Unlocking Tobago’s Tourism Potential through the Stopover Strategy

Commentary

Introduction:

Few regions worldwide have transformed natural beauty into economic value as successfully as the Caribbean. Across the region, tourism built around sun, sea and sand has generated substantial foreign exchange earnings and supported long-term economic development. Yet, despite possessing some of the Caribbean’s most unique natural attractions, including the Nylon Pool, rich biodiversity and strong eco-tourism potential, for decades Tobago has struggled to fully convert these advantages to achieve sustainable tourism growth and to compete internationally. The island remains comparatively underleveraged within the regional tourism market. Limited strategic focus, inconsistent investment and weak international positioning have prevented Tobago from fully capitalizing on its significant tourism potential.

For decades, Trinidad and Tobago’s (T&T) development trajectory has been uneven, with national policy and investment priorities disproportionately concentrated in Trinidad, while Tobago’s tourism-driven potential has remained largely underutilized. In years following independence, policymakers identified a critical structural vulnerability – the economy’s heavy dependence on oil and gas, which was widely recognized as unsustainable in the long term.

In response, the T&T Development Programme (1969-1973) positioned tourism as a central pillar of economic diversification, intended to reduce reliance on hydrocarbons and expand foreign exchange earnings. More than fifty years after this plan was conceived, this diversification objective remains only partially achieved. As T&T approaches its 64th year of Independence, the gap between early policy intent and current economic structure remains evident. Against this backdrop, renewed strategic focus on Tobago’s tourism sector presents an opportunity to address longstanding imbalances and advance a more diversified economic model.

The Case for Tourism

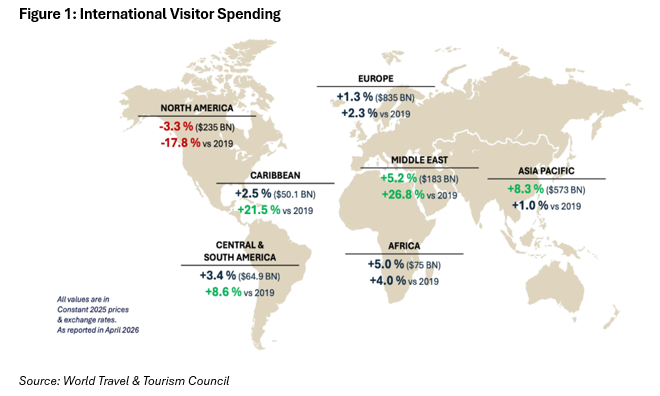

Travel and tourism remain one of the world’s most lucrative industries, contributing significantly to global economic activity. According to the World Travel and Tourism Council (WTTC), the sector contributed approximately USD11.6 trillion to global GDP in 2025, representing an annual growth of 4.1%, outpacing overall global economic growth of 3.4%. Within the Caribbean, tourism plays an even more dominant role, accounting for over 30% of GDP across several economies and generating an estimated USD50.1 billion in tourism-related activity. In comparison, tourism’s contribution to GDP in T&T remains modest, highlighting the country’s underexploited potential within a high-growth global industry.

Tobago’s Crossroads

Tobago possesses many of the core attributes required of a world-class tourism destination, but the sector continues to underperform. This underperformance is particularly evident when viewed against global tourism trends. International tourism has now fully rebounded to pre-pandemic levels, with the United Nations World Tourism Organization (UNWTO) estimating that global tourist arrivals reached approximately 1.52 billion in 2025 representing a 4.0% increase over 2024 and surpassing the 1.5 billion recorded in 2019. This marks the full recovery of the global tourism industry, with record high travel demand. However, Tobago has not fully benefited from this global resurgence as the island continues to suffer debilitating constraints.

Limited airlift connectivity remains one of Tobago’s major hindrances. The dependence on a narrow range of international flight routes continues to restrict accessibility from its key source markets, including the United States, Canada and Europe. High airfare cost and limited direct connectivity reduce the island’s competitiveness relative to regional destinations such as Jamaica, Barbados and the Dominican Republic, which have actively expanded airline partnerships and route network. At present, Tobago’s direct services include flights from London Gatwick and New York’s John F. Kennedy International Airport. Travellers from other major US cities, including Miami, Fort Lauderdale and Houston are required to transit through Trinidad before continuing to Tobago. Canada, meanwhile, has no direct air service to the island. In contrast, destinations such as Barbados benefit from multiple direct routes including Miami, New York, Boston, and Charlotte significantly enhancing accessibility and market reach.

Tobagoremains heavily dependent on seasonal tourism flows and cruise passenger activity, both of which generate lower and less consistent visitor expenditure compared to long-stay stopover tourism. During the 2025/2026 cruise season Tobago’s visitor arrivals declined considerably, highlighting the vulnerability associated with a seasonally dependent tourism model.

Marketing and branding constraints compound these structural challenges. Unlike several regional competitors that have developed strong and recognisable tourism identities, Tobago’s international positioning remains fragmented and underdeveloped. While destinations such as the Bahamas and St. Lucia have successfully positioned themselves around themes such as luxury, romance, exclusivity and lifestyle tourism, Tobago has yet to establish a clearly differentiated global brand capable of attracting high-value international travellers.

