Investing Through Uncertainty: Lessons from COVID and the Hantavirus Threat

Commentary

Financial markets have always had a tumultuous relationship with uncertainty. They can price inflation, interest rates and even wars with some degree of rationality. However, pandemics occupy a different category altogether. They are one of the few risks capable of simultaneously disrupting supply chains, consumer confidence, labour markets, travel, trade and political stability. More importantly, pandemics attack something markets depend on heavily, predictability.

Over the past few weeks, headlines surrounding outbreaks of the Andes strain of Hantavirus have started to gain international attention following reports of quarantines arising out of a cruise ship outbreak back in April 2026. The inevitable comparisons to the early stages of the COVID-19 outbreak have begun as the effects of the latter are still very fresh and apparent in the minds of the public. Currently, health authorities like the World Health Organization (WHO) and the Centre for Disease Control and Prevention (CDC) both maintain that the broader public risk remains low. Yet investors would be mistaken to dismiss the economic implications entirely since financial markets do not wait for certainty before reacting – they begin pricing risk the moment uncertainty becomes plausible.

The average investor often assumes that markets respond primarily to events themselves. In reality, markets respond to changes in expectations. A public health crisis does not need to become globally catastrophic to generate volatility. It only needs to create sufficient doubt about future earnings, growth and consumer behaviour.

Global disease outbreaks: Historical Impact on Financial Markets

According to the WHO, a pandemic is the worldwide spread of a new disease. Historically, pandemics have produced surprisingly different market outcomes depending on the underlying economic environment. The Spanish Flu pandemic of 1918 was extremely deadly accounting for roughly 50 million deaths which represented about one third of the world’s population at the time. It occurred during the final stages of World War I which made it difficult to isolate its direct economic effect.

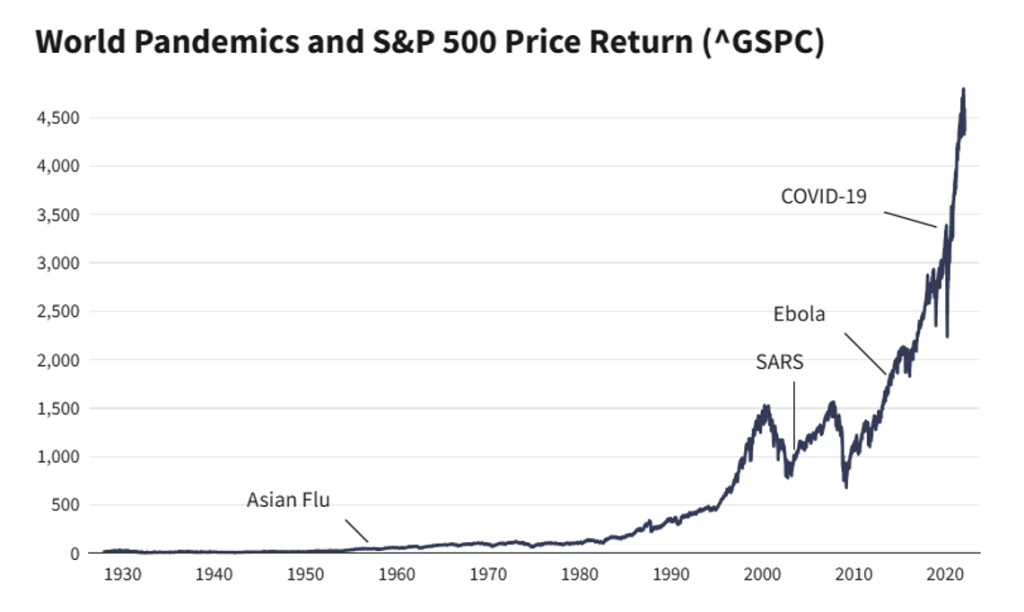

The Asian Flu pandemic which began in China in late 1956 and by October of 1957 was in full swing in the United States (US) was estimated to have killed one – two million people. In 1957, the Dow Industrials peaked on July 12 and then dropped 19.4% to a low on October 22. In this instance the flu pandemic proved to be a leading indicator for the mild recession that then took place in the US economy in August 1957, which reportedly lasted until April of the following year as cited in the Pandemics and Endemics Report published by the Museum of American Finance.

