The U.S.-Iran Conflict and the impact on Tourism

Commentary

In the Caribbean, the line between a thriving tourism season and a slowing economy is becoming increasingly tied to movements in global energy prices. As crude oil prices have surged between USD90 and USD111 per barrel in early 2026 amid rising Middle East tensions, the impact is filtering into the Caribbean’s tourism dependent economies.

Higher oil prices translate directly into increased jet fuel and marine fuel expenses, which in turn drive up airfares and cruise costs. These higher travel expenses are often not immediately captured in headline inflation figures, yet they place pressure on visitor demand, government revenues, and overall economic activity. The result is tighter fiscal space and a more fragile growth outlook for many island economies.

From an investment perspective, the relationship is clear and increasingly important. Caribbean tourism should not be viewed solely as a leisure-driven sector, but rather as one with strong exposure to global energy markets. Each incremental rise in oil prices can ripple through airline profitability, reduce travel demand, and ultimately weigh on economic performance and sovereign credit profiles.

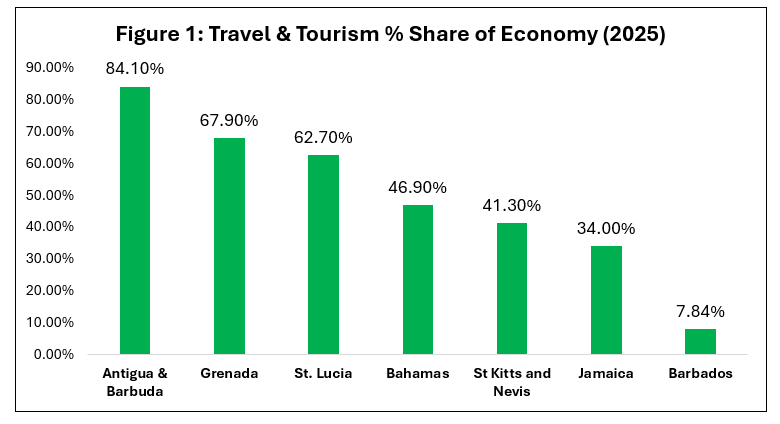

This vulnerability is particularly acute in economies where tourism contributes more than 20% of Gross Domestic Product (GDP), that is, the total value of goods and services produced within an economy. As airlines and cruise operators pass on higher fuel costs to consumers, the region’s recovery faces renewed headwinds. In this environment, both investors and policymakers must recognise that energy price dynamics are not external to the Caribbean growth story, they are central to it.

Oil Shock in the Caribbean Context

According to the World Travel & Tourism Council (WTTC), the global tourism sector contributed approximately 10% to GDP in 2024, while supporting roughly 11% of global employment. In the Caribbean, tourism plays an even more dominant role. Data from the World Tourism Organization (UNWTO) indicate that the sector accounted for approximately 17.6% of the region’s GDP in 2024, the highest share globally from a regional perspective. It also remains a critical employer, supporting an estimated 2.9 million jobs, or 15.7% of total employment across the region.

However, the tourism industry does not operate in isolation. The ongoing U.S.–Iran conflict has introduced renewed volatility into global energy markets. Disruptions to energy infrastructure in the Gulf region, along with concerns surrounding the Strait of Hormuz, a critical global shipping lane for oil, have driven energy prices higher. This is particularly relevant for tourism, which is inherently energy-intensive and heavily dependent on reliable and affordable fuel for transportation.

While current pressures are driven by geopolitical developments, the Caribbean’s vulnerability reflects deeper structural factors, including near total reliance on imported fossil fuels, limited airline competition, and relatively small domestic markets. These factors amplify the transmission of external energy shocks into tourism demand and fiscal outcomes

Air travel, ground transport, and cruise operations collectively make tourism one of the largest consumers of fuel and electricity. As a result, fluctuations in oil prices quickly translate into higher operating costs for airlines and cruise operators. These increased costs are often passed on to consumers through higher ticket prices and surcharges, which can dampen travel demand.

The Caribbean is especially vulnerable to these dynamics. The region relies almost entirely on air connectivity, with the U.S. accounting for roughly half of total visitor arrivals, and Europe and Canada contributing a significant share of the remainder. This dependence makes the region highly sensitive to any shock that increases the cost of flying or weakens consumer confidence in these key source market.

