Understanding the

Mutual Fund Industry in

Trinidad & Tobago

Commentary

Understanding the Mutual Fund Industry in Trinidad and Tobago occupy a strategic segment of the country’s financial landscape. As investors increasingly seek opportunities to grow their wealth beyond traditional savings accounts and fixed deposits, mutual funds have emerged as an accessible and effective vehicle for long-term wealth creation.

The local investment environment is characterized by a limited number of publicly listed companies in a developing capital market, and a financial system that has traditionally been dominated by commercial banks. Against this backdrop, mutual funds provide investors with access to professionally managed and diversified investment portfolios that would otherwise be difficult for many individuals to construct and manage on their own. By pooling funds from numerous investors, mutual funds allow participants to benefit from economies of scale, professional expertise, and exposure to a broad range of asset classes and securities.

What is a Mutual Fund and Its importance?

A mutual fund is an investment vehicle that pools money from multiple investors and invests those funds in a diversified portfolio of assets such as equities, bonds, money market instruments, or a combination thereof. The fund is managed by professional investment managers who are responsible for making investment decisions, conducting research, selecting securities, and monitoring portfolio performance on behalf of investors.

Each mutual fund is established with clearly defined investment objectives and an accompanying investment strategy designed to achieve those objectives. As a result, investors can select funds that align with their individual financial goals, risk tolerance, income needs, and investment horizon.

Mutual funds are designed to satisfy a wide range of investor needs. One of the most common objectives is capital appreciation, where the primary goal is to grow investors’ wealth over time. To achieve this, fund managers invest in assets with the potential for long-term value creation, particularly equities. While these funds may experience periods of market volatility, they are generally suitable for investors with longer investment horizons who are prepared to accept higher levels of risk in exchange for the potential to earn superior returns.

Figure 1: Understanding how Mutual Fund Works

Another important objective is income generation. Income-oriented funds seek to provide investors with a steady stream of earnings through investments in fixed-income securities such as government and corporate bonds, money market instruments, and dividend-paying stocks. These funds are particularly attractive to retirees and other investors seeking predictable cash flows and portfolio stability.

Some mutual funds place greater emphasis on capital preservation. These funds invest primarily in lower-risk instruments such as treasury bills, money market securities, and high-quality fixed-income investments. Although they typically offer lower returns than growth-oriented funds, their objective is to preserve capital and minimize the risk of significant losses, making them suitable for conservative investors and those with shorter investment horizons.

Source: CFI

Fixed NAV Funds vs Floating NAV Funds

Mutual funds can generally be classified into two broad categories: Fixed Net Asset Value (NAV) Funds and Floating Net Asset Value (NAV) Funds. While both structures pool investors’ funds and provide professional investment management, they differ in the way the value of each unit is determined and how investors earn returns.

Understanding the distinction between these two fund types is important, as each is designed to meet different investment objectives and cater to varying risk appetites.

Understanding Net Asset Value (NAV)

At the heart of every mutual fund is its Net Asset Value (NAV). NAV represents the value of a fund’s assets after deducting its liabilities, divided by the total number of units outstanding. In simple terms, NAV is the price at which investors buy into or redeem units from a mutual fund.

The NAV can be calculated using the following formula:

NAV = (Total Assets – Total Liabilities) ÷ Total Units Outstanding

For example, suppose a mutual fund closes the trading day with:

- Total investments valued at TT$1.5 million;

- Total liabilities of TT$575,000; and

- 500,000 units outstanding.

The fund’s NAV would be calculated as follows:

NAV = (TT$1,500,000 – TT$575,000) ÷ 500,000

NAV = TT$925,000 ÷ 500,000

NAV = TT$1.85 per unit

This means that each unit in the mutual fund is valued at TT$1.85, and investors would purchase or redeem units at that price.

Fixed NAV Funds

A Fixed NAV Fund maintains a stable unit price, regardless of fluctuations in the market value of the underlying investments. Rather than reflecting gains and losses through movements in the unit price, returns are typically distributed to investors through dividends or additional units or a similar mechanism as specified in the fund’s prospectus.

One of the defining characteristics of a Fixed NAV Fund is its low-risk return profile that stems from types of securities in which they invest. Their portfolios are typically concentrated in high-quality, short- to medium-term fixed-income instruments, including government securities, investment-grade corporate bonds and money market instruments. These investments generally provide a predictable stream of interest income rather than sizeable capital appreciation. As a result, Fixed NAV Funds tend to experience significantly lower volatility than equity or balanced mutual funds and generate lower return.

