Market Review: First Quarter of 2026

Commentary

International Market Review

The year began on a positive note, with global equity markets advancing through January and February, led by a strong performance in emerging markets, which outpaced their developed market counterparts. Despite this encouraging start, underlying volatility remained elevated, as geopolitical developments quickly became the dominant force shaping investor sentiment.

Early in the year, tensions between the United States and Venezuela escalated significantly, culminating in the capture of President Nicolás Maduro on January 3, 2026, following months of military build-up, sanctions, and targeted operations across the Caribbean. Global tensions intensified further in late February when the United States and Israel carried out coordinated military strikes against Iran. In response, Iran launched attacks on Israel, U.S. military bases in neighbouring countries, and energy infrastructure across several Gulf nations, significantly increasing geopolitical uncertainty and market volatility.

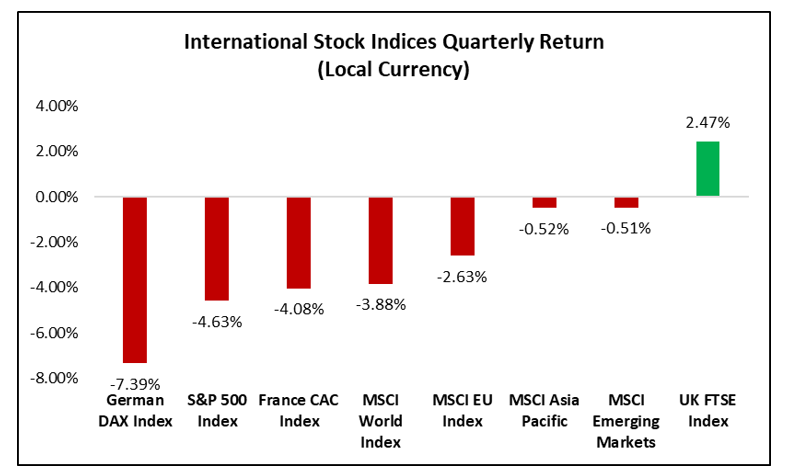

As part of its retaliation, Iran closed the Strait of Hormuz, one of the world’s most important energy shipping routes, through which roughly one-fifth of global oil supply normally passes. The closure triggered a sharp rise in energy prices and has been described as one of the largest disruptions to global energy supply in history. The resulting surge in oil prices and inflation concerns unsettled global financial markets and caused investor sentiment to deteriorate. As a result, the gains recorded earlier in the year were reversed, and global equities ended the quarter in negative territory, with the MSCI World Index declining by 3.88%.

U.S.

U.S. equities began 2026 on a strong note, with the S&P 500 Index surpassing the 7,000 mark for the first time, reaching this milestone just 14 months after crossing 6,000. The rally was driven by continued optimism surrounding artificial intelligence, strong earnings from major technology companies, and expectations that the Federal Reserve would begin lowering interest rates later in the year. Although the Federal Reserve kept interest rates unchanged at its January meeting, investors remained confident that monetary easing would occur in the months ahead.

However, market momentum weakened in February as the S&P 500 declined amid a broad sell-off in technology stocks and rising economic uncertainty. Concerns grew about the potential impact of artificial intelligence on employment, particularly as the labour market began to show signs of slowing. Market conditions worsened further in March as escalating tensions between the United States and Iran significantly weighed on investor sentiment, triggering a sharp equity sell-off and increased market volatility. As a result, for the quarter ended March 2026, the S&P 500 Index declined by 4.63%.

Europe and the U.K.

Europe was not spared from rising geopolitical tensions, as the region found itself drawn into a dispute with the U.S. over Greenland. Investor sentiment weakened amid concerns over potential U.S. tariffs and even the possibility of military intervention should negotiations fail. These tensions later eased as the U.S. and its NATO allies shifted their focus toward cooperation on Arctic security, helping to stabilize market confidence.

Despite these challenges, there were some supportive economic developments. Inflation fell below the European Central Bank’s 2% target in December 2025, reinforcing expectations that monetary policy would remain accommodative. Over the quarter, the euro strengthened against the U.S. dollar, reaching its highest level since 2021, while fourth-quarter growth of 0.3% modestly exceeded expectations.

In the U.K., equities demonstrated greater resilience than both European and U.S. markets. The FTSE 100 Index posted gains in January and February, extending its rally to eight consecutive months, and reached a historic milestone by surpassing the 11,000-point level for the first time in late February 2026. This strong performance was supported by steady corporate earnings and expectations that the Bank of England would maintain a supportive monetary policy stance.

