What Investors Need to Know About Trinidad and Tobago’s Asset Levy Era

Commentary

On October 13, 2025, during the National Budget Presentation for 2026, the government announced a major fiscal reform – the introduction of a 0.25% Asset Levy on the assets of commercial banks and insurance companies operating in the country.

Taking effect on January 1, 2026, this new measure is designed to broaden government revenue streams and promote fiscal fairness by drawing contributions from sectors with strong capitalization, solid profitability and resilient balance sheets. Institutions and insurers licensed under the Special Economic Zones (SEZ) Act 2022 will be exempt, in keeping with the government’s commitment to maintain investment incentives within export-oriented and innovation-driven areas.

Unlike traditional profit-based corporate taxes, an asset levy is assessed on the size of an institution’s balance sheet rather than its earnings. This means that large, well-capitalized entities contribute to public finances consistently, regardless of short-term profit fluctuations. The structure promotes more stable revenue flows, strengthens fiscal resilience, and reflects the principle that a company’s economic footprint, not just its profits, defines its responsibility to the broader economy. This approach is already practiced in Jamaica and Barbados and have demonstrated how such levies can support fiscal sustainability while encouraging shared responsibility between government and the financial sector.

Asset Levies in the Caribbean

In Barbados, the government applies an asset-based levy on the financial sector that reflects its commitment to fair and balanced fiscal policy. Under the Bank (Tax on Assets) Act, 2017, all deposit-taking institutions, specifically commercial banks, must pay a 0.35% annual tax on their average domestic assets. These assets refer to holdings within Barbados or those denominated in the local currency, distinguishing them from foreign or offshore assets. Credit unions are exempt from this tax.

The levy is prorated and collected quarterly, providing a steady stream of government revenue and reducing fluctuations across reporting periods. Insurance companies are also subject to the same 0.35% rate, though calculated on their total assets minus “segregated assets.” These segregated assets represent reserves set aside for policyholder liabilities or reinsurance recoverables, meaning only the company’s own capital base is taxed.

In Jamaica, a similar ad valorem (value-based) asset tax applies to the financial sector at a rate of 0.125% of the taxable assets reported on balance sheets. This includes loans, investments and other financial instruments, before deducting liabilities. The levy covers banks, merchant banks, and building societies regulated by the Bank of Jamaica, as well as securities dealers and insurance companies under the oversight of the Financial Services Commission (FSC). Since its inception, it has undergone several adjustments. Initially introduced in 2012 as part of Jamaica’s IMF-supported fiscal reform programme, the asset tax was first set at 0.14%, increased to 0.25% in 2014, and later reduced to 0.125% in 2021.

Investor and Market Implications

The introduction of this new tax could temporarily weigh on the profitability of banks and insurance companies, particularly in the short term. While legislation is being set that will define “assets”, the levy may apply to the entire balance sheet, including loans, investments, and securities, regardless of how well these assets perform. As these institutions are already subject to corporate income tax, the additional levy may further reduce net earnings.

With lower profits, dividend payments may also come under pressure. Banks and insurers have historically maintained high dividend payout ratios. A decline in profitability could therefore result in lower distributable income or prompt boards to adopt more conservative dividend policies to preserve capital buffers, particularly in line with Basel III liquidity and leverage standards.

Given these dynamics, investors may see short-term volatility in Trinidad & Tobago Stock Exchange (TTSE) listed banking stocks, as the stock prices may fall in response to tighter margins, reduced dividends and uncertainty around the levy’s full impact. Trinidad and Tobago’s financial stocks are traditionally valued for their dividend stability and consistent returns on equity, so any fiscal measure that alters these expectations tends to trigger valuation adjustments. Investors typically revise earnings forecasts downward, leading to modest declines in share prices in the near term.

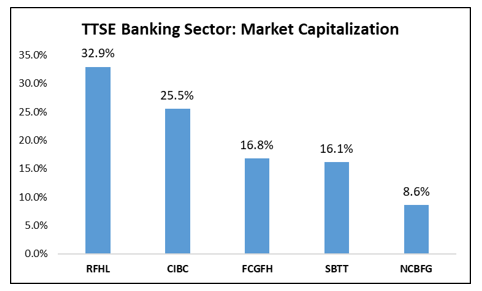

Figure 1: TTSE Sector Market Capitalization

Source: TTSE

In addition, given that the TTSE Composite Index is heavily weighted toward banks and insurers, the market could experience a temporary dip as portfolio managers rebalance toward defensive or non-financial holdings, pending further government clarity on deductibility rules and exemptions.

However, this reaction is expected to be short-lived rather than structural. Once investors quantify the likely impact and as institutions implement cost recovery strategies such as modest fee adjustments or expense rationalization, market stability should return.

Experience in Jamaica and Barbados supports this outlook. Both markets saw initial dips in bank valuations following similar asset levies, followed by a gradual rebound as investors gained confidence in the sector’s ability to absorb the cost without undermining capital strength or dividend continuity.

Figure 2: Banking Sector Market Capitalization

Source: TTSE

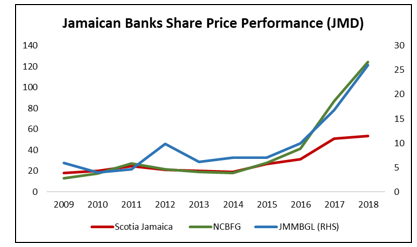

Figure 3: Jamaican Bank Stocks

Source: SCJ, NCBFG and JMMBGL Annual Reports

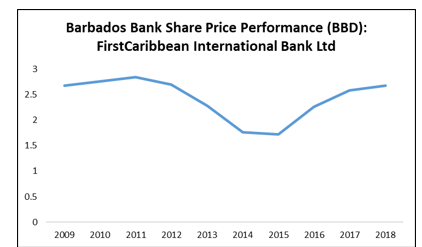

Figure 4: Barbados Bank

Source: CIBC Annual Reports

Future Outlook

Over the next fiscal cycle, policymakers are expected to focus on integrating the levy into a broader tax modernization framework that includes National Insurance System (NIS) reform, a Landlord Business Surcharge and the launch of a Real Estate Investment Trust (REIT) listed on the TTSE.

The Bankers Association of Trinidad and Tobago (BATT) is currently working with the Ministry of Finance to refine these technical details, including the definition of “assets”, whether the levy will be deductible against corporate income tax and whether the measure will include tiered rates or thresholds to protect smaller institutions. Draft regulations are expected to be presented to Parliament by late Q4 2025, followed by detailed guidelines from the Board of Inland Revenue (BIR) on valuation methods and audit procedures for financial statements prepared after January 1, 2026.

In the medium-term, policymakers plan to review the levy after its first year, guided by the Financial Oversight and Appropriations Committee, which monitors tax efficiency and expenditure performance. If the measure delivers stable and predictable revenues, it may evolve into a permanent fiscal instrument, similar to Jamaica’s long-standing asset tax.

For investors, in the short term, modest effects on profitability, dividend yields, and valuation multiples for listed banks and insurers are likely, as markets price in the higher cost structure. However, these shifts are expected to be temporary, as the domestic financial sector remains highly capitalized, liquid and resilient.

Ultimately, while the Asset Levy introduces a new cost element for the financial sector, it does not alter the long-term investment case for Trinidad and Tobago. The nation’s banks and insurers continue to demonstrate strong liquidity, high capital adequacy and reliable dividend performance, supported by digital innovation, regional growth and ongoing capital market development. For long-term investors, any short-term volatility surrounding the levy’s rollout may therefore present selective buying opportunities, particularly among financial institutions with robust fundamentals and disciplined governance.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.