How the U.S.–Iran Conflict Has Reshaped Trade Flows in the Middle East

Commentary

The recent escalation in tensions between the U.S. and Iran has underscored how deeply interconnected the global economy has become. While it may appear that the regional geopolitical conflict is isolated to the Middle East, in reality it is more pervasive in nature as it has served to significantly disrupt energy routes and critical shipping corridors.

As conflict rages on somewhat unabated, global trade has adjusted with shipping routes being redirected and the cost of moving goods across borders has increased. Looking beyond the immediate disruptions, the conflict is also accelerating a broader shift in how countries and companies think about trade. Faced with unexpected supply gaps, countries are placing greater emphasis on resilience, security, and strategic partnerships and thus is acting as a catalyst for lasting changes in the structure of global trade.

Disruptions to Trade Flows

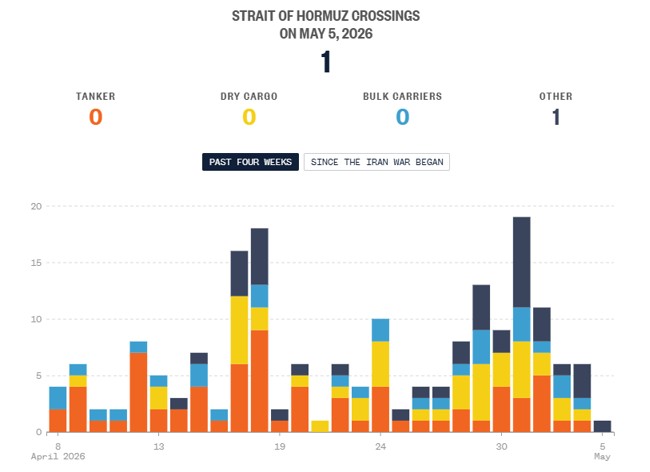

At the heart of this disruption lies the Strait of Hormuz, one of the world’s most critical arteries for oil and gas exports, where even the threat of instability is enough to unsettle markets and delay the movement of goods. While there have been many attempts at ceasefire agreements with the objective of resuming activities in the Strait of Hormuz, it has effectively remained closed to commercial traffic, prolonging a historic supply shock.

Before the full closure, shipping slowed as risks grew. Vessel seizures, attacks, and warnings pushed vessel operators to delay, reroute, or avoid the region altogether. Due to the perceived and actual risk of traversing the Strait of Hormuz, war-risk premiums have risen sharply. War risk insurance is a specialized policy typically covering damage or losses caused by war, terrorism, sabotage, riots, insurrection, or other similar perils, which are usually excluded from standard marine insurance policies. Resultantly, shipowners hiked their freight rates in an effort to compensate for the heightened risk and damage to their vessels.

Heightened uncertainty has begun to redraw the map of global trade. The traditional route linking Asia, the Middle East, and Europe, through the Strait of Hormuz, the Red Sea, and the Suez Canal, once enabled the swift and cost-efficient movement of energy, raw materials, and finished goods. Today, however, shipping lines are increasingly diverting toward longer but more secure routes, most notably around the Cape of Good Hope, in an effort to avoid high-risk zones.

This shift has come at a meaningful cost. Transit times have lengthened by over a week in many cases, fuel consumption has increased, and vessels remain at sea for longer periods, tightening global shipping capacity. The result has been a broad rise in freight rates and a reconfiguration of trade flows. What began as a response to immediate risk is now shaping a more enduring transformation in how goods move across the global economy.

Source: NBC News

The Supply Chain Reconfiguration

The disruption to the Strait of Hormuz has forced a fundamental redirection of global energy flows, as producers and consumers scramble to maintain supply in the face of heightened uncertainty. Governments worldwide have introduced emergency consumer support measures to offset rising energy prices for consumers, including price caps, fuel subsidies, and reduced energy taxes. However, the longer the conflict persists, the more energy prices risk becoming a sustained driver of inflation.

