The “DEBT” of the Middle Class

Commentary

Introduction:

In the medical field, the term “pandemic” is defined as a widespread epidemiological contagion that crosses borders and affects large populations simultaneously. In a broader context, the concept suggests a pervasive and systematic phenomenon rather than a series of isolated or temporary developments. Through these lenses, the decline in the middle class increasingly resembles that of an economic pandemic, reflecting a structural trend unfolding across both advanced and emerging economies. Since the global financial crisis of the late 2000’s and more recently amid inflationary shocks and persistent cost-of-living pressures, middle-income households have become more reliant on borrowing to sustain consumption, preserve living standards and finance essential needs. What was once a mechanism for upward mobility, in many instances, has become a necessity for maintaining financial stability. The normalization of debt-financed consumption raises pertinent questions about the long-term resilience of middle-income households and the sustainability of consumption-led growth.

Framing the Issue: How is the Middle Defined?

Defining a social class may appear straightforward, but in practice it is a complex and multidimensional exercise. The middle class cannot be captured by income alone, it is more accurately understood through a combination of income thresholds, economic security and social or cultural characteristics. The Pew Research Centre defines middle-income households in the US as those earning between USD37,000 and USD167,460 annually, adjusted for household size and cost of living. Beyond earnings, economic stability is a central pillar of the middle-class status. This includes the ability to absorb unexpected financial shocks, maintain adequate health insurance coverage, and accumulate savings for retirement.

Cultural and lifestyle factors also play an important role in shaping perceptions of the middle class. These are often associated with material conditions and consumption patterns, such as homeownership, access to private transportation, stable employment and sufficient disposable income to support leisure and savings. Collectively, these elements distinguish the middle class not only as an income group but as a segment defined by relative security and participation in mainstream economic life.

In economic literature the middle class is frequently defined as households earning between 75% and 200% of median national income. Historically, this group has been the cornerstone of mass consumption, social cohesion and macroeconomic stability. Consequently, any sustained erosion in the financial stability of this group carries broader macroeconomic implications.

Evidence of the Decline

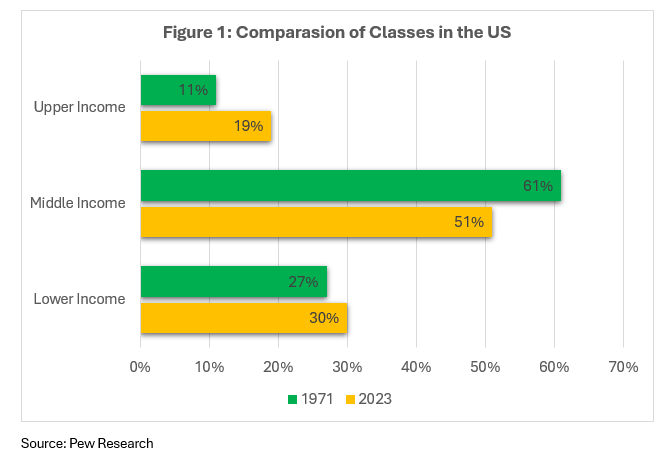

Data from the Organization for Economic Co-operation and Development (OECD) shows that the share of the population in advanced economies classified as middle-income households has declined from 64% to 61% in recent decades. In the United States, the middle class contracted from 61% of the population in 1971 to 51% by 2023, according to data from Pew Research Centre. These statistics suggest that middle income households are experiencing deeper structural pressures, including sluggish real income growth, widening inequality, and rising cost of essential goods and services (housing, education, healthcare and food) which are eroding their traditional economic security.

Is Debt now Funding the Middle-Class Lifestyle?

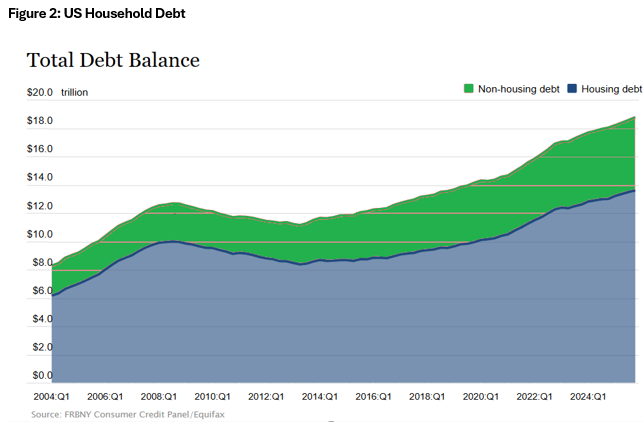

According to the Federal Reserve Bank of New York, household debt in the US totalled USD18.8 trillion as at Q4’25, based on their Quarterly Report on Household Debt and Credit. Within this current economic environment, a growing share of households’ report living “pay check to pay check”, with limited saving buffers and reduced capacity to absorb unexpected expenses. As a result, many are only one adverse shock away from “financial catastrophe”.