As a result, the FTSE 100 was the only major European index to end the first quarter in positive territory, recording a gain of 2.47% for Q1 2026. In contrast, broader European markets declined over the same period, with the MSCI Europe Index, France’s CAC Index, and Germany’s DAX Index falling by 2.63%, 4.08%, and 7.39%, respectively.

Emerging Markets

The MSCI Emerging Markets Index ended the quarter performing notably better than the MSCI World Index and most major developed market indices, recording only a modest decline of 0.51%. The Index’s relative outperformance was largely driven by strong gains in key Asian markets, particularly Korea and Taiwan.

Korea was the top-performing market within the Emerging Markets Index during the quarter, supported by a rally in memory-related technology stocks and improved investor sentiment surrounding potential corporate governance reforms. Thailand also performed strongly and was close behind Korea, posting double-digit returns in U.S. dollar terms, aided by growing optimism about political stability following the country’s general election. Meanwhile, Taiwan’s performance was supported by continued strength in technology hardware stocks, which benefited from ongoing global demand for semiconductor and technology components.

Figure 1: International Stock Indices Performance (Local Currency Returns)

Source: Bloomberg

U.S Sector Performance

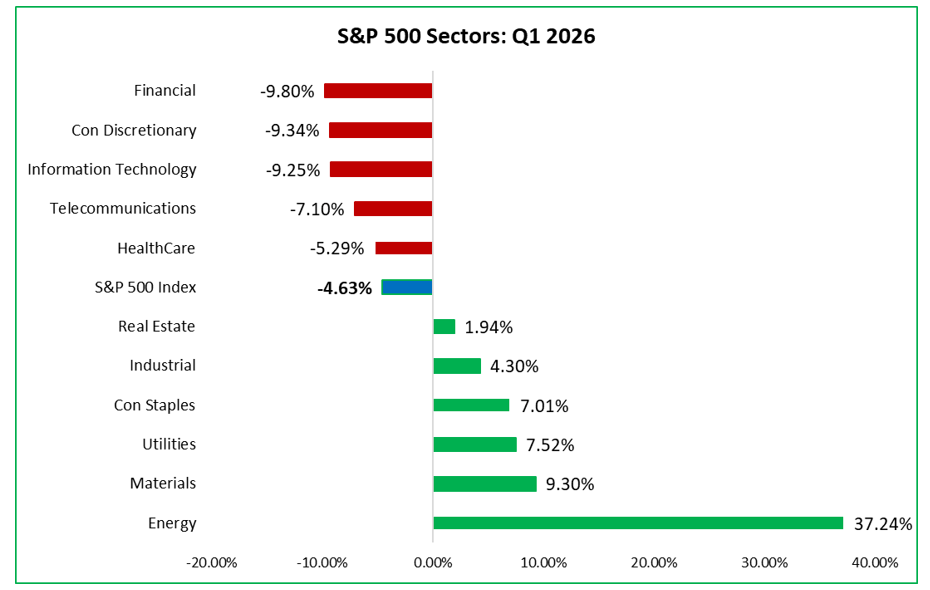

In the first quarter of 2026, there was a clear rotation across sectors within the U.S. equity market. The Energy sector was the standout performer, surging by 37.4%, driven largely by rising oil prices as WTI crude climbed above US$100 amid tensions involving Iran. The Materials sector followed in a distant second, gaining 9.3% in the quarter. Utilities also performed well, rising 7.5%, as the sector benefited from increasing electricity demand, particularly from the rapid expansion of data centres.

In contrast, the Information Technology sector, previously a leading driver of U.S. equity market performance, underperformed in the first quarter of 2026, declining by 9.25%. Investor sentiment weakened amid rising concerns over elevated capital expenditure on artificial intelligence, which has cast uncertainty over near-term returns and heightened the risk of margin compression. The sector’s decline was largely driven by notable share price losses in Microsoft (23.5%), NVIDIA (6.5%), and Apple (6.7%), which together account for approximately 57% of the Information Technology Index.