Tourism in Tobago remains insufficiently integrated into the broader domestic economy. Stronger linkages between tourism and sectors such as agriculture, entertainment, transport and the creative industries could significantly enhance local value-added and improve foreign exchange retention. For example, Tobago can offer a pristine cocoa experience whereby tourists can visit functioning estates which offers tours on “bean-to-bar processing, drying and chocolate making. Such a segment within the industry have experienced extreme success within other markets however, underexploited within the Tobago market.

The Startling Statistics

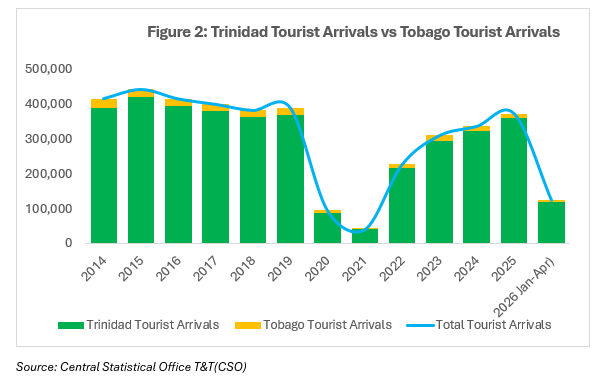

According to the Central Statistical Office (CSO), total visitor arrivals for T&T reached 373,027 in 2025 a slight increase from the 336,696 visitor arrivals in 2024. Recent quarterly data indicates a marginal contraction in stopover arrivals, which fell by 1.03% year-on-year from 97,901 in Q1’25 to 96,901 in Q1’26. Trinidad, however, continues to account for the majority of visitor arrivals. In Q1’26 Trinidad recorded 92,188 stopover visitors compared to 92,103 in the same period in 2025, representing approximately 95.1% and 94.1% of total arrivals respectively. This highlights the persistent concentration of tourism activity within Trinidad, with Tobago continuing to receive a comparatively small share of overall arrivals. The disparity becomes more evident when compared to pre-pandemic levels. In Q1’19 total visitor arrivals stood at 105,896, with Tobago accounting for 8,421 arrivals, compared to Q1’26, Tobago’s performance has declined by approximately 44.0%.

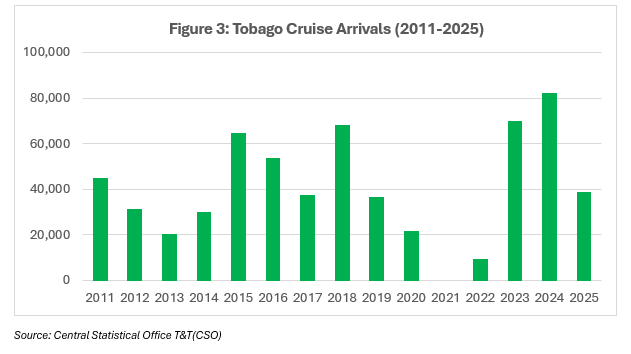

Monthly data further reinforces this downward trajectory. In March 2026, T&T recorded 28,567 stopover visitors, of which 27,807 were received in Trinidad, while only 760 were recorded in Tobago. The weakness in stopover performance is compounded by declining cruise tourism activity. According to the Division of Tourism, Tobago recorded 32 cruise calls and 37,086 passengers in the 2025/2026 season, compared to the 41 calls and 51,069 passengers in 2024/2025. This follows a stronger 2023/2024 season, which recorded 64 cruise calls and 102,512 passengers, indicating a sustained downward trend.

Panama’s Stopover Success

A useful comparative example can be found in Panama, which has successfully leveraged stopover tourism as a tool for economic diversification and foreign exchange generation. While Tobago continues to face challenges related to connectivity and destination competitiveness, Panama demonstrates how strategic policy intervention can transform transit traffic into a significant source of tourism revenue. Over the past decade, Panama has repositioned itself from being viewed primarily as a transit hub into one of Latin America’s leading tourism and service-based economies. Rather than allowing millions of passengers to simply pass through its airports, policymakers implemented targeted initiatives aimed at converting transit travellers into stopover visits.

One of the most successful initiatives was the partnership between Copa Airlines and the Panama Tourism Authority, which introduced structured stopover programmes allowing passengers to remain in Panama for several days at little or no additional airfare cost. Instead of competing solely as a traditional leisure destination, Panama positioned itself as a convenient urban, cultural, business tourism experience for travellers already moving through the region. In effect, layovers were transformed into economic opportunities.

This strategy was supported by sustained international marketing campaigns promoting Panama as a destination for shopping, eco-tourism, business travel and cultural tourism. Simultaneously, investments in hotels, convention centres, transport infrastructure and urban redevelopment projects such as Casco Viejo (historical district filled with cobblestone, colonial architecture, vibrant night life) enhanced the overall visitor experience and increased tourism expenditure throughout the economy.

