The Caribbean’s Productivity Puzzle: Unlocking Growth Potential

Commentary

Productivity is the untapped engine of growth across the Caribbean, one of the most critical yet most underperforming drivers of the region’s long-term economic development. While many economies in the region have achieved macroeconomic stability and moderate growth, productivity levels continue to lag behind global peers, constraining income convergence, competitiveness, and resilience to external shocks. According to the Inter-American Development Bank, labour productivity growth in Latin America and the Caribbean has averaged less than 1% annually over the past decade, significantly below emerging Asia, where productivity growth has exceeded 3–4% in several economies. In an increasingly competitive global economy, productivity is not merely a technical metric but a key determinant of economic transformation. For small, open Caribbean economies, improving productivity is essential to enhancing export competitiveness, attracting investment, and sustaining long-term growth.

Understanding the Productivity Gap

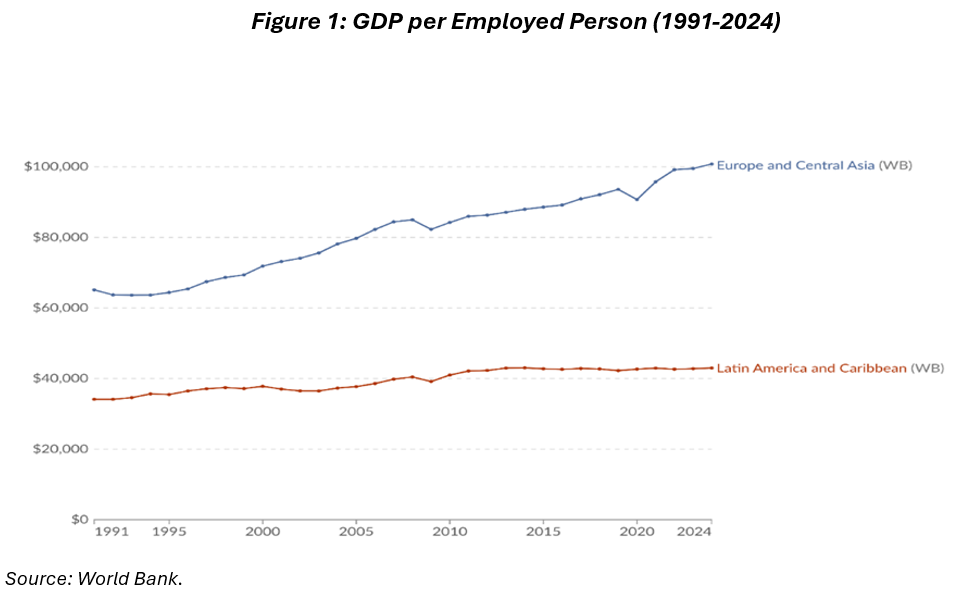

Productivity, as defined by the United Nations, reflects the efficiency with which labour, capital, and other inputs are transformed into economic output. Labour productivity, the most widely used productivity statistic, is commonly measured via output per worker, or alternatively via output per hour worked. At the macroeconomic level, labour productivity is a key determinant of long-term growth, competitiveness, fiscal strength, and overall improvements in living standards. Data from the World Bank indicates that labour productivity remains structurally low and stagnant across the Caribbean (see Figure 1). GDP per worker in many Caribbean economies is less than half that of high-income countries and, in some cases, trails even middle-income Latin American peers.

Several structural characteristics contribute to this gap. Caribbean economies are typically concentrated in a narrow set of sectors. For example, tourism accounts for over 25% of GDP in economies such as Jamaica and Barbados, while energy dominates Trinidad and Tobago’s export base. This concentration limits productivity spillovers across sectors and reduces incentives for innovation. Additionally, capital investment remains relatively low. Gross fixed capital formation across many Caribbean economies averages between 20–25% of GDP, compared to over 30% in fast-growing emerging markets. Less investment in machinery, infrastructure, and digital systems constrains firms’ ability to scale and improve efficiency.