At First Citizens, two flagship mutual funds operate under a Fixed NAV structure. The Abercrombie Fund is a Trinidad and Tobago dollar-denominated fixed-income mutual fund that maintains a constant Net Asset Value of TT$20.00 per unit. Similarly, the Paria Fixed Income Fund, which is denominated in United States dollars, maintains a fixed Net Asset Value of US$10.00 per unit. By maintaining a stable unit price, both funds offer investors a high degree of capital stability while generating returns through income distributions, making them well suited for individuals and businesses seeking to preserve capital, manage liquidity, and earn a competitive return on surplus cash.

Fixed NAV funds are generally favoured by conservative investors, individuals with short-term investment horizons, and those seeking an alternative to traditional savings accounts.

Floating NAV Funds

Unlike Fixed NAV Funds, Floating NAV Funds allow the unit price to rise or fall based on the market value of the underlying investments. As the value of the portfolio changes, the NAV adjusts accordingly, enabling investors to participate directly in both gains and losses. These funds typically invest in equities, bonds, and diversified portfolios of growth-oriented assets. As a result, they offer greater potential for capital appreciation over the long term, albeit with a higher degree of market volatility.

Complementing its Fixed NAV offerings, First Citizens also manages two Floating NAV mutual funds: the Immortelle Income and Growth Fund and the El Tucuche Fixed Income Fund. The Immortelle Income and Growth Fund invests in a diversified portfolio of both equities and fixed-income securities, providing investors with the opportunity to benefit from capital growth while generating regular income. The El Tucuche Fixed Income Fund, on the other hand, invests primarily in a diversified portfolio of high-quality debt securities.

Unlike Fixed NAV Funds, the unit prices of these funds are not fixed. Their Net Asset Values (NAVs) are calculated daily and fluctuate in response to changes in the market value of the underlying investments. As a result, Floating NAV Funds carry a higher level of investment risk and may experience short-term movements in value. However, this additional risk is accompanied by the potential for higher long-term returns through both capital appreciation and income distributions.

The Domestic Mutual Fund Industry and its Evolution

In Trinidad and Tobago, the growth of the mutual fund industry has been driven largely by Floating NAV Funds, as investors increasingly sought opportunities to achieve returns above traditional deposit rates and participate in the long-term growth of financial markets. While Fixed NAV Funds continue to serve an important role in preserving capital and providing liquidity, Floating NAV Funds have become an increasingly important vehicle for investors pursuing long term wealth accumulation.

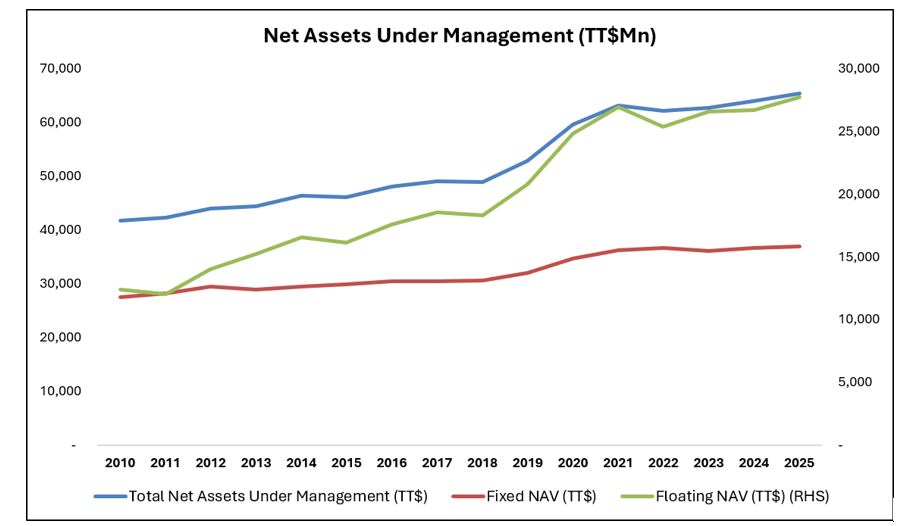

According to data from the Central Bank of Trinidad and Tobago, total assets under management within the domestic mutual fund industry expanded steadily from TT$41.8 billion in 2010 to TT$65.3 billion in 2025. A substantial share of this growth was attributable to Floating NAV Funds, whose assets more than doubled over the period, increasing from TT$12.4 billion to TT$27.7 billion.

Notwithstanding this strong growth, Fixed NAV Funds remain the largest segment of the industry, accounting for approximately 57% of total assets under management in 2025. However, their share of industry assets has gradually declined from 66% in 2010, highlighting a notable shift in investor preferences.

This trend reflects the increasing demand for investment solutions that offer the potential for capital appreciation and long-term wealth accumulation. Unlike Fixed NAV Funds, which primarily focus on capital preservation and income generation and resultantly offers very low returns, Floating NAV Funds allow investors to participate directly in the appreciation of equities and fixed-income securities. As investors have become more focused on growing their wealth and preserving purchasing power over the long term, they have increasingly embraced Floating NAV Funds as a means of achieving these objectives.