Further, the Severe Acute Respiratory Syndrome (SARS) outbreak which mainly infected China and Hong Kong did not start to affect the financial markets until March 2003 after the Chinese authorities reported the SARS outbreak to the WHO though the initial contagion began five months prior in November 2002. At that time, the S&P 500 lost 12.8% of its value. In addition, the MSCI China Index underperformed compared to its global peers. The outbreak caused significant regional disruptions across Asia but had a relatively muted long-term impact on global equities. It was estimated that SARS caused a global economic loss of USD40 billion, with the world GDP suffering a 0.1% hit.

However, COVID-19 was different. The coronavirus pandemic triggered one of the greatest human and economic consequences the world has ever seen. To date, approximately 779 million were infected with the virus worldwide, with a reported 7.11 million deaths as recorded by WHO Data. In addition, the pandemic was expected to drive most countries into recession in 2020 with the World Bank’s baseline forecast predicting a 5.2% contraction in global GDP potentially becoming the deepest global recession since 1870.

According to the International Monetary Fund (IMF), the global economy contracted by 2.7% in 2020, down from a growth rate of 2.9% in 2019. Despite COVID triggering one of the fastest bear markets in modern history, it was also followed by one of the most aggressive recoveries ever recorded with Global GDP Growth rising to 6.7% in 2021. The S&P 500 not only rebounded but experienced record highs by the end of 2020, registering a 63% increase from its mid-March decline. The index continued to post record gains, up 105% by the end of 2021.

Source: Yahoo! Finance & Federal Reserve Bank of St. Louis via Investopedia

Market participants proved that they were less concerned about the existence of a crisis and more concerned about the policy response to it. During COVID-19, governments and central banks flooded the global financial system with liquidity. Interest rates collapsed toward zero, fiscal spending exploded and asset purchases reached unprecedented levels. The result was an environment where financial assets recovered long before the real economy did. In many ways, the post-COVID bull market became less a reflection of economic strength and more a reflection of abundant liquidity. Ironically, some of the best-performing periods in market history emerged immediately after one of the worst public health crises. This highlights an uncomfortable but important reality for investors, that is economic suffering and market performance are not always aligned. In fact, during periods of extreme fear, markets often begin discounting recovery long before ordinary people feel it. This behavioural disconnect explains why so many investors historically get pandemic investing wrong. Once the fear becomes a reality much of the market decline would have already occurred mostly driven by sentiment itself.

During the early COVID-19 selloff, investor sentiment deteriorated rapidly across nearly every sector before sharply reversing within weeks. Retail investors who panicked and sold near the lows were unable psychologically to re-enter during the recovery phase. Conversely, investors with disciplined allocation strategies and sufficient liquidity were able to capitalize on historically depressed valuations. This in and of itself arises as the most valuable lesson from pandemic investing. Before discussing portfolio construction, however, it is worth understanding what Hantavirus is and whether comparisons to COVID-19 are even appropriate.

Hantavirus

Hantaviruses are a group of viruses, primarily carried by rodents like rats and mice, that can cause severe respiratory and renal illnesses which can lead to death. Although many hantavirus species have been identified worldwide, only a limited number are known to cause human disease. The Andes strain of the hantavirus, largely found in parts of South America, is the only type known to spread person-to-person. Persons can contract the Andes Hantavirus from direct contact with rodents, especially when exposed to their urine, droppings, and saliva. It can also spread through a bite or scratch by a rodent, but this is rare. The virus currently has a mortality rate of approximately 38% according to the Centre for Disease Control and Prevention. Meanwhile, the World Health Organization cites an even higher fatality rate of up to 50% due to Hantavirus Pulmonary Syndrome (HPS), a severe respiratory illness brought on by the virus.

It is important to make a distinction between an epidemic and a pandemic as the way financial markets react is usually tied to the size and spread of the potential health outbreak/crisis. An epidemic is the fast and sudden spread of an infectious disease to a disproportionately large number of individuals in a given population within a short space of time. Whereas a pandemic is an epidemic of a disease that has an unexpected increase in cases and spreads across a large region affecting a substantial portion of the human population.

