The Evolution of Banking in the Age of Digital Assets

Commentary

A New Era for Banking

The banking industry is entering one of the most transformative periods in its history. For decades, banks operated through centralized systems built around physical branches, traditional currencies, and trusted intermediaries. While online banking and mobile apps modernized customer experiences, the underlying structure of banking remained largely unchanged.

The rise of digital assets, however, is fundamentally altering how money moves, how investments are made, and how financial institutions operate. What began with Bitcoin in 2009 has expanded into a global ecosystem of cryptocurrencies, stablecoins, tokenized assets, decentralized finance platforms, and central bank digital currencies (CBDCs).

Today, digital assets are no longer viewed solely as speculative investments. They are becoming integrated into mainstream finance, forcing banks to rethink traditional business models and embrace new forms of innovation. The shift is not merely technological; it represents a structural evolution of the financial system itself.

Several factors have accelerated this transformation in recent years, including advances in blockchain technology, growing institutional investment, increasing customer demand for digital financial products, and regulatory developments that have provided greater clarity around digital asset markets. Together, these forces are driving the integration of digital assets into the mainstream financial system and encouraging banks to explore new ways of delivering financial services.

The Rise of Digital Assets

Digital assets are financial assets that exist in electronic form. Unlike physical assets such as real estate, machinery, or equipment, digital assets are created, stored, transferred, and managed electronically through digital platforms and networks.

There are several categories of digital assets, including cryptocurrencies, which are digital currencies that operate using blockchain technology. Blockchain is a secure digital ledger that records, verifies, and permanently stores transactions across a decentralized network of computers. This technology enables transactions to be conducted securely, transparently, and without the need for a central intermediary.

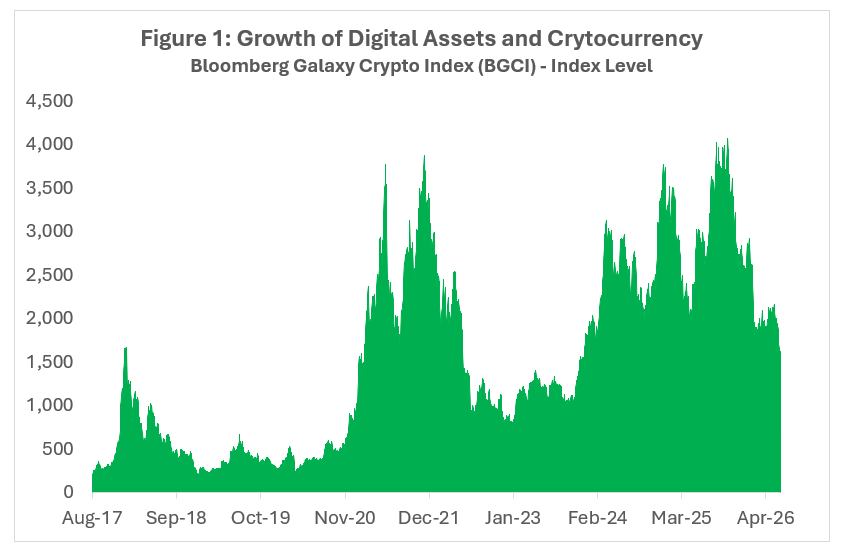

The most widely recognized cryptocurrency is Bitcoin, which was the world’s first successful decentralized cryptocurrency and remains the largest by market value. Since its introduction in 2009, the cryptocurrency market has expanded dramatically, evolving from a niche innovation into a global financial ecosystem.

Today, thousands of cryptocurrencies exist, each designed to serve a distinct purpose within the digital economy. While some function primarily as digital currencies for making payments and transferring value, others support more advanced applications. These include decentralized applications (dApps), which are software programs that operate on a blockchain network rather than being controlled by a single company and digital asset trading, which involves the buying, selling, and exchange of cryptocurrencies.

Initially, many banks viewed digital assets with scepticism due to concerns surrounding volatility, regulation, and fraud. However, institutional adoption has grown rapidly over the past few years. Large corporations, hedge funds, payment processors, and even governments are now participating in the digital asset ecosystem. This growth has forced banks to acknowledge that digital assets are no longer a fringe innovation. Instead, they are emerging as a legitimate part of the global financial infrastructure.

