The Cost of Aging Gracefully–

The Economics Behind Trinidad and Tobago’s Pension Reform

Commentary

Introduction

The Caribbean region faces a growing and urgent challenge: the mounting strain on national insurance and pension systems. These once-robust safety nets are increasingly threatened by demographic shifts, structural pay-out demands and declining contributor bases. In Trinidad and Tobago, the case of the national contributory system, largely administered by the National Insurance Board (NIB), illustrates how this problem has moved from an actuarial warning to a clear fiscal priority.

A Nation Growing Older

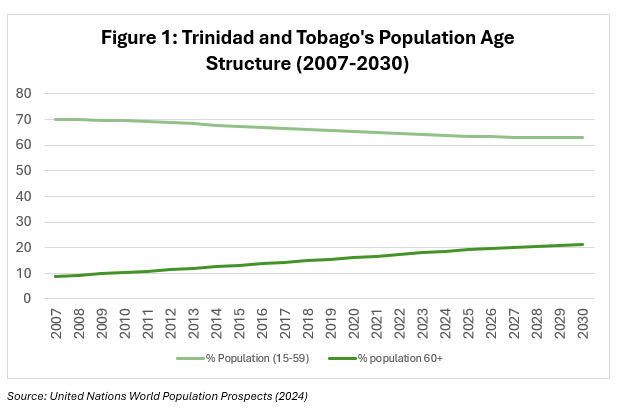

According to theUnited Nations World Population Prospects (2024) report, citizens aged 60 and over now make up roughly 16% of Trinidad and Tobago’s population, compared to about 13% in the early 2000s. Fertility rates have declined to 1.5 births per woman (2020),according to the World Bank well below the replacement rate (the average number of children a woman needs to have for a population to replace itself from one generation to the next) of 2.1, while life expectancy has increased to approximately 71 years (2021) according to the World Health Organization (WHO). This means more people are living longer after retirement, while fewer young workers are entering the workforce to support them.

Actuarial projections from the National Insurance Board of Trinidad and Tobago (NIBTT) indicate that the ratio of contributors to pensioners, which stood at 3.7 to 1 in 2013, will fall to around 1.1 to 1 by 2060 if no changes are made. In simple terms, within a generation, each active contributor could be supporting one retiree. Between 2016 and 2020, the number of active contributors fell by more than 60,000, even as the number of pensioners continued to grow. The country’s demographic shift is creating a structural imbalance that threatens the long-term viability of the national insurance system.

The Financial Strain on the NIB

According to the NIBTT’s most recent financial reports (2024), contribution income was approximately TTD4.7 billion, while benefit payments totalled about TTD6.5 billion. This created a deficit of nearly TTD1.8 billion, marking the third consecutive year in which expenses exceeded income. If this pattern continues, the Fund’s reserves could be depleted within the next decade (by 2035).

A major concern is that about 88% of pensioners (2020) receive the minimum pension regardless of their contribution history. This weakens the link between contributions and benefits, discourages full compliance, and reduces revenue. Meanwhile, the government’s non-contributory Senior Citizens’ Pension (SCP) has become an even larger fiscal burden. The Ministry of Finance reported that between 2021 and 2024, the SCP cost the state TTD16.6 billion and benefited over 114,000 older persons. For fiscal year 2025, SCP expenditure is expected to reach TTD4.6 billion. Together, the NIB’s deficit and the government’s transfer programs now account for nearly 5% of GDP (2025).

The 2025/26 Budget: Confronting the Crisis

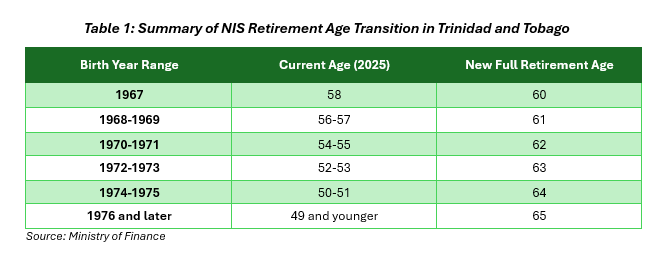

The 2025/26 National Budget, presented in October 2025, marked a decisive step toward addressing this growing problem. According to the Ministry of Finance (2025), the government will implement a phased reform plan beginning in 2026. The contribution rate, which is currently 13.2% of insurable earnings, will be increased gradually over two years to 16.2% in 2026 and 19.2% in 2027. The statutory retirement age, currently at 60 years, will also rise to 65 through incremental increases starting in 2028.

The finance minister emphasized that these measures are necessary to protect the Fund’s solvency and ensure fairness between current and future retirees. Existing pensioners and individuals who qualify before the transition will not be affected by the change. The government expects the reforms to extend the lifespan of the NIB’s reserves by at least 15 years (to approximately 2040) and improve the system’s sustainability.

The Budget also highlighted the need to modernize the NIB’s administrative systems and expand coverage to the self-employed and informal sector, which represent roughly 20% of the workforce (2024). Greater compliance and inclusion are seen as key steps in closing the gap between inflows and payouts.

Macroeconomic and Fiscal Implications

The pension challenge is not just about social security; it carries major macroeconomic consequences. The NIB is one of Trinidad and Tobago’s largest institutional investors, holding substantial positions in government bonds, corporate equities, and real estate. As reserves decline, the Fund’s ability to invest in long-term national projects, such as housing and infrastructure, is reduced. This weakens the flow of domestic capital that supports growth and development.

If the NIB’s reserves continue to shrink, the government could eventually be forced to assume responsibility for its liabilities, effectively turning pension shortfalls into public debt. With debt already around 67% of GDP (2025), such a move would significantly constrain fiscal flexibility. At the same time, the aging population is expected to place further pressure on public finances through rising healthcare and social assistance costs. Without reforms, pension-related spending could become one of the country’s most persistent fiscal risks.

A Regional Challenge

Trinidad and Tobago’s situation is not unique. Across the Caribbean, similar challenges are emerging. Barbados, Jamaica, and The Bahamas have all reported funding shortfalls and shrinking contributor bases. Many of these countries have already begun to implement key reforms to their pension systems. Barbados has increased its retirement age to 67 (2023), Jamaica has introduced stricter compliance monitoring (2022), and The Bahamas has announced plans to adjust contribution rates (2024). Trinidad and Tobago’s reforms are therefore in line with broader regional efforts to stabilize pension systems.

The Way Forward

Securing the future of Trinidad and Tobago’s pension system will require a mix of short-term discipline and long-term vision. Actuarial experts have recommended a combination of parametric reforms, such as adjusting contribution rates and retirement ages, along with structural changes that address compliance, governance, and investment management.

Expanding coverage to informal and self-employed workers is vital to widen the contributor base. Strengthening digital systems to track payments and enforce compliance will help reduce evasion and ensure greater equity. The NIB’s investment portfolio must also balance risk and return to preserve the real value of reserves in an environment of moderate inflation and slow growth.

Public trust will play a decisive role in the success of any reform. Pension policy touches nearly every household, and transparency will be critical. Workers need assurance that their contributions are protected, while retirees must be confident that promised benefits will be maintained. Effective communication from both the NIB and the government can help build confidence and reduce resistance to change.

Trinidad and Tobago is at a critical juncture. According to official projections, the NIB’s reserves could be depleted by the mid-2030s if current trends continue. The 2025/26 Budget represents a necessary course of correction aimed at preventing that outcome. But reform cannot end with legislation; it requires continuous management, periodic reviews, and national dialogue.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.