Financial Inclusion and the Role of Fintech

Commentary

In an increasingly digitalized global economy, financial inclusion has emerged as a critical pillar of economic development. As financial systems evolve, access to affordable and efficient financial services is no longer a luxury, but a necessity for individuals and businesses to participate fully in economic activity. The World Bank defines financial inclusion as a situation in which “individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit, and insurance – delivered in a responsible and sustainable way”.

Financial inclusion is a “development accelerator” that advances multiple Sustainable Development Goals (SDGs), from poverty reduction and gender equality to climate action and inclusive growth. In recent years, a driving force for financial inclusion is the widespread use of Financial Technology (fintech). According to the World Bank’s Global Findex Database 2025, advancements in fintech over the past 15 years have contributed to a significant increase in global account ownership to 79% in 2025, a 28-percentage point increase from the worldwide average of 51% in 2011.

The Evolution of Fintech

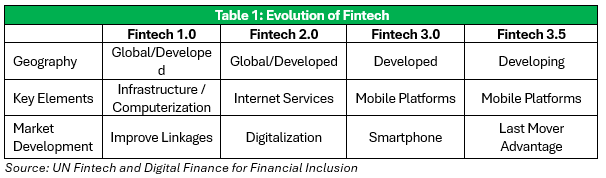

Given the importance of fintech adoption for financial inclusion, it is therefore important to understand exactly what fintech is and how it has developed over time. The United Nations (UN), in its policy brief entitled Fintech and Digital Finance for Financial Inclusion, categorizes the evolution of fintech into four distinct phases, summarized in Table 1:

Fintech 1.0 (1886 – 1967)

Classified as the Infrastructure phase, this time period focused on laying the foundation for key financial technologies including:

- The transatlantic cable – introduced in 1866, it allowed for near instant communication between the US and Europe.

- Fedwire – the first electronic funds transfer system, still used today in the US Treasury market.

- Credit cards – introduced in the US in the 1950s.

Fintech 2.0 (1967 – 2008)

This phase marked the shift from analogue to digital in traditional financial institutions. Key events in this period include:

- Establishment of the NASDAQ (World’s first digital stock exchange) in the early 1970s.

- Establishment of SWIFT in 1973, which continues to serve as a backbone for financial institutions, facilitating large volumes of cross border payments.

- The introduction of online banking and e-commerce (1980s – 1990s)

- Fully digitized internal banking processes at the beginning of the 21st century.

Fintech 3.0 (2008 – Present)

The fallout of the financial crisis in 2008 and the growing distrust of consumers in banks saw the rise of alternate financial technologies to disrupt existing financial processes, including:

- The creation of Bitcoin in 2009, and the launch of cryptocurrencies more broadly.

- Digital payment technologies supported by the growing prevalence of smartphones e.g. Google Wallet, Apple Pay, etc.

Fintech 3.5 (Present), i.e. fintech evolution in developing markets. In this phase, developing markets, particularly China and India accelerated their use of fintech rapidly, and often ‘leapfrogged’ developed markets into more efficient financial solutions, an example of late-mover advantage.

Pandemic-Induced Inclusion

A driving force for the increased momentum in financial inclusion was the COVID-19 pandemic. Pandemic-induced inclusion came as lockdowns, the need for contactless transactions, and governments utilizing digital systems to assist vulnerable citizens, all created significant demand for digital methods of service delivery and access. Despite the significant progress made, the number of adults that remain unbanked globally stands at 1.3 billion according to data from the Global Findex Database 2025.

Regional Financial Inclusion

In the Caribbean, the presence of fintech alone does not guarantee widespread adoption, as multiple factors contribute to variance in the levels of inclusion across countries. In Trinidad and Tobago (T&T), the 2023 National Financial Inclusion Survey conducted by the T&T International Financial Centre (TTIFC) found that 75% of households have access to an account at a financial institution, a decline from 81% in 2017. The TTIFC notes that this decline may indicate a potential rise in financial exclusion. 21% of respondents were unbanked, while the remaining 4% utilized informal means (such as sou sou) for their financial needs.

In Jamaica, a survey done by the Bank of Jamaica (BOJ) in 2022 found that 70.9% of survey respondents had a bank account, while 22.8% were unbanked, and 6.3% were underbanked (Underbanked refers to individuals or families who have a bank account but reported not having used their bank account within the past 12 months).

In the Eastern Caribbean, financial inclusion levels are higher than in T&T and Jamaica. The Financial Literacy and Financial Inclusion Survey Volume II conducted in 2023 by the Eastern Caribbean Central Bank (ECCB) found that financial inclusion for the currency union was 86.1%, with varying levels across member countries. Montserrat had the highest level of financial inclusion at 94.4%, while St. Vincent and the Grenadines had the lowest level at 75.1%.

The Cost of Being Unbanked

The Center for Financial Inclusion notes that over 1 billion unbanked adults live in regions highly exposed to climate risks, making them more vulnerable to environmental and economic shocks. The higher vulnerability to climate events in these regions leads to individuals, typically lower income, feeling the brunt of the impact and having less resources to recover.