Recent movements in Brent crude oil prices highlight this risk. As of early April 2026, prices surged to approximately USD111.54 per barrel, an increase of nearly 60% compared to the previous year. This has significantly raised jet fuel costs, which typically account for between 25% and 35% of an airline’s operating expenses. In response, several airlines have implemented measures such as capacity reductions, fuel surcharges, and higher ancillary fees. In Trinidad and Tobago, Caribbean Airlines introduced fuel surcharges ranging from USD15 to USD25 on regional and international tickets to offset rising fuel costs.

Cruise operators, which are vital to Caribbean tourism, are facing similar pressures. Carnival Corporation, which does not hedge its fuel costs, has already revised its 2026 outlook downward due to an estimated USD500 million increase in fuel expenses. In contrast, Royal Caribbean Group, which hedges approximately 60% of its fuel needs, has demonstrated greater resilience. Nonetheless, the broader industry is adjusting pricing structures, with some operators introducing additional charges of up to USD25 per guest per day.

These rising costs are translating into overall vacation price increases of approximately 10% to 15%, placing a disproportionate burden on middle-income travellers, who account for nearly 70% of visitor arrivals to the region.

Impact so far on Caribbean Tourism

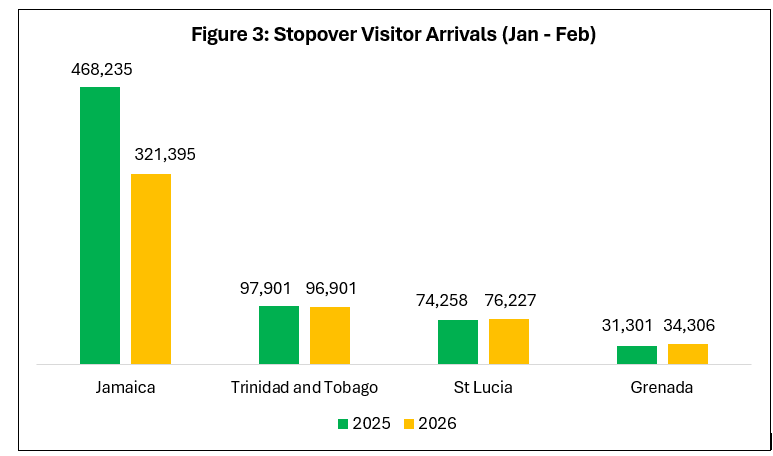

The Caribbean tourism sector recorded a notable recovery in 2025, with stay-over arrivals reaching approximately 35 million visitors, about 2.5% above pre-pandemic levels. This marked an important milestone for the region, reinforcing tourism’s role as a key driver of economic activity. However, early data for 2026 suggest that this momentum is beginning to moderate. In the first quarter of 2026, arrivals totaled 9.2 million, compared to 8.5 million in 2019, but growth has started to soften across several major destinations, including Jamaica and Trinidad and Tobago.

This emerging slowdown is closely linked to developments in global energy markets. As oil prices increase, airlines are faced with a difficult trade-off: either absorb higher fuel costs, which compresses profitability, or pass these costs on to consumers through higher ticket prices and reduced flight capacity. In practice, a combination of both responses tends to prevail, ultimately weighing on travel demand, particularly among more price-sensitive consumers. Many travellers may choose closer or more affordable alternatives, such as Mexico, Central America, or domestic travel within the U.S. rather than longer-haul Caribbean destinations.

From a broader economic perspective, the implications can be significant. A slowdown in tourist arrivals can reduce foreign exchange inflows, weaken government revenues, and constrain fiscal flexibility at a time when many Caribbean economies are still rebuilding from the pandemic. In this context, volatility in oil prices effectively acts as an external economic shock, with the potential to slow growth and place additional pressure on sovereign credit profiles.