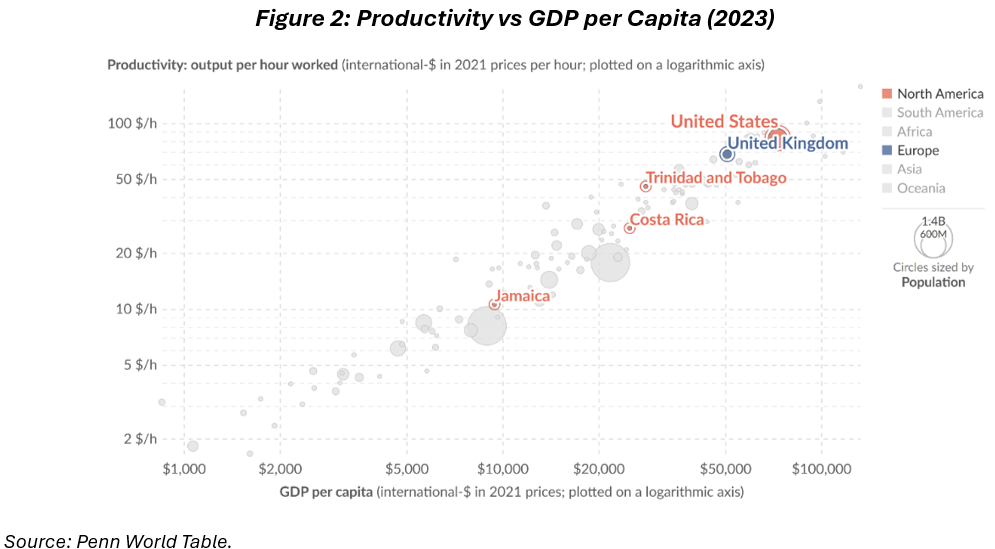

The strong positive relationship between productivity and income levels is clearly illustrated in Figure 2 below, where countries with higher output per hour consistently exhibit higher GDP per capita. Advanced economies such as the United States and United Kingdom cluster at the top-right of the distribution, reflecting both high productivity and income levels, while Caribbean economies remain positioned in the middle range. Trinidad and Tobago, for instance, performs relatively better than regional peers, with productivity levels approaching USD 40–50 per hour, yet still lags significantly behind advanced economies, highlighting a persistent productivity gap. Meanwhile, countries like Jamaica, with productivity closer to USD 10 per hour, sit much lower on the income spectrum, reinforcing the notion that limited productivity gains directly constrain income growth. This pattern underscores a key macroeconomic reality: without sustained improvements in productivity, the Caribbean’s ability to converge toward higher-income economies will remain structurally limited.

Structural Barriers to Productivity Growth

Low Technology Adoption

One of the most significant constraints on productivity in the Caribbean is the slow pace of technology adoption. According to the International Telecommunication Union, while internet penetration in the Caribbean exceeds 70% in several countries, firm-level digital adoption remains uneven, particularly among SMEs. Surveys suggest that fewer than 40% of small firms in some Caribbean economies actively use digital tools for business operations such as e-commerce, digital payments, or data analytics. This digital gap reduces operational efficiency and limits firms’ ability to compete internationally. High costs remain a key barrier. Broadband prices in parts of the Caribbean can exceed 5% of monthly income, compared to the global affordability target of 2%. Limited access to financing further constrains firms’ ability to invest in new technologies.

Skills Mismatches in the Labour Market

Human capital constraints continue to weigh heavily on productivity. The International Labour Organization reports that youth unemployment in the Caribbean averages above 20% in several economies, despite persistent skills shortages in key sectors such as ICT, engineering, and finance. This reflects a mismatch between education systems and labour market needs. While tertiary enrolment has increased, employers frequently cite gaps in digital literacy, technical skills, and managerial capacity. At the same time, brain drain remains significant. It is estimated that over 70% of tertiary-educated Caribbean nationals reside abroad in some countries, one of the highest rates globally. This loss of skilled labour reduces innovation capacity and limits the adoption of productivity-enhancing technologies.

High Levels of Informality

Informality, referring to economic activity that operates outside formal regulatory, tax, and social protection systems, remains a persistent feature of Caribbean labour markets. Estimates suggest that informal employment accounts for approximately 30–50% of total employment in several Caribbean economies. Informal firms typically exhibit lower productivity levels due to limited access to financing, training, and formal markets. From a fiscal perspective, informality also constrains government revenue. The International Monetary Fund has highlighted that high informality reduces tax collection efficiency and limits public investment in infrastructure and social services, both of which are critical for productivity growth.

Unlocking Productivity: Policy and Strategic Solutions

Strengthening Education and Workforce Development

Improving productivity begins with investing in human capital. Evidence suggests that countries that align education systems with labour market needs experience significantly higher productivity growth. Expanding technical and vocational education and training (TVET) programmes can help address skills gaps, particularly in digital and technical fields. Additionally, increasing investment in education remains critical. Public spending on education in the Caribbean averages around 4–6% of GDP, broadly in line with global benchmarks, but outcomes remain uneven. Improving quality and relevance will be key to translating spending into productivity gains.

Building Innovation Ecosystems

Innovation remains underdeveloped across the region. Research and development (R&D) expenditure in most Caribbean economies is below 0.5% of GDP, compared to over 2% in advanced economies. This limits the development of new technologies and reduces the region’s ability to move into higher value-added industries. Developing innovation ecosystems requires targeted policy support, including tax incentives for R&D, funding for start-ups, and stronger collaboration between universities and the private sector. Expanding digital infrastructure is also essential. A 10% increase in broadband penetration has been associated with up to a 1.5% increase in GDP growth in developing economies, highlighting the potential productivity gains from digital investment.

Modernizing the Private Sector

Private-sector modernization is central to improving productivity. Firms that adopt digital tools and modern management practices can experience productivity gains of 20–30%, according to global firm-level studies. Improving the business environment will be critical. This includes reducing regulatory burdens, improving access to credit, and strengthening contract enforcement. SMEs, which account for over 70% of employment in many Caribbean economies, require targeted support to scale and integrate into global value chains. Export diversification also plays a key role. Economies that move into higher value-added sectors tend to experience faster productivity growth. For the Caribbean, this includes opportunities in digital services, renewable energy, and knowledge-based industries.

Conclusion

The Caribbean’s productivity challenge is complex, but not insurmountable. While structural barriers such as low technology adoption, skills mismatches, and informality continue to constrain growth, they also highlight clear areas for policy intervention. As highlighted in broader economic transformation discussions, structural change requires coordinated and sustained effort across multiple sectors. For the Caribbean, unlocking productivity is ultimately about enhancing resilience, competitiveness, and economic opportunity. In a global economy defined by rapid technological change and increasing competition, closing the productivity gap will be critical to ensuring long-term growth and economic relevance. The region’s ability to transition from low productivity to high efficiency will determine not only its economic trajectory but also its capacity to compete in an increasingly dynamic global landscape.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.