Further evidence from the study Cheque In: Increasing Access to the Formal Financial System (2023), conducted by the Caribbean Policy Research Institute (CaPRI), highlights that being outside the formal financial system carries real economic costs. The study focused on Jamaica and found that the unbanked individuals are primarily low-income and minimum-wage earners who face higher transaction costs for everyday financial activities. The combination of direct transaction costs, and productive time loss due to time spent travelling to locations and processing transactions amounted to about JMD6,825 (TTD293 equivalent) per month or “a week’s work for a minimum wage earner.”

Added to this are the long-term opportunity costs of limited access to credit from financial institutions, weak financial resilience, and potential exclusion/difficulty receiving government support which was demonstrated in the pandemic.

Cash Remains King

Despite a significant number of individuals across the region having access to bank accounts, and the growing availability of digital alternatives; cash remains the dominant means of payment in the Caribbean. The National Financial Inclusion Survey 2023 indicates that in T&T, 63% of all transactions are reported to be done with cash. Particular transactions were reported to have a much higher rate of cash utilization; “top-up”/paying phone bills (91% cash utilization), educational expenses (80%) and paying utility bills (80%).

In Jamaica, cash also holds a dominant position in payment method preferences, with 72% of respondents using cash over other methods. Interestingly, the BOJ also found that lower-income households were more likely to use cash than higher-income households, at 74.9%, and 46.2% respectively. In the ECCU, cash also remains king, with 89.2% of respondents across all member countries utilizing cash to make regular and recurring payments. St. Vincent and the Grenadines had the highest percentage cash utilization at 96.9%, while Anguilla had the lowest at 77.6%.

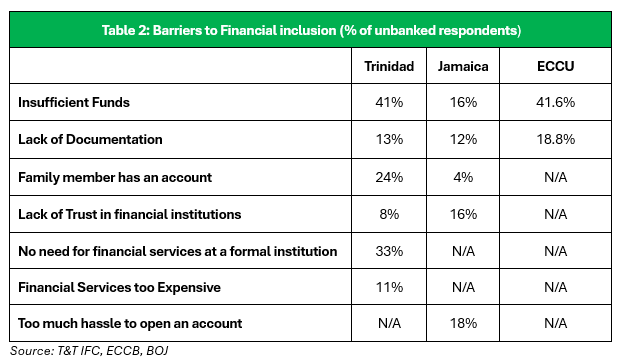

Barriers to Inclusion – Why People Remain Unbanked

Throughout the region, the reasons individuals remain unbanked are largely the same. The surveys in T&T, Jamaica, and the ECCU all highlight insufficient funds to open/maintain accounts, and lack of adequate documentation to meet Know-Your-Customer (KYC) requirements as a recurring factor for an individual being unbanked. Table 2 below summarizes the reasons reported for individuals not having a bank account.

These constraints disproportionately affect low-income and informally employed individuals, limiting their ability to access formal financial services. Additionally, structural issues such as limited financial literacy and the perceived cost of maintaining accounts further reinforce exclusion.

Closing the gap

Efforts to improve financial inclusion are ongoing across the region with central banks and governmental agencies working towards common goals of increasing financial literacy and promoting a digital landscape. The ECCB promotes financial literacy and has encouraged licensed institutions in the bloc to streamline KYC procedures for the establishment of basic accounts through its ECCU First Step Savings Account. The accounts are free to open, do not have maintenance fees or require a minimum balance, and accrue interest at 2% per annum. The ECCB also promotes the use of digital payments with their Central Bank Digital Currency (CBDC), DCash.

The BOJ promotes financial inclusion through promoting digital means, as well as launching the nation’s CBDC, Jam-Dex. Additionally, the BOJ has also been tasked with promoting the National Financial Inclusion Strategy (NFIS) since 2017. Progress in the strategy has been solid thus far, with available data from the BOJ indicating that the number of non-cash transactions increased by roughly 200% to 146.6 million in 2025, and digital utility bill payments rose from 58.4% in 2017 to 83% in 2025.

In T&T, the push to promote financial inclusion from a policy standpoint is relatively new, with the NFIS only being launched in 2024. The responsibility of promoting the NFIS lies with the National Payment and Innovation Company of TT (NPICTT), formerly the TTIFC with collaboration of the Central Bank of Trinidad and Tobago (CBTT). A notable action by the CBTT was a simplification of KYC requirements for basic bank accounts for both individuals and SMEs, and low-value e-money wallets from issuers. The CBTT has also promoted financial literacy since 2007 as part of its National Financial Literacy Programme.

Conclusion

While significant progress has been made in expanding financial inclusion globally, largely driven by fintech innovation, the Caribbean experience highlights a critical gap between access and usage. Despite relatively high levels of account ownership, the continued dominance of cash, and structural barriers, indicate that financial inclusion efforts still have room for improvement.

As the region continues to navigate economic uncertainty and climate vulnerability, strengthening financial inclusion will be essential not only for improving individual welfare, but also for supporting broader resilience.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.