Market Review: Second Quarter of 2026

Commentary

International Market Review

Global equity markets rebounded strongly in the second quarter of 2026, recovering from the losses recorded in the previous quarter. The rally was driven by a marked improvement in investor sentiment as geopolitical tensions eased, supported by progress in diplomatic negotiations between the U.S. and Iran that culminated in temporary ceasefires. The reduction in geopolitical risk alleviated concerns over potential disruptions to global energy supplies, leading to a decline in oil prices from their recent highs.

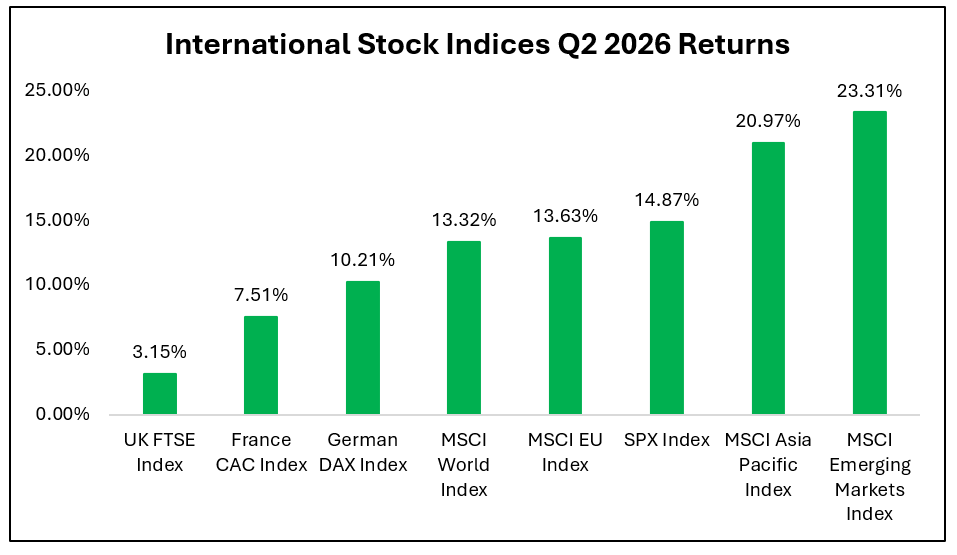

Lower oil prices helped improve the inflation outlook, reinforcing market expectations that major central banks may be able to keep policy interest rates unchanged rather than tightening monetary policy further. Against this more favourable backdrop, investor confidence strengthened, risk appetite improved and global equity markets rallied throughout the quarter. As a result, the losses recorded in the first quarter were reversed, with the MSCI World Index ending the second quarter up 13.32% compared with a loss of 3.88% in the prior quarter.

U.S.

Among the advanced economies, the rebound in the second quarter of 2026 was led by U.S. equities, notably technology stocks. The U.S. market gained momentum from strong earnings reported by mega-cap technology companies, along with renewed confidence in spending on artificial intelligence. Demand remained robust across the AI infrastructure value chain, including AI accelerators, high bandwidth memory chips, advanced networking equipment, cloud computing capacity, data centres, and related power and cooling systems. This strengthened the earnings outlook for key semiconductor and infrastructure suppliers, helping to drive strong share price gains across the technology sector. U.S. equities also received support from a more stable monetary policy outlook.

At its April 2026 meeting, the U.S. Federal Reserve left interest rates unchanged, signalling policy would remain restrictive to contain inflation, while noting that future rate movements were uncertain, given risks to both sides of the mandate. increases were not imminent. This provided investors with greater clarity on the interest rate outlook, improving market sentiment and encouraging renewed investment in equities. Bolstered by resilient corporate earnings, sustained AI investment, and stable monetary policy, both the S&P 500 Index and the NASDAQ advanced to new record highs during the quarter. For the second quarter of 2026, the S&P 500 Index and the NASDAQ index posted returns of 14.87% and 21.41% respectively – the best quarterly performance since 2020.

Europe and the U.K.

European equity markets generated strong gains during the second quarter of 2026 but slightly underperformed the U.S. market as investors remained cautious amid a challenging economic backdrop. For the quarter ended June 2026, the MSCI Europe Index increased by 13.63% while the German DAX and France CAC Index posted gains of 10.21% and 7.51% respectively.

While easing geopolitical tensions and the temporary ceasefires between the U.S. and Iran helped improve global risk sentiment, elevated energy prices weighed on the region’s economic outlook. Europe remains heavily dependent on imported energy, making it particularly vulnerable to supply disruptions and higher energy costs. These elevated prices increased operating costs for businesses, placed pressure on household spending and dampened expectations for stronger economic growth across the region.