In the physical market, after accounting for alternate routes by major Middle Eastern exporters, the overall supply shortfall still exceeds 13 million barrels of oil per day (mbpd). Countries have turned to survival tactics, with one such tactic sourcing sanctioned Russian oil to bridge the gap temporarily.

Turning to Russia

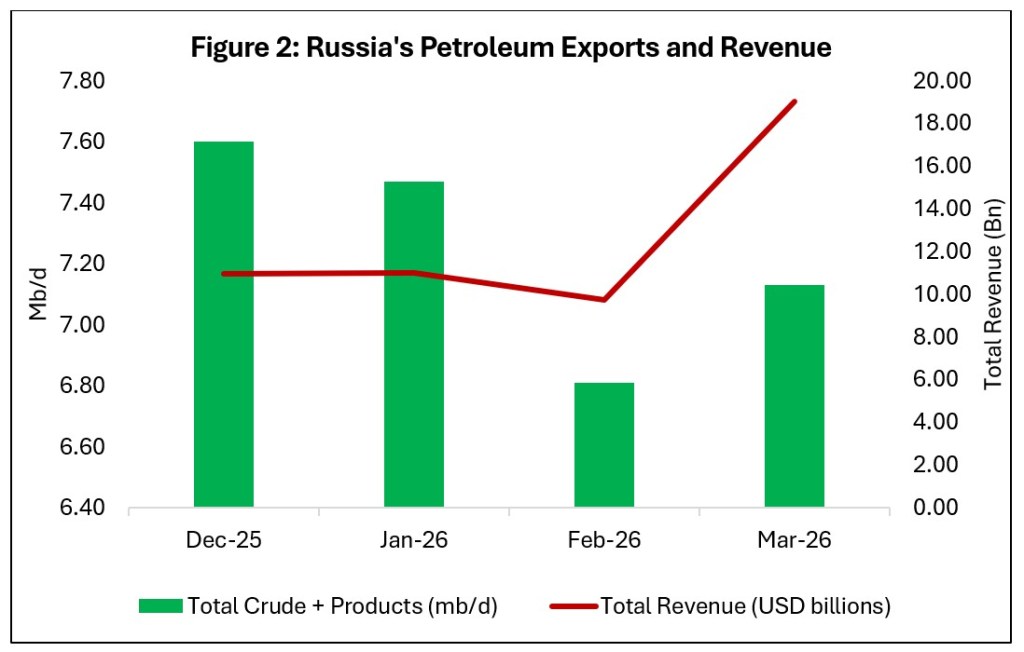

For countries such as India, Indonesia, Vietnam, and the Philippines, national energy security has taken precedence over Western-led sanctions, with Russia emerging as a key alternative supplier. Many Asian nations that previously limited purchases of Russian oil are now increasing imports out of necessity. While historically cautious due to ties with G7 economies, these countries are diversifying toward Russian crude and to a lesser extent U.S. exports to keep refineries operating without rapidly depleting strategic reserves.