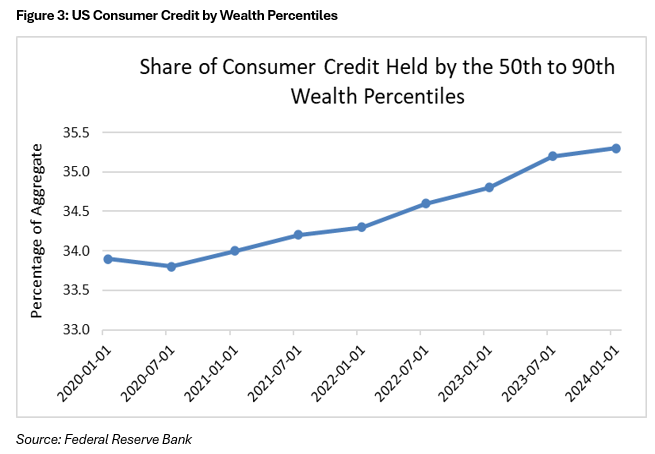

This dynamic suggests that a meaningful portion of the middle class is increasingly financing its standard of living through credit rather than income growth in the US. Data from the Federal Reserve’s Distributional Financial Accounts shows supporting evidence of this whereby, households within the 50th to 90th wealth percentiles, commonly used as a proxy for the middle and upper middle-income groups, account for a significant share (approximately 35%) of outstanding consumer credit in the US. This signals that borrowing has become a structural component of middle-class household balance sheets. Easy access to borrowing has also compounded this development, with households commonly using loans to fund major purchases such as housing and vehicles, as well as everyday consumption including clothing, appliances and furniture. The widespread use of instalment plans and the “buy now, pay later” facilities further underscore the reliance on credit to sustain consumption.

The underlying driver of this pattern is prolonged real wage stagnation combined with elevated inflation, which has sharply increased the cost of essential goods and services. Credit has therefore become the proverbial bridge between rising cost of living and the desire to maintain an established lifestyle. However, this normalized reliance on borrowing is placing mounting financial pressure on households. Resulting in increasing unbalanced household budgets, where debt servicing obligations outpaces income growth, heightening financial vulnerability over time.

Economic Pressures in a Trinidad and Tobago Context: Inflation, Wages and Household Debt

Given the absence of recent comprehensive income distribution data in Trinidad and Tobago, shifts in the middle-income population cannot be directly measured. Consequently, analysis must rely on broader macroeconomic indicators that capture pressures on household finances.

Inflation has remained relatively subdued in recent years, but it has contributed to the gradual erosion of consumers’ purchasing power. Data from Trinidad and Tobago’s Central Statistical Office (CSO), indicate that headline inflation averaged below historical norms through 2024 to 2026, with year-on-year inflation recorded at 0.7% in January 2026. While this suggests overall price stability, essential categories, particularly food and household services, have experienced more pronounced increases at various intervals, disproportionately affecting middle-income households. Annual Consumer Price Index (CPI) data from the Central Bank of Trinidad and Tobago (CBTT) illustrates the long-term impact of these price changes. The index value stood at 36.1 in 1998 and 125.3 in 2025, reflecting cumulative inflation of approximately 247% over the 27-year period. With further analysis, realistically this means that a basket of goods that cost TTD100.00 in 1998 would now require roughly TTD347.00 to purchase the same items, highlighting an erosion of income as well as purchasing power.

At the same time, wage growth has remained relatively modest. Available earnings estimates suggest that average monthly incomes for many workers outside the energy sector have been broadly stagnant, limiting the ability of nominal salary adjustments to meaningfully outpace living cost. Minimum wage data illustrates this dynamic. The statutory wage increased from TTD7.00 per hour in April 1998 to TTD20.50 currently, representing an increase of TTD13.50, equivalent to approximately 192.9% over more than two decades. When adjusted for cumulative inflation over that period, the real value of income gains is considerably less pronounced.