Inflation and monetary policy remained the primary drivers of investor sentiment across Europe during the second quarter of 2026. Eurozone headline inflation accelerated to 3.2% in May, up from 3.0% in April, marking its highest level since September 2023 and remaining well above the European Central Bank’s (ECB) 2% inflation target. The increase was largely driven by a sharp rise in energy prices, with energy inflation surging 10.9%, the fastest pace since February 2023, as supply constraints linked to the conflict in the Middle East pushed fuel costs higher.

In response to mounting inflationary pressures, the ECB raised its three key policy interest rates by 25 basis points in June 2026, ending a period of seven consecutive meetings in which rates had been left unchanged. The decision reflected policymakers’ growing concern that elevated energy prices would not only keep inflation higher for longer but also spill over into food, goods, and services prices. Accordingly, the ECB revised upward its inflation forecasts for both 2026 and 2027 to reflect a higher expected path for energy prices.

At the same time, the ECB adopted a more cautious view of the region’s economic outlook. It lowered its growth projections for 2026 and 2027, citing the adverse effects of the Middle East conflict on commodity markets, household purchasing power, and business confidence. Under its latest baseline forecasts, the euro area economy is expected to expand by 0.8% in 2026, before improving modestly to 1.2% in 2027 and 1.5% in 2028.

U.K. equities continued their upward momentum during the second quarter of 2026, with the FTSE 100 Index advancing 3.15%. This marked the index’s strongest quarterly performance in five quarters and extended its winning streak to six consecutive quarters. The rally was driven primarily by strong gains in the aerospace and defense sector, with companies such as Rolls-Royce Holdings and BAE Systems leading the market higher.

Investor sentiment also benefited from moderating inflation, as the U.K.’s headline inflation rate eased to 2.8% in April 2026 and remained at that level in May. The decline was largely attributable to changes in the U.K.’s regulated energy price cap, which temporarily reduced household energy costs. However, this relief is expected to be short-lived, with the energy price cap projected to increase by 13% later in the year, potentially pushing household energy costs to their highest level in two years and renewing inflationary pressures.

Against this backdrop, the Bank of England maintained its policy interest rate at 3.75% during its April meeting. Nevertheless, one member of the Monetary Policy Committee voted in favour of a further rate increase, highlighting ongoing concerns about persistent inflation. The split decision reinforced expectations that monetary policy may remain restrictive for longer, contributing to a more cautious outlook for U.K. financial markets.

Emerging Markets

Emerging market equities delivered the strongest performance among the major global equity markets during the second quarter of 2026, with the MSCI Emerging Markets Index rising by 23.31%. The rally was driven primarily by Asia’s technology sector, as continued global investment in artificial intelligence (AI) fuelled robust demand for semiconductors, advanced processors, memory chips, and other AI-related hardware. For the quarter, the MSCI Asia Pacific Index rallied 20.97%. Strong corporate earnings, coupled with upward revisions to earnings expectations, further strengthened investor confidence and attracted significant capital inflows into the region’s technology companies.

South Korea was one of the standout performers during the quarter, supported by strong gains in global technology leaders such as Samsung Electronics and SK Hynix. Both companies benefited from accelerating demand for high-bandwidth memory chips and advanced semiconductor products that are essential for AI applications and data centers. As expectations for AI-related investment continued to strengthen, investors became increasingly optimistic about the earnings prospects of South Korea’s semiconductor industry, driving the country’s equity market higher.

Taiwan also posted impressive gains, reflecting its critical role within the global semiconductor and AI supply chain. Home to many of the world’s leading chip manufacturers and technology suppliers, Taiwan benefited from sustained demand for advanced semiconductors, chip testing services, and semiconductor manufacturing equipment. Expectations that major U.S. technology companies would continue to invest heavily in AI infrastructure further boosted investor confidence in Taiwanese technology companies.