The appeal of Floating NAV funds lies in their ability to allow investors to participate directly in changes in the value of the underlying investments. As the market value of equities and fixed-income securities increases, so too does the value of the fund’s units. Consequently, during periods of economic growth, favourable market conditions, and strong corporate earnings, investors in equity and balanced funds have benefited from rising asset prices and enhanced investment returns.

However, investors should also recognize that this growth potential comes with a higher level of investment risk. During periods of economic slowdown, market uncertainty, or weaker corporate performance, the value of the underlying investments may decline, causing the fund’s NAV to decrease. As a result, investors may experience short-term fluctuations in the value of their investment and, in some cases, capital losses. For this reason, Floating NAV Funds are generally most suitable for investors with a medium- to long-term investment horizon who can remain invested through market cycles and allow time for markets to recover from periods of volatility.

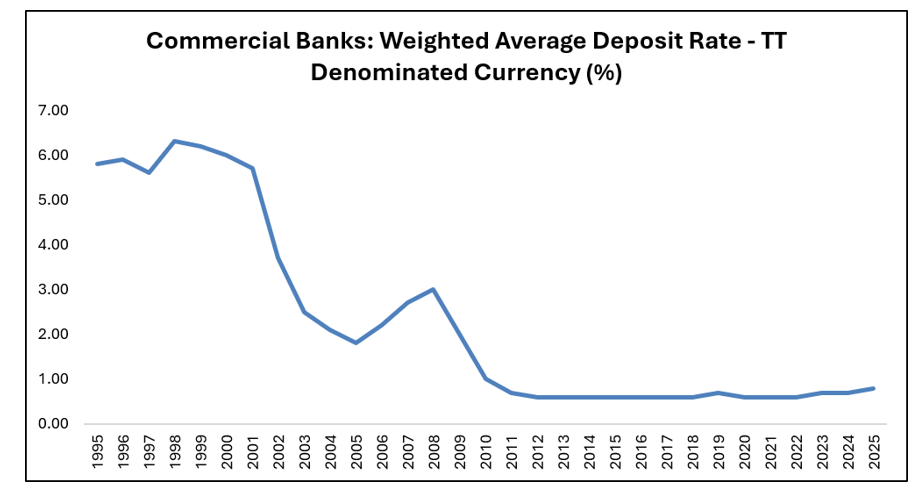

The increasing popularity of Floating NAV funds has also been supported by Trinidad and Tobago’s prolonged low-interest-rate environment. As illustrated in Figure 3, while traditional savings accounts and fixed deposits continue to play an important role in meeting short-term liquidity needs, the prolonged low-interest rate environment failed to keep pace with investors’ long-term financial objectives.

As returns on traditional savings accounts, fixed deposits, and money market instruments remained subdued for an extended period, many investors began seeking alternative investment options capable of generating stronger long-term returns. Floating NAV Funds addressed this need by providing exposure to growth-oriented assets such as equities and longer-duration fixed-income securities, offering investors the opportunity to benefit from both capital appreciation and income generation.

Figure 2: Total Net Assets Under Management

Table 1: Composition of Domestic Mutual Fund Industry

Figure 3: Interest Rates

Investor Considerations

The evolution of the mutual fund industry highlights a broader shift in how investors approach financial planning. In an environment where inflation can gradually erode purchasing power and market opportunities continue to expand beyond national borders, investors are increasingly recognizing the importance of balancing immediate financial needs with long-term financial objectives. The ability to access a wide range of asset classes through a single investment vehicle has become an important consideration for those seeking to build resilient portfolios capable of adapting to changing economic conditions.

For investors, selecting the appropriate mutual fund should be guided by individual financial objectives, risk tolerance, and investment horizon. While Fixed NAV Funds continue to provide stability and liquidity, Floating NAV Funds offer the potential to participate in the long-term growth of local and international financial markets. As every investor’s financial circumstances and goals are unique, it is important to seek professional financial advice before making any investment decisions. A qualified financial advisor can help assess your financial needs, recommend an appropriate investment strategy, and identify the mutual fund or combination of funds that best aligns with your long-term financial objectives.

The NAV structure should not be considered a complete measure of risk. Investors should also examine the fund’s underlying assets, credit quality, duration, currency exposure, liquidity, fees and concentration limits.

As always, investors should adopt a disciplined and diversified approach to investing, recognizing that successful wealth accumulation is not driven by short-term market movements, but by a well-constructed investment strategy that remains aligned with their long-term financial aspirations.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.