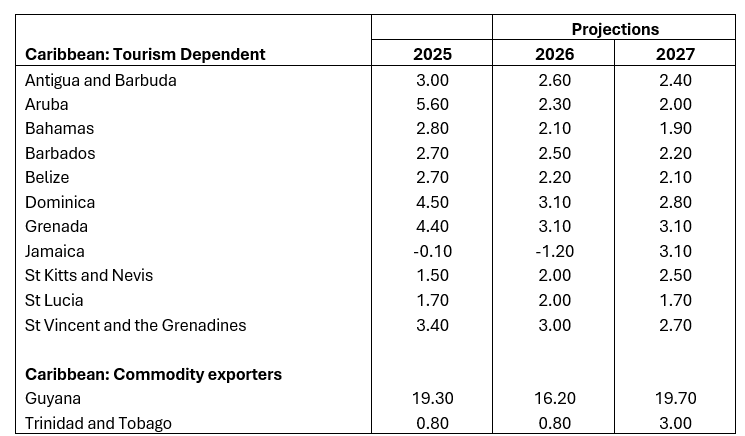

This view is reinforced by the International Monetary Fund (IMF), which has indicated that Caribbean economies are likely to be among the most adversely affected by the sustained increases in global oil prices. In its April 2026 World Economic Outlook, the IMF revised downwards economic growth forecasts for the region, particularly the tourism-dependent economies, due to rising risks relative to its October 2025 projections. Many countries in the region are both heavily dependent on tourism and reliant on imported fuel. As a result, elevated and volatile oil prices affect them on two fronts. On the cost side, higher fuel prices increase operating expenses for airlines, hotels, and other tourism-related services, reducing overall profitability. On the demand side, these higher costs are often passed on to visitors through increased travel and accommodation prices, which can weaken demand.

This dual impact places added strain on economic growth. With many Caribbean countries already carrying high levels of public debt, lower tourism revenues and reduced foreign exchange inflows make it more challenging to service foreign-denominated debt and meet ongoing financial obligations.

Market Impacts and Investor Considerations

Elevated energy prices caused by the U.S.–Iran conflict are already weighing on the airline, cruise‑line, and hotel sectors. Many stocks in these industries are underperforming broader markets as investors worry about higher operating costs, squeezed profit margins, and more volatile travel demand.

Several major airlines and cruise‑line companies have recently cut or revised down their profit forecasts and earnings guidance, largely due to rising fuel and operating costs tied to higher oil prices and the ongoing conflict. Carnival Corporation & plc, the world’s largest cruise operator, has lowered its full‑year adjusted earnings‑per‑share guidance from a previous range of up to about USD2.48 to roughly USD2.21, citing higher fuel bills and cost pressures. Delta Air Lines has also trimmed its 2026 profit outlook and scaled back growth plans, pointing to rising fuel costs and weaker‑than‑expected earnings compared with Wall Street forecasts. Even where companies have not cut their own guidance, major investment banks have significantly downgraded the 2026 profit and earnings estimates for airlines and cruise-line companies.

The pressure is also spreading to bond markets. In tourism‑dependent countries such as Jamaica and Barbados, investors are taking a closer look at credit risk as expectations for visitor‑driven revenue weaken. This is making borrowing costs and market sentiment more sensitive to any further shocks in energy prices or travel demand.

The Road Ahead: Managing Turbulence Through Risk and Resilience

Looking ahead, the outlook for Caribbean tourism remains closely tied to the path of oil prices. If crude stays above USD100 through 2026, the region could see a 2–4% contraction in tourist arrivals, pushing GDP growth in tourism-dependent economies to below 1%. On the other hand, if geopolitical tensions ease, particularly in the Middle East, and prices settle closer to the USD90–100 range, there is room for a rebound supported by pent-up travel demand, with early Q2 booking trends already showing some resilience.

For investors, this environment calls for a more deliberate and selective approach. Tourism-linked assets such as airlines, hospitality operators, and travel-dependent businesses, may face near-term earnings pressure as higher operating costs compress margins and soften demand. Conversely, sectors and companies with direct or indirect exposure to energy markets, or those with strong pricing power and resilient balance sheets, are better positioned to navigate this period of elevated costs.

At the portfolio level, diversification remains essential. Allocations to commodities and energy-related assets can provide a natural hedge against sustained oil price increases, while maintaining exposure to high-quality equities ensures resilience amid volatility. Importantly, investors should avoid broad-based regional assumptions and instead focus on country and company-specific fundamentals, as vulnerability to energy shocks varies across the Caribbean.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.