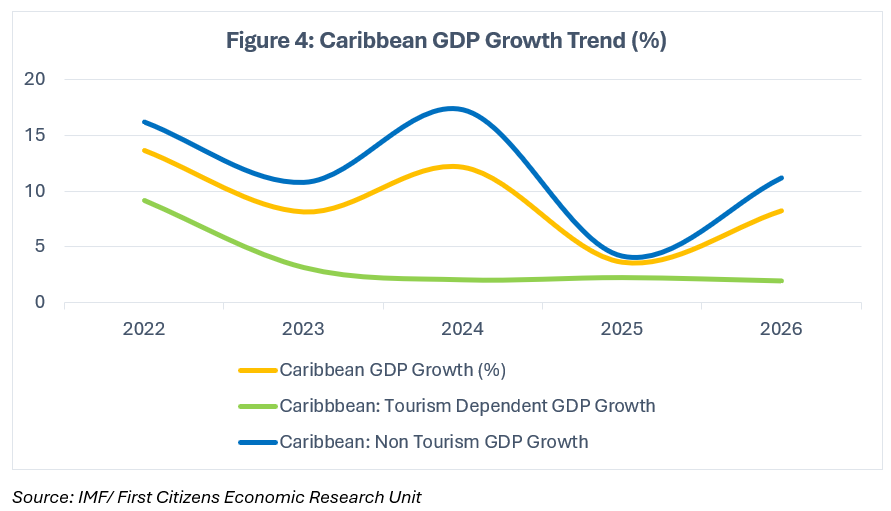

Across the region, recovery has often been cyclical rather than transformative. Tourism-dependent economies record sharp rebounds after crises, e.g. a surge in visitor arrivals following the pandemic, or bursts of reconstruction after hurricanes, but these temporary gains frequently mask underlying fragility. Inflationary pressures, limited fiscal space, and external shocks continue to weigh on household welfare even as GDP expands. According to the IMF’s Western Hemisphere Regional Outlook (October 2025), overall GDP growth in the Caribbean is projected at 3.6% in 2025. However, this average conceals major disparities. Growth among tourism-dependent economies is expected to reach just 2.3%, while non-tourism Caribbean economies are projected to expand by 4.2% in 2025 (Figure 4), a figure heavily influenced by Guyana’s sustained ‘double-digit’ expansion, which significantly elevated the regional growth rate and masks softer outcomes across the rest of the Caribbean

Countries such as Grenada and St Vincent and the Grenadines (SVG) illustrate this dynamic. Both maintained positive growth paths following the disruptions of Hurricane Beryl in 2024, supported by reconstruction activity, tourism recovery, and citizenship-by-investment inflows. Grenada’s GDP growth for 2025 is projected at 4.4%, while SVG is expected around 3.3%, according to the IMF. These figures point to resilience, but they reveal little about inclusiveness, fiscal strain, or the sustainability of recovery.

For small island states repeatedly tested by climate and external shocks, GDP measures the pace of growth, not its quality. True progress depends on whether expansion translates into broader opportunity, social resilience, and sustainable development across the region.

Beyond GDP: Rethinking Progress

If GDP alone cannot capture the full picture of development, the next question is what can. Around the world, policymakers and economists are increasingly seeking complementary measures that reflect not just output, but well-being, resilience, and sustainability.

The Human Development Index (HDI), developed by the United Nations Development Programme (UNDP), measures a country’s overall achievement in three key dimensions of human development: health, education, and income. HDI considers how growth translates into broader improvements in living standards and human potential. According to the UNDP Human Development Report 2023, Costa Rica recorded an HDI value of 0.833, placing it in the Very High Human Development category. Costa Rica, however, is not a low-income economy by regional standards, it already ranks relatively high in Latin America on a per-capita income basis. What distinguishes it is how consistently that income has been channelled into public services and social outcomes, allowing the country to achieve strong human development results.

Alongside this, the World Happiness Report provides a complementary perspective by assessing subjective well-being across countries. Its findings highlight that well-being is influenced not only by income, but also by social support, institutional trust, and economic security. According to the 2026 report, Finland once again ranks as the happiest country globally, while the United States, despite being one of the world’s largest economies, places significantly lower at 23rd. This contrast emphasizes that higher income levels do not automatically translate into improved well-being. Evidence also points to declining life satisfaction among younger populations in advanced economies, further highlighting the growing disconnect between economic performance and lived experience. Together, these insights reinforce the limitations of GDP as a standalone measure of progress.

Other frameworks, such as the Inclusive Wealth Index (IWI) by the United Nations Environment Programme (UNEP), expand the definition of national wealth to include produced, human, and natural capital. The World Bank’s Changing Wealth of Nations similarly tracks the value of these assets to show whether growth today is achieved at the expense of tomorrow’s prosperity.

In the Caribbean, this conversation has already begun. The OECS and UNDP continue to advance Blue and Green Economy frameworks, designed to integrate economic diversification with environmental stewardship and climate resilience. These initiatives represent a step toward a more comprehensive view of progress, one that balances income growth with social inclusion and sustainability.

Redefining What Progress Means

Now let us imagine a different measure of success. One where growth is not judged only by what is produced, but by what endures. Where a rise in output is matched by a rise in opportunity, and where every new dollar of income strengthens the social fabric that holds a nation together.

Imagine a Caribbean where a rebuilt school counts for more than a statistic, and where healthier coastlines, stronger skills, and more resilient communities are treated as the true returns of progress. Inevitably, GDP will always have its place, but it should no longer stand alone. The future belongs to economies that measure not only how fast they grow, but how effectively growth improves people’s lives. When development is judged by lived outcomes rather than headline figures, the region moves closer to a more meaningful and sustainable understanding of progress.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus., offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.