Source: Bloomberg

U.S Sector Performance

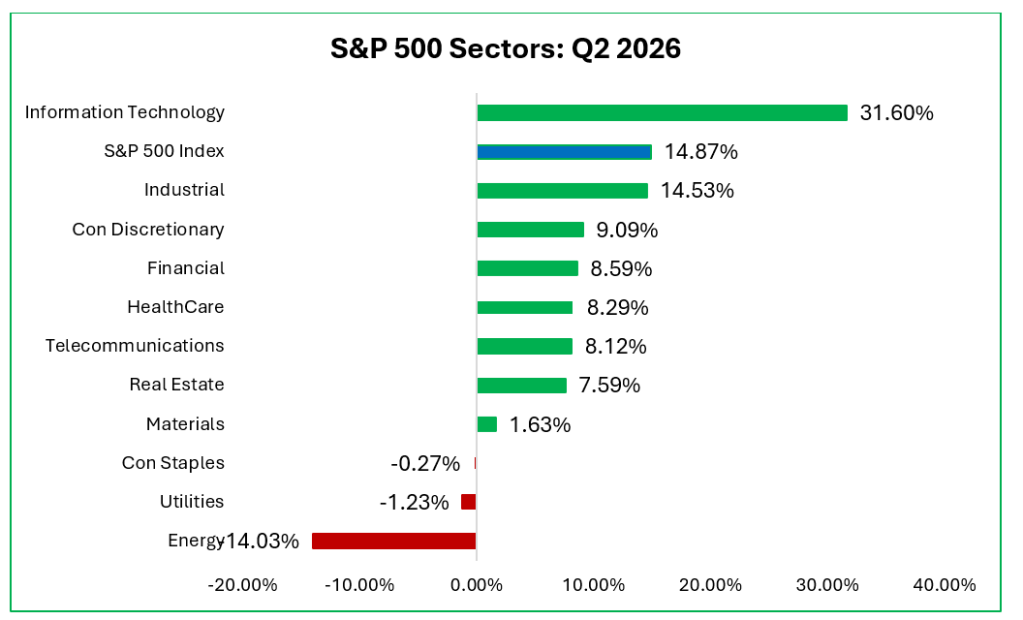

The Information Technology sector reclaimed its position as the best-performing sector in the second quarter of 2026 after being the weakest performer in the first quarter. The sharp turnaround was driven by continued investment in AI infrastructure, both on Earth and in space, which fuelled strong demand for semiconductors, memory chips, networking equipment, and data storage solutions. As a result, companies such as Broadcom, Micron Technology, Seagate Technology, Taiwan Semiconductor Manufacturing Company and Samsung Electronics delivered strong share price gains. For the April to June 2026 period, the Information Technology sector advanced an impressive 31.60%, making it the only sector to outperform the S&P 500 Index. The Industrials sector followed with a respectable gain of 14.5%, while the Consumer Discretionary sector rose 9.09%.

In contrast, the Energy sector experienced a sharp reversal in performance. After leading the market in the previous quarter, the sector became the weakest performer in the second quarter, declining 14.03%. The downturn was largely driven by easing geopolitical tensions, which reduced concerns over global oil supply disruptions and contributed to lower crude oil prices. The sector also came under pressure as investors locked in profits following the strong rally recorded earlier in the year.

U.S. Treasuries

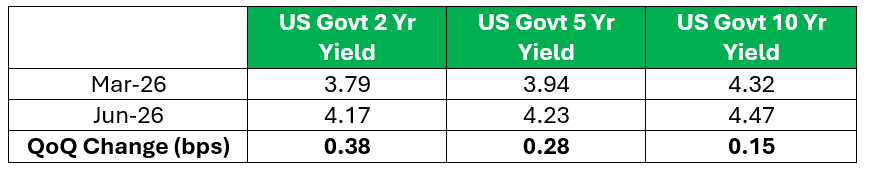

Following the rise in the first quarter of 2026, U.S. Treasury yields extended their upward trend across the curve in the second quarter, supported primarily by persistent inflation concerns and expectations that monetary policy would remain restrictive for longer. Although crude oil prices eased significantly from above USD100 per barrel to around USD68, inflation pressures did not abate as quickly as markets had anticipated, owing to stronger-than-expected consumer spending and increases in rent and medical care costs.

In particular, the Personal Consumption Expenditure (PCE) index, the U.S. Federal Reserve’s preferred inflation measure, rose by 3.8% year-on-year in April, up from 3.5% in March 2026, marking its highest level since May 2023. This reinforced the view that price pressures were proving more stubborn than expected and reduced confidence that the Fed would be in a position to ease policy in the near term.

As a result, market participants increasingly began to price in the possibility that the Fed could maintain a tighter policy stance for longer, or even reverse course and tighten further if inflation failed to moderate. That expectation was reinforced by the April 2026 Federal Open Market Committee (FOMC) communication, which explained the decision to leave rates unchanged by pointing to a solid pace of economic growth, a still-strong labour market, and inflation remaining above the Fed’s 2% target.

Table 1: U.S. Treasury Yields

Local Market Review

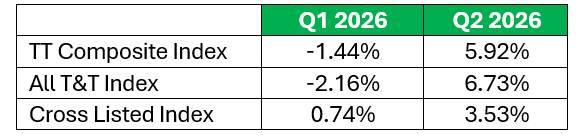

Following a prolong period of declines, the Trinidad and Tobago equity market staged a welcome recovery in the second quarter of 2026, with all three major indices ending the period in positive territory. The All T&T Index led the advance, rising 6.73%, a marked turnaround from its 2.16% decline in the previous quarter. The TT Composite Index also rebounded strongly, gaining 5.92% after falling 1.44% in the first quarter. Meanwhile, the Cross Listed Index extended its positive momentum, delivering a return of 3.53%, an improvement from the 0.74% gain recorded in Q1 2026.