COVID-19 became economically devastating because of its combination of relatively efficient transmission and asymptomatic spread throughout the population. Hantavirus, while potentially more severe medically in certain cases, does not currently appear to possess the same transmissibility characteristics. Health authorities continue to describe outbreaks as localized and manageable through tracing and isolation measures. If outbreaks increase in frequency or if evidence emerges of broader transmission capabilities, sectors sensitive to mobility and discretionary spending could quickly come under pressure again. Airlines, tourism, hospitality, commercial real estate and discretionary retail would likely experience renewed volatility first.

Globally, economies remain burdened by elevated debt levels, structurally higher interest rates and slower post-pandemic productivity growth. Unlike 2020, policymakers today have less room to respond aggressively. Inflation remains a lingering concern, meaning central banks may not be able to deploy the same level of monetary stimulus without risking renewed price instability. The next pandemic scare may not produce the same “everything rally” that followed COVID-19. Investors assuming that central banks will always rescue markets may be relying too heavily on the last cycle.

Portfolio Positioning

First, investors need to accept that building a resilient portfolio does not necessarily require accurately forecasting the next outbreak but rather acknowledging that volatility itself is inevitable. One of the biggest mistakes investors make during periods of uncertainty is overconcentration. Pandemic environments expose concentration risk. Businesses dependent on physical mobility, leveraged balance sheets or discretionary consumer behaviour can deteriorate rapidly when economic activity slows unexpectedly. Diversification, while often criticised during bull markets for reducing upside gains, becomes extraordinarily valuable during systematic shocks. A resilient portfolio during uncertain periods generally possesses several characteristics but are not limited to:

- Exposure to defensive sectors

- Strong liquidity

- Geographic diversification

- Sufficient cash reserves for opportunistic deployment

Healthcare, utilities and consumer staples historically tend to perform more defensively during economic disruptions because demand for their products remains relatively stable regardless of economic conditions. Information Technology and Communications, both cyclical sectors, can behave differently depending on the nature of the crisis. During COVID-19, digital acceleration massively benefited technology firms as the creation of work from home policies and store front digitization were on the rise.

While investors frequently treat cash as “dead money”, especially in bull markets when it could be employed as a revenue-generating asset, during financial crises it becomes incredibly invaluable as it affords investors the option to purchase quality assets when fear and market sentiment distorts valuation. In practice, investor psychology becomes the real challenge during pandemics as fear alters rational decision-making. During COVID-19 many investors became highly reactive to short-term headlines, infection counts and economic collapse scenarios, yet historically markets have rewarded investors capable of maintaining long-term frameworks during temporary panic. This does not mean that investors should risk or blindly invest during every market downturn because some crises do permanently impair industries and business models. However, discerning temporary dips vs. structural deterioration is key.

For example, during COVID-19, certain airlines and hospitality firms faced existential pressure due to debt burdens and collapsed revenues. Meanwhile, businesses with strong balance sheets and durable competitive advantages emerged stronger because weaker competitors disappeared. Investors should pay close attention to debt levels, cash flow sustainability and refinancing exposure. Companies dependent on cheap borrowing environments become significantly more vulnerable when disruptions occur alongside elevated interest rates

Geographic exposure is another important consideration as emerging markets often experience greater volatility during global crises because of capital flight, currency weakness and weaker fiscal flexibility. Small developing economies can face disproportionate economic stress during pandemic-related disruptions particularly those dependent on tourism or commodity exports.

For the Caribbean region, many economies remain heavily linked to tourism, energy prices and external demand. A severe global slowdown triggered by renewed health concerns could indirectly affect government revenues, employment levels and currency stability even if infection rates locally remain manageable. As a result, individual investors may want to consider maintaining broader international diversification rather than concentrating solely in domestic or regional assets.

Investors with liquidity, patience and strong analytical strategies are often rewarded once stability returns. Perhaps the most overlooked lesson from pandemics is that markets eventually normalize even when the crisis itself feels endless. Surprisingly, the most predictable factor in any major financial disruption is investor behaviour; either their fear or optimism overshoots but in both cases the market overreacts in either direction. At present, there is little evidence to suggest that Hantavirus presents an imminent pandemic comparable to COVID-19 as the WHO characterized the risk as moderate for those exposed in the initial outbreak and low globally, while the CDC described the risk to the US as extremely low. Nevertheless, investors should not interpret low probability as zero probability.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.