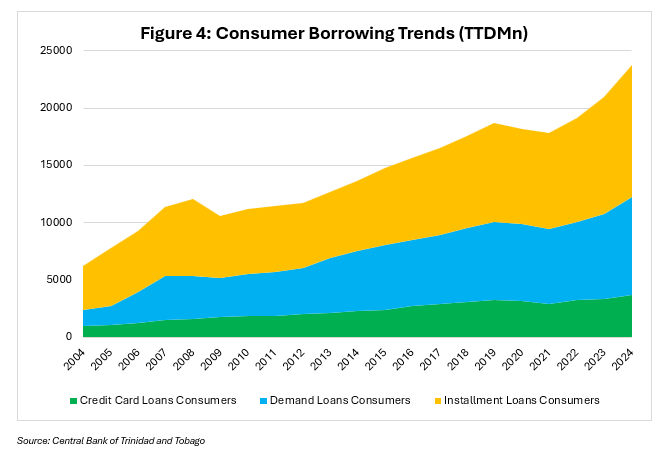

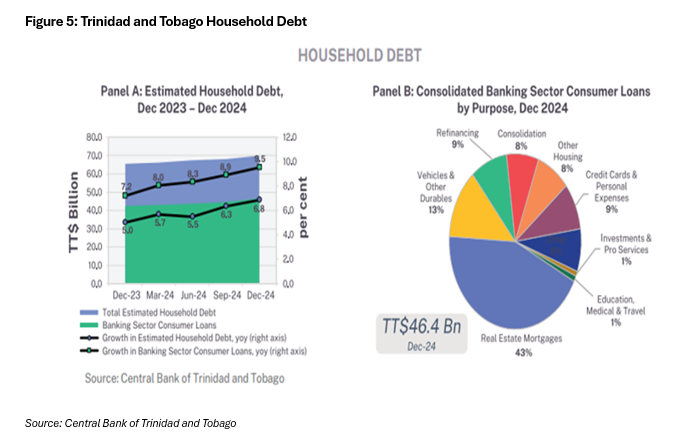

Given the economic conditions of rising cost of living and relatively stagnant wages, household indebtedness has been on an upward trend and continues to rise. The Central Bank of Trinidad and Tobago’s most recent Financial Stability Report indicates that household debt increased to an estimated TTD70 billion in 2024, representing a 6.8% year-on-year increase. This is equivalent to 40.6% of GDP, driven largely by growth in consumer lending, mortgages and motor vehicle loans. The expansion in borrowing suggests that households are becoming increasingly reliant on credit to smooth consumption and meet rising expenses.

While rising household debt and inflation do not on their own confirm the contraction in the middle class, they are consistent with an environment in which middle-income households face tightening budget constraints and reduced financial resilience. In absence of direct income-based measurements, the combination of modest wage growth, essential cost pressures, and increased reliance on borrowing provides indirect but meaningful evidence that the middle class may be shrinking in real economic terms rather than in absolute numbers.

Economic Consequences of a Debt funded Middle-Class

Aggregate Demand and Economic Growth – In both advanced and small open economies, a strong middle class underpins aggregate demand. In economies where consumption accounts for a large portion of GDP, a decline in the middle class will directly affect a country’s economic growth. When middle-income households increasingly rely on debt to maintain living standards, savings decline and discretionary spending weakens, reducing consumption led growth. Thus, debt constrains the traditional role of the middle class as a stable driver of demand.

Productivity and Investment in Human Capital – Middle-income households play a critical role in funding education, skills development, and other forms of human capital investment. High debt burdens, however, limit the capacity to invest in training, professional advancement and entrepreneurship, with long-term implications for productivity.

Labour Market Outcomes and Financial Stress – High household debt also affects labour market behaviour. Financial pressures can reduce labour mobility, as households are unable to relocate, change jobs or accept temporary income disruptions. This can stagnate workers into lower productivity roles resulting in a reduction of overall labour market efficiency.

Recommendation and Conclusion:

The interplay between household debt and middle-class decline is not solely a matter of credit statistics, it reflects broader structural challenges including wage stagnation, inequality and labour market transitions. Elevated debt levels can reduce long-term economic growth, by limiting household spending power and investment, while increasing financial stress and uncertainty. Globally or domestically, factors that affect the middle class who forms a key component of domestic demand, such as prolonged erosion of purchasing power may slow broader productivity gains and exacerbate social inequality.

Addressing these challenges may require an all-rounded approach. Stakeholders can promote financial literacy programmes to help households better manage debt, understand interest rates and build sustainable saving habits. In tandem, structural measures such as supporting wage growth in non-energy sectors, promoting skill development to match evolving labour market needs and targeted social policies can help rebuild financial security and stability of the middle class. Combining education, policy and institutional support, can aid, in mitigating the risks associated with rising household debt and foster a more resilient economy.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.