Figure 2: U.S. S&P Sectors Performance

Source: Bloomberg

U.S. Treasuries

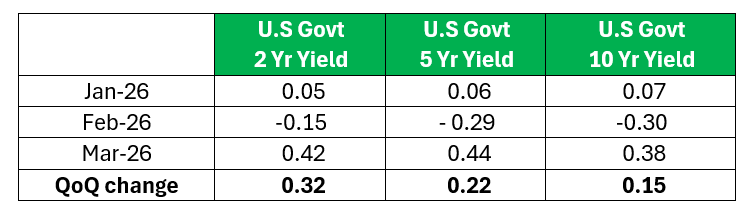

After rising in January, U.S. Treasury yields declined sharply in February as geopolitical tensions intensified. U.S. Treasury securities are widely considered safe-haven assets and typically attract strong investor demand during periods of global uncertainty. During times of crisis, investors often reduce exposure to riskier assets such as equities and move funds into instruments that are viewed as stable and reliable. U.S. Treasuries are regarded as particularly secure because they are backed by the full faith and credit of the U.S. government.

As investors increased their purchases of U.S. Treasuries, the surge in demand pushed bond prices higher. Since bond prices and yields move in opposite directions, the rise in bond prices resulted in lower yields. Consequently, Treasury yields declined during February.

However, this trend reversed in March, when U.S. Treasury yields surged and recorded their largest monthly increase since 2024. The sharp rise in oil prices driven by the Iran conflict fuelled inflation concerns, which began to outweigh the earlier flight-to-safety demand for Treasuries. As oil prices climbed above the US$100 per barrel level, markets began to price in higher inflation risks and the possibility that the Federal Reserve may delay interest rate cuts, leading to the sharp rise in Treasury yields.

Table 1: Change in U.S. Treasury Yields

Local Market Review

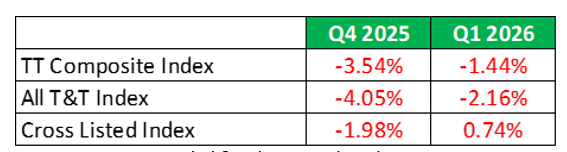

While the major indices continued to trend downward, the pace of decline slowed noticeably in the first quarter of 2026, with losses easing to roughly half the rate recorded in the previous quarter. The All T&T Index led the declines, falling by 2.16% for the quarter, compared to a sharper decline of 3.54% in the fourth quarter of 2025. Similarly, the TT Composite Index declined by 2.16%, an improvement from the 4.05% drop recorded in the prior quarter. The Cross-Listed index was the sole index to end the quarter in positive territory, up 0.74% in Q1 2026 after declining over three consecutive quarters.

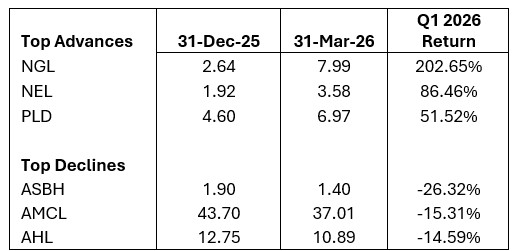

Market breadth also showed signs of improvement. The number of stocks posting quarterly gains doubled in the first quarter of 2026 compared to the previous quarter. Between January and March 2026, ten companies recorded share price gains, up from five in the prior quarter. Trinidad and Tobago NGL (NGL) led the market, with its share price rising by $5.35 following the company’s decision to reduce its stated capital in order to facilitate the resumption of dividend payments to shareholders.

At the sector level, the Energy sector recorded the largest increase, rising by 202.65%, followed by the Non-Banking sector, which gained 9.3% largely due to the surge in NEL’s share price. The Banking sector recorded a modest gain of 0.40%, as higher share prices for RFHL, FCGFH and CIBC were partially offset by a 5.81% decline in SBTT’s share price over the quarter.

Table 2: Local Stock Indices Performance Q1 2026

Table 3: Top Advances and Declines: Q1 2026

Equity Markets Outlook

Looking ahead to the second quarter of 2026, global financial markets are expected to remain volatile as investors continue to navigate geopolitical tensions, elevated energy prices, and uncertainty surrounding inflation and interest rates. The conflict in the Middle East and the disruption to global energy supply have introduced new inflation risks, particularly through higher oil, shipping, and fertilizer prices. As a result, central banks, particularly the U.S. Federal Reserve, may remain cautious in cutting interest rates, which could keep bond yields elevated and equity market volatility high in the near term.

Despite this uncertainty, sector rotation is likely to continue across global markets. Energy and commodity-related sectors may continue to perform well if oil prices remain elevated, while technology stocks may remain under pressure in the short term due to concerns over high capital expenditure and margin pressures. Defensive sectors such as Utilities and Consumer Staples may also attract investor interest as investors seek stability and consistent earnings in a more uncertain economic environment.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus., offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.