Source: Bloomberg

Transforming Payments and Cross-Border Transactions

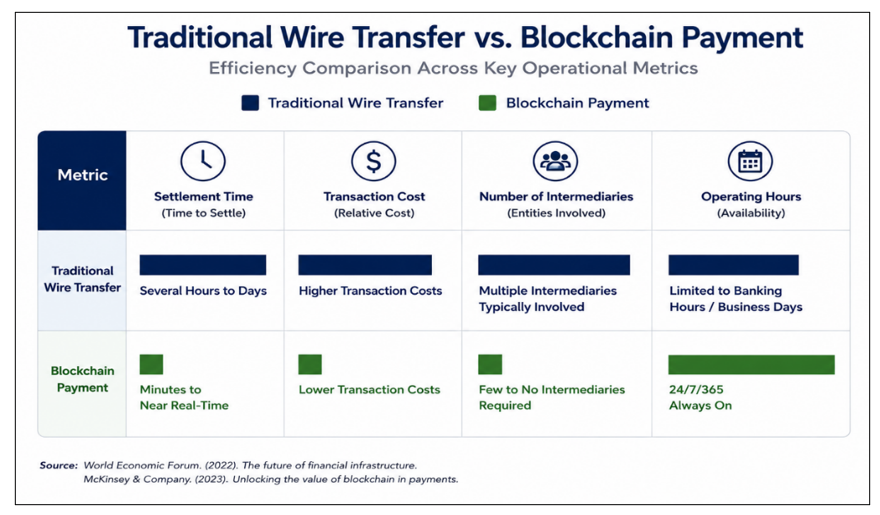

One of the biggest ways digital assets are changing banking is through payments and money transfers. Traditional cross-border transactions are often expensive, slow, and dependent on multiple intermediaries. International wire transfers can take several days to settle and usually involve high fees. Blockchain technology offers a faster and more efficient alternative. Digital asset transactions can often be completed within minutes, and in some cases near real-time, depending on the underlying blockchain network. Stablecoins, in particular, are becoming increasingly important because they combine the speed of blockchain with the stability of fiat currencies.

For banks, the rise of digital assets presents both significant opportunities and growing competitive challenges. Fintech firms, businesses that leverage technology to enhance, streamline, and automate financial products and services, and crypto-native companies, whose operations and offerings are built around cryptocurrencies, blockchain technology, and digital assets, are increasingly reshaping the financial landscape. Many of these firms now provide innovative payment solutions that enable funds to be transferred quickly and efficiently, often without relying on traditional banking infrastructure. As a result, banks face increasing pressure to adapt their business models, embrace technological innovation, and remain competitive in an evolving digital economy.

In response, many financial institutions are investing in blockchain-based payment systems and similar networks to modernize their operations and enhance service delivery. These technologies have the potential to facilitate near real-time settlement of transactions, reducing the need for lengthy clearing processes and multiple intermediaries. By improving transaction speed and efficiency, banks can lower operational costs, strengthen liquidity management, reduce settlement risk, and enhance the overall customer experience, positioning themselves more competitively in the digital era.

Source: World Economic Forum

Digital Asset Custody and Wealth Management

As digital assets become more widely accepted, investors are increasingly seeking secure ways to store them. This has created a major opportunity for banks in digital asset custody services. Traditionally, banks safeguarded assets such as stocks, bonds, and cash. Now, they are beginning to provide custody solutions for cryptocurrencies and tokenized assets as well. Institutional investors especially prefer regulated banks due to their reputation, compliance frameworks and security infrastructure.

Several major financial institutions have already entered the digital asset space. JPMorgan Chase & Co. has developed blockchain-based payment and settlement systems through its Kinexys by J.P. Morgan, formerly known as Onyxplatform and JPM Coin initiative. BNY Mellon launched digital asset custody services for institutional clients, allowing investors to hold cryptocurrencies alongside traditional assets, while Goldman Sachs expanded into cryptocurrency trading and blockchain-focused investment products. Other global banks such as State Street, HSBC, and Standard Chartered have also invested in tokenization platforms and digital asset infrastructure to support growing institutional demand.

The wealth management industry is also evolving. Younger generations of investors are far more comfortable with digital assets than previous generations. As a result, banks and investment firms are expanding their offerings to include crypto investment products, blockchain-focused funds, and tokenized investment opportunities. This shift reflects a broader change in investor behaviour. Clients increasingly expect their banks to provide exposure to both traditional and digital financial markets within a single ecosystem. These developments demonstrate that digital assets are no longer operating outside the traditional financial system but are increasingly becoming integrated into mainstream banking operations and wealth management strategies.

Tokenization and the Future of Capital Markets

One of the most transformative innovations within digital finance is tokenization. Tokenization refers to converting ownership rights of real-world assets into blockchain-based digital tokens. These assets can include real estate, stocks, bonds, commodities, fine art, and private equity, allowing traditionally illiquid or high-cost investments to become more accessible to a broader range of investors.