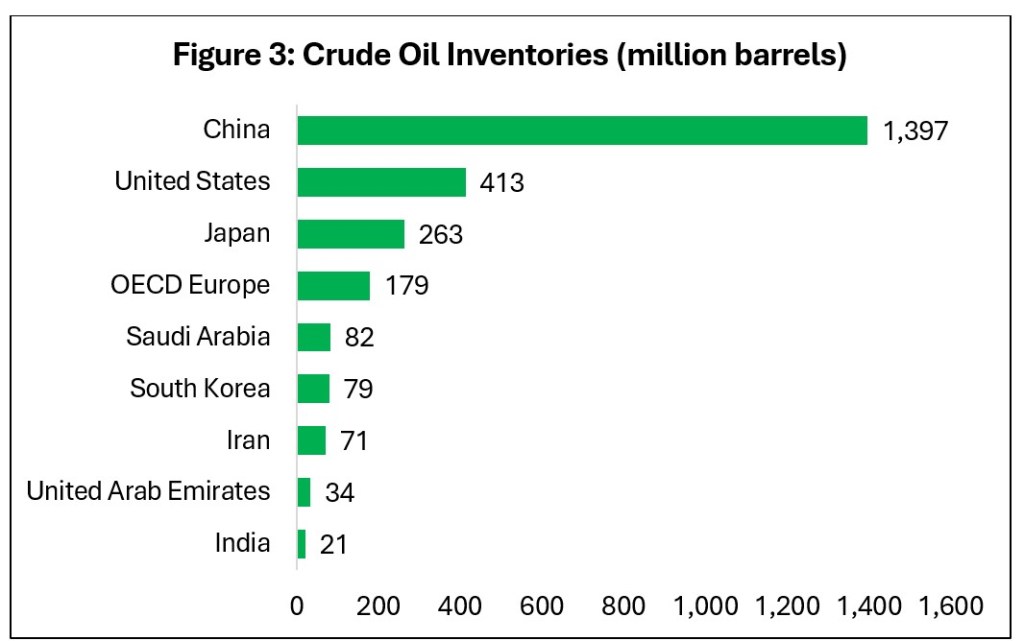

India, with relatively modest strategic reserves of around 21 million barrels, increased its imports of Russian crude to approximately 2 million barrels per day in March 2026. This shift has been supported by a broader domestic refining base, with twelve refineries now configured to process Russian grades, up from just seven previously. Similarly, Indonesia has committed to purchasing roughly 150 million barrels of Russian crude this year.

Other regional players are also deepening energy ties with Moscow. The Philippines recently received its first shipment of Russian oil in five years, with 750,000 barrels delivered to its Bataan refinery, signaling a willingness to diversify supply sources. Meanwhile, Vietnam has taken a more strategic approach, with its leadership engaging directly with Russia to formalize agreements spanning oil, gas, refining, and even nuclear energy. Together, these developments reflect a broader realignment of energy trade flows, as countries prioritize security of supply over traditional sourcing patterns.

The U.S. also eased rules briefly, issuing a temporary 30-day license from 12 March to 11 April 2026. This allowed countries to buy and deliver Russian crude oil and petroleum products already loaded on ships at sea. Building on this, the U.S. Treasury granted a specific waiver on 5 March for India, freeing up Russian oil stuck mid-ocean.

Source: International Energy Agency

Strategic Stockpiling

Unlike India or other Southeast Asian nations, China, Japan and South Korea hold significantly greater Strategic Petroleum Reserves (SPR) that provide a temporary shield during supply shocks. These reserves act as emergency buffers, allowing governments to release stored crude into the market when deliveries are disrupted. In doing so, they help replace missing supply, ease panic buying, and slow the rise in prices.

By 2026, China is estimated to hold about 1.4 billion barrels in combined government and commercial reserves, making it the largest reserve holder in the world. Japan also has one of the world’s largest reserves, with enough supply to cover roughly 150 to 182 days of domestic demand.

On 11 March 2026, the 32 member countries of the International Energy Agency agreed to make 400 million barrels from their emergency reserves available to the market in response to the disruption caused by the war in the Middle East.

Impact on Investors

This conflict has underscored how a fundamental shift in global trade can have ripple effects in several markets and countries. Investors should adopt a more deliberate and selective approach, particularly in sectors heavily dependent on logistics and global supply chains. Companies in manufacturing, retail, automotive, and consumer goods should be assessed through a supply chain resilience lens,favouring those with diversified sourcing, nearshoring strategies and strong pricing power to pass on higher costs.

Additionally, investors must also know the companies with concentrated supplier bases as they will face a heightened risk of supply interruptions. If a firm relies heavily on a single country or a limited number of vendors, any geopolitical shock, transport delay, or regulatory restriction can halt production entirely. This lack of diversification reduces flexibility and can quickly translate into lost revenue and market share.

Knowledge of such factors allows investors to better anticipate earnings volatility, margin compression, and balance sheet stress as it helps to distinguish between companies that are structurally resilient and those that are more fragile. Companies that are more exposed to the volatility associated with the conflict may experience more significant share price declines when compared to firms whose exposure is limited.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.