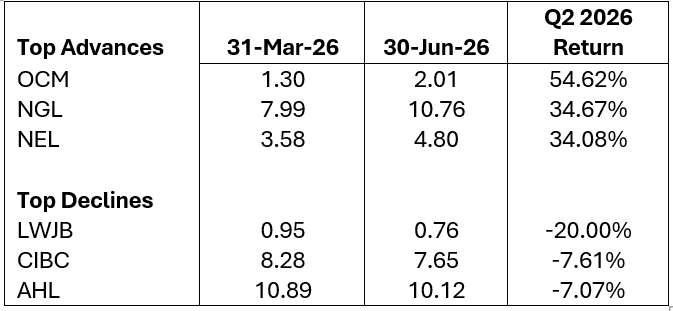

Market participation also strengthened considerably during the quarter. The number of companies recording share price gains increased from 10 in the first quarter to 17 in the second quarter, reflecting a broader-based improvement in investor sentiment. One Caribbean Media Limited (OCM) emerged as the best-performing stock, with its share price surging 54.62% from $1.30 at the end of March to $2.01 by the end of June. Trinidad and Tobago NGL Limited (NGL) followed with a gain of 34.67%, while National Enterprises Limited (NEL) advanced 34.08%.

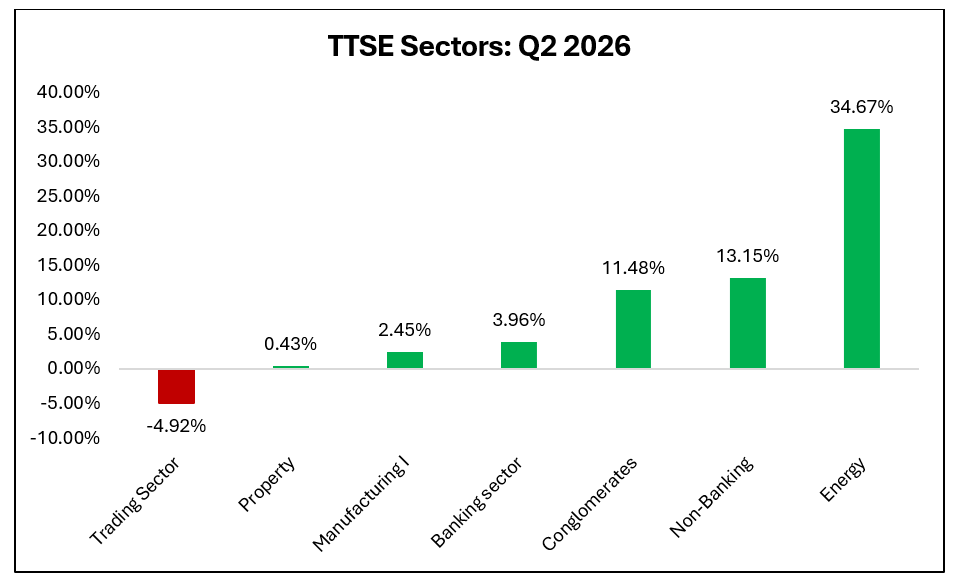

At the sector level, the Energy sector remained the market’s strongest performer, climbing 34.67% during the quarter, supported by the sharp appreciation in NGL. The Non-Banking sector ranked second, posting a solid gain of 13.15%, aided by the strong performance of NEL. In contrast, the Trading sector was the only sector to finish the quarter lower, with the decline primarily driven by weakness in the share price of L.J. Williams Limited.

Table 2: Local Stock Indices Performance

Table 3: Top Advances and Declines: Q2 2026

Figure 3: TTSE Sectors Quarterly Performance

Equity Markets Outlook

Global equity markets are expected to remain supported in the third quarter of 2026, with continued investment in AI infrastructure serving as a key driver of earnings growth. As businesses and governments accelerate AI-related capital expenditure, companies positioned along the AI supply chain are likely to continue benefiting from robust demand.

Despite these favourable structural trends, investors should expect market volatility to remain elevated. Geopolitical risks continue to cast a shadow over the outlook, with repeated breaches of ceasefire agreements between the U.S. and Iran underscoring the fragile security environment. While periodic diplomatic progress has provided temporary relief and supported investor sentiment, the broader geopolitical backdrop remains uncertain. Any renewed escalation could disrupt key global shipping routes, placing upward pressure on energy prices once again and increasing inflationary risks.

Furthermore, the full pass-through effects of higher energy prices have yet to be fully reflected in global inflation data. As these cost pressures gradually work their way through supply chains, major central banks are likely to keep interest rates unchanged while they assess the persistence of inflationary pressures and the evolving geopolitical landscape. Although the AI investment cycle continues to provide a strong foundation for equity markets, investors should remain selective and maintain diversified portfolios, as periods of heightened volatility are likely to persist throughout the upcoming quarter.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgement as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus., offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.