Tokenization has the potential to reshape capital markets by increasing liquidity and reducing transaction friction. Through fractional ownership, investors could gain exposure to assets that were previously inaccessible due to large capital requirements. For example, instead of purchasing an entire commercial property or large investment stake, individuals could own smaller portions represented by digital tokens on a blockchain network.

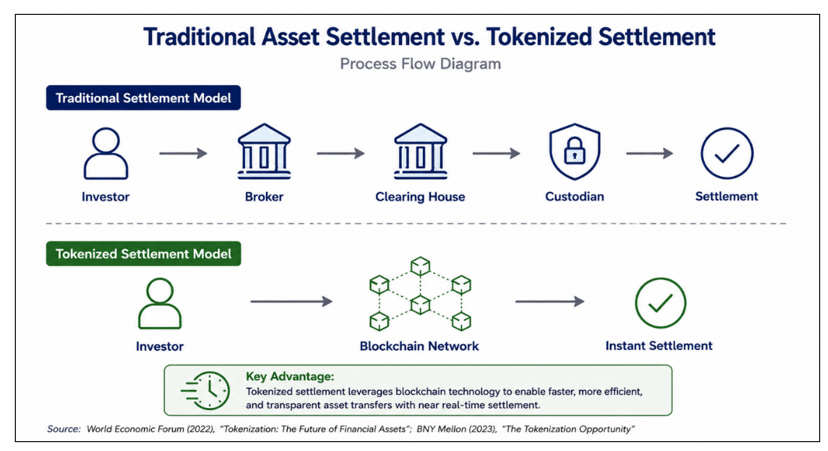

For banks, tokenization presents enormous possibilities. Traditional securities settlement systems are often slow and operationally complex because multiple intermediaries must reconcile transactions before settlement is finalized. Blockchain technology can streamline this process by enabling near-instant settlement, automated recordkeeping, and transparent ownership tracking. This not only reduces operational inefficiencies but may also lower transaction costs and counterparty risk across financial markets.

In the future, tokenized financial markets could operate continuously, reducing delays and improving efficiency across global finance. As adoption grows, tokenization may fundamentally change how assets are issued, traded, and managed within the banking industry.

Source: World Economic Forum

Decentralized Finance (DeFi): A Challenge to Traditional Banking

Another major disruption comes from decentralized finance, commonly known as DeFi. DeFi platforms use blockchain-based smart contracts which are digital agreements that self-execute without the need of a third party, to offer financial services without relying on traditional intermediaries such as banks. Through these decentralized platforms, users are able to lend assets, borrow funds, earn interest, trade cryptocurrencies, and access liquidity pools without the involvement of traditional financial institutions.

The growth of DeFi challenges the traditional role of banks as financial intermediaries. Consumers are increasingly attracted to the speed, accessibility, and transparency offered by decentralized platforms, particularly because transactions can occur continuously without the delays and restrictions associated with traditional banking systems.

However, DeFi also introduces significant risks, including cybersecurity vulnerabilities, regulatory uncertainty, and potential smart contract failures. Because of these concerns, many experts believe banks will not disappear but instead evolve by integrating aspects of decentralized finance into regulated financial systems. In response, banks are already exploring programmable finance, automated settlements, and blockchain-based lending structures inspired by DeFi technology.

Regulation and the Rise of Central Bank Digital Currencies (CBDCs)

As digital assets continue to expand globally, governments and regulators face increasing pressure to develop frameworks that balance innovation with financial stability. Because banks operate within highly regulated environments, regulatory clarity remains essential before large-scale digital asset adoption can occur. Concerns surrounding money laundering, fraud, consumer protection, cybersecurity, and systemic risk continue to shape the regulatory response to digital assets worldwide.

In Trinidad and Tobago, regulators have taken a cautious approach toward the digital asset sector. The Virtual Assets and Virtual Asset Service Providers Act, 2025 established a regulatory framework for virtual asset activities and service providers while introducing restrictions on certain cryptocurrency-related activities as regulators work to strengthen oversight of the sector. The framework also reflects significant regulatory caution, including restrictions on certain virtual asset activities as authorities seek to strengthen oversight, address financial crime risks, and align with international standards. The legislation reflects growing concerns surrounding financial crime, investor protection, and the need to align with international regulatory standards.

At the same time, the Central Bank of Trinidad and Tobago (CBTT) has continued to explore the future of digital payments and financial innovation. The Central Bank of Trinidad and Tobago has advanced payment system modernization through its 2026 public consultation on the Draft Payment Systems and Services Bill and accompanying regulations. While this does not amount to a CBDC launch plan, it reflects continued policy focus on strengthening the safety, efficiency, and resilience of the national payments infrastructure. The proposed framework seeks to enhance the safety, efficiency, and resilience of digital payment systems while creating an environment that can accommodate emerging financial technologies.