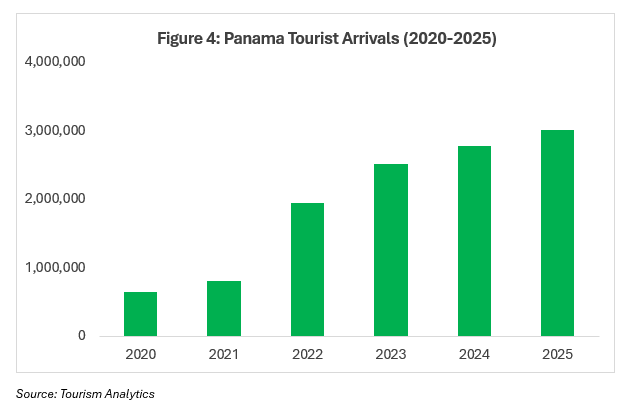

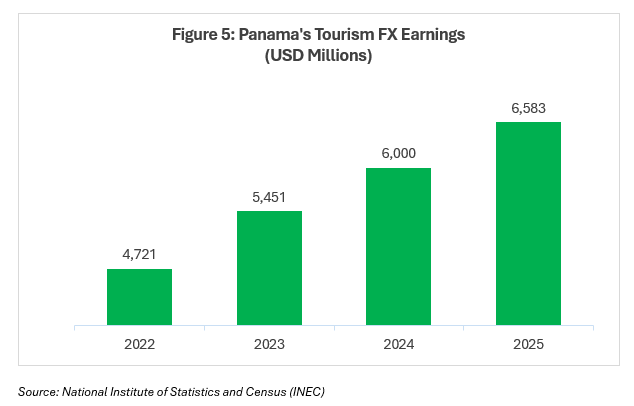

The results were significant. Tourism evolved into one of Panama’s largest service export sectors, generating billions in foreign exchange earnings and supporting employment across hospitality, transportation, retail and entertainment. According to Panama’s National Institute of Statistics and Census, the country recorded 999,934 international visitor arrivals during Q1’26, representing a 17.3% increase compared with the corresponding period of 2025. The sector generated more than USD2 billion in tourism related expenditure. Additionally, Panama’s stopover programme continued to gain momentum, with visitor participation by 37% through April 2026, surpassing 88,000 travellers.

Panama’s experience illustrates that stopover tourism, when supported by airline partnerships, infrastructure investment and coordinated destination marketing, can become an effective mechanism for economic diversification. The model offers valuable lessons for Tobago if they are serious about strengthening tourism competitiveness and expand its contribution to national economic growth.

Building Tobago into a Forex Goldmine

Unlike many competing destinations, Tobago already possesses a strong natural and cultural tourism product that aligns closely with evolving global travel preferences. The challenge facing Tobago is therefore not the absence of tourism assets, but rather the limitations in connectivity, strategic execution, and sustained policy coordination required to fully realise its potential.

Improving international connectivity must therefore be treated as a national economic priority. The island can adopt a Panama-style partnership model by working directly with regional and international airlines to develop stopover packages linked to Trinidad, North America and Latin America. In this context, travellers moving between North and South America could be incentivised to spend 3-5 days in Tobago through integrated packages combining airfare extensions, hotel partnerships and curated tourism experiences. The recent modernisation of the ANR Robinson International Airport, with approximately USD178 million in upgrades, provides a strong platform to support expanded international connectivity and increased visitor arrivals.

Strengthening Tobago’s global brand identity is equally important. Historically, Tobago has often been marketed as an extension of Trinidad rather than a standalone destination with distinct tourism value. However, its comparative advantage lies precisely in this distinction. Unlike more commercialised Caribbean tourism markets, Tobago offers a more intimate, nature-based experience. Positioning the island around themes such as authentic Caribbean escape, eco-luxury, wellness tourism and untouched paradise would help better differentiate it within a highly competitive regional tourism landscape.

Digital marketing and destination promotion must also become more targeted, and data driven. Panama’s success was supported by sustained international visibility and coordinated marketing efforts. Tobago can similarly leverage social media campaigns, influencer partnerships, diaspora engagement and collaboration with global travel platforms to enhance international awareness and improve destination competitiveness.

Most importantly, Tobago requires policy consistency and long-term coordination. A key weakness in T&T’s diversification agenda has been fragmented implications and short policy cycles. Tourism development cannot rely on isolated initiatives or short-term campaigns. A successful stopover strategy would require sustained coordination between government agencies, airlines, investors and private sector stakeholders over an extended period.

If effectively implemented, Tobago’s stopover strategy could significantly reshape the island’s role with Trinidad and Tobago’s economic structure. Beyond increasing visitor arrivals, it would expand foreign exchange earnings, stimulate employment creation, support small business development and reduce the overdependence on the energy sector.

Conclusion

The gap between vision and reality in T&T’s tourism development reflects a deeper structural challenge in economic transformation. While the 1969-1973 development framework correctly identified tourism as a diversification tool, execution over subsequent decades has been inconsistent. Today, Tobago stands at a critical crossroad: it can either continue its current trajectory of underutilized potential or adopt a decisive stopover tourism strategy capable of repositioning it with global travel networks. As demonstrated by Panama’s experience, strategic intent combined with policy execution can transform geography into economic advantage. For Tobago, the opportunity remains present, but increasingly time sensitive.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.