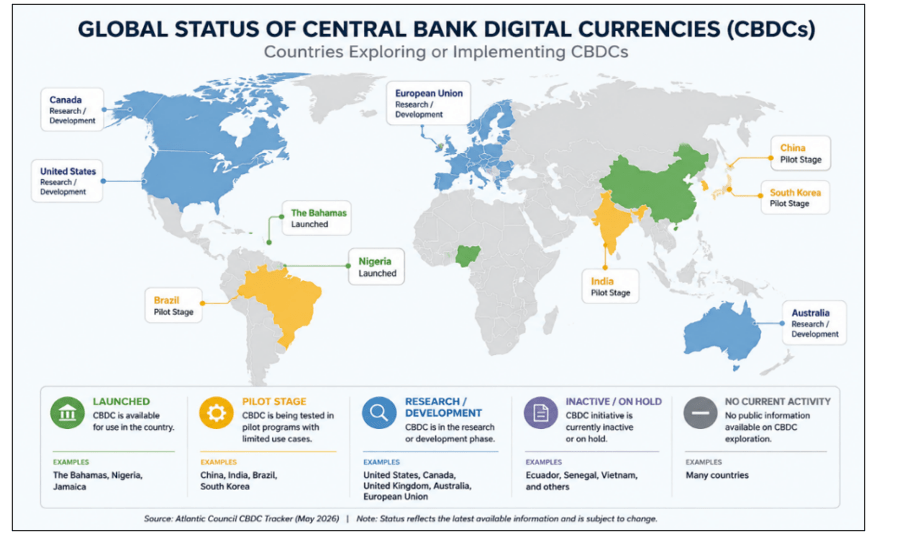

The CBTT has also acknowledged the growing global interest in Central Bank Digital Currencies (CBDCs), which are digital forms of national currencies issued by central banks. While Trinidad and Tobago has not announced plans to launch a CBDC, the ongoing modernization of the national payments system and the increasing focus on digital financial infrastructure suggest that digital currency developments will remain an important area of policy consideration in the years ahead. As central banks around the world continue exploring CBDCs, including China’s Digital Yuan (e-CNY), discussions surrounding the future of money, payments, and financial intermediation are becoming increasingly relevant for both policymakers and financial institutions.

Source: Atlantic Council CBDC Tracker

Cybersecurity and Operational Risks

Despite the opportunities digital assets provide, they also introduce new risks. Blockchain transactions are generally irreversible, meaning errors or fraud can be extremely costly. Unlike traditional banking systems where transactions may sometimes be reversed or disputed, digital asset transfers often cannot be undone once completed, increasing the importance of security and operational controls.

As a result, banks entering the digital asset space must invest heavily in cybersecurity systems, wallet security, fraud detection mechanisms, compliance infrastructure, and private key management solutions. These safeguards are essential to protecting both customer assets and institutional credibility in an increasingly digital financial environment.

Operational resilience is becoming increasingly important as digital asset adoption grows. Trust remains central to banking, and financial institutions must ensure digital asset services meet the same security standards as traditional banking operations. Strong cybersecurity frameworks and regulatory compliance will likely become critical competitive advantages as banks continue integrating digital assets into their services.

The Future of Banking in a Digital Asset Economy

Digital assets are no longer operating outside the financial system; they are becoming increasingly integrated within it. Major global banks are now exploring blockchain settlement systems, digital asset trading desks, tokenized deposits, and cryptocurrency custody solutions as they adapt to changing market dynamics and customer expectations. The future of banking will likely involve a hybrid financial ecosystem where traditional financial institutions coexist alongside blockchain infrastructure and decentralized technologies.

Banks that successfully adapt to this evolving landscape will likely gain significant competitive advantages. As consumers increasingly demand faster, more accessible, and digitally integrated financial services, institutions that embrace innovation may strengthen their relevance in the modern financial system. At the same time, those that resist technological change risk falling behind in an increasingly digital economy.

The rise of digital assets marks one of the most important transformations in modern finance. From cross-border payments and digital asset custody to tokenization and decentralized finance, these technologies are influencing nearly every aspect of banking operations and financial services. While challenges surrounding regulation, cybersecurity, and financial stability remain, the long-term direction is becoming increasingly clear: digital assets are steadily moving from the margins of finance into the mainstream.

The banking industry has consistently evolved alongside technological innovation, from online banking and electronic payments to mobile financial services. Digital assets represent the next major chapter in that evolution, one that may fundamentally redefine how money, investments, and financial services function in the decades ahead.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.