Escalation of the U.S.-Israel-Iran conflict and implications for Financial Markets

Commentary

The Conflict

Rising geopolitical tensions can quickly reshape global financial markets, and the renewed confrontation between the U.S. and Iran in early 2026 is a reminder of how fragile international stability can be. What began as diplomatic pressure and warnings over Iran’s domestic crackdown on protesters escalated into coordinated military strikes by the U.S. and Israel against Iranian military and nuclear infrastructure. The developments have heightened uncertainty in global energy markets, increased security risks in the Middle East and prompted investors to closely monitor potential economic and financial spillovers.

While the current escalation appears sudden, the tensions between the U.S. and Iran are rooted in decades of political rivalry, mistrust and competing strategic interests in the region. Historical events, shifting alliances, and unresolved disputes over security and influence have shaped the relationship between the two nations for more than seventy years.

Historical Context

This feud did not begin in 2026, the origins of the U.S.–Iran divide stretch back much further. In 1953, the U.S. and the United Kingdom supported a coup that removed Iran’s elected prime minister, Mohammad Mosaddegh, after he moved to nationalize Iran’s oil industry, which was under British control. The coup restored Shah Mohammad Reza Pahlavi to power and Western governments supported his regime as a strategic ally during the Cold War.

By the late 1970s, growing frustration among Iranians over corruption, inequality and Western backing of the Shah culminated in the 1979 Iranian Revolution. Ayatollah Ruhollah Khomeini led the movement that ultimately removed the Shah and established the Islamic Republic of Iran. Later that same year, Iranian students seized the U.S. embassy in Tehran and held 52 Americans hostage for 444 days. Although the crisis ended in 1981, it permanently severed diplomatic relations, led to decades of sanctions and entrenched deep mistrust between the two nations.

Financial Market Impacts

Market Volatility

Although tensions between the U.S. and Iran had been steadily rising for months, the scale of the escalation still surprised global markets. Since mid-2025, both countries had intensified their rhetoric following Israeli and U.S. strikes on Iranian nuclear facilities. In January 2026, the U.S. deployed aircraft carriers to the Middle East as a show of force. Despite these warning signs, markets were jolted when coordinated military strikes against Iran were launched on February 28, 2026. The initial market reaction was consistent with what investors typically observe during geopolitical crises.

Periods of conflict often trigger sharp increases in market volatility as uncertainty spreads across financial markets. Investors begin to worry about potential disruptions to global supply chains, particularly energy flows, such as the risk of oil blockades in the Strait of Hormuz. These concerns can lead to rapid price swings across stocks, commodities and safe-haven assets.

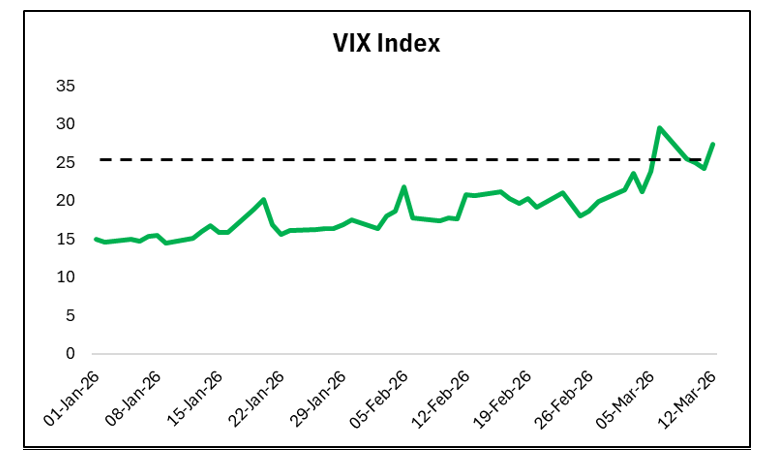

Figure 1: VIX Index (Source: Bloomberg)

In equity markets, volatility is commonly measured by the CBOE Volatility Index (VIX), which reflects investors’ expectations of stock market fluctuations over the next 30 days. Often referred to as the market’s “fear gauge,” the VIX rises when investors rush to buy protection against sudden market declines, as typically occurs during wars, financial crises, or major economic shocks. A VIX level below 20 generally signals calm market conditions, while readings above 25 indicate rising uncertainty. During the current U.S.–Iran conflict, the VIX briefly surged above 25, reflecting a spike in investor anxiety similar to what occurred during past geopolitical events, including the 2022 Russian invasion of Ukraine

Equities

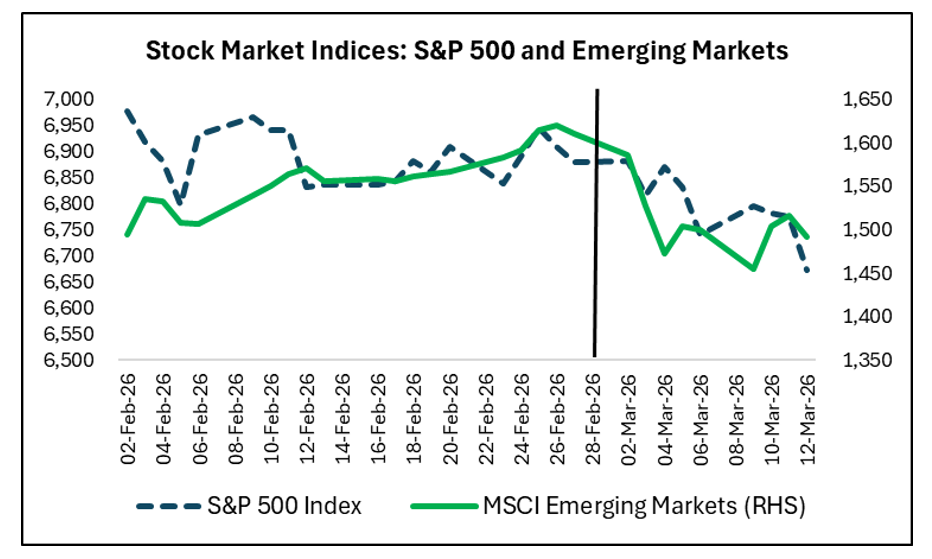

Stock markets often respond to geopolitical tensions with an immediate rise in volatility, as investors move away from riskier assets and seek safer investments during periods of uncertainty. This “flight to safety” can lead to short-term declines in equity markets owing to the rise in selling pressure. However, once the scale and implications of the event become clearer, markets often stabilize and begin to recover. Emerging markets tend to experience steeper declines, often around 2–3%, as these economies generally have fewer financial buffers and are more vulnerable to sudden capital outflows.

A similar pattern has emerged during the current U.S.–Iran conflict. Global equity markets have reacted sharply, driven by a mix of fear-induced selling and selective buying of perceived safe-haven assets. Major U.S. indices such as the S&P 500 have declined by roughly 2% since late February, as investors reduce exposure to riskier stocks amid concerns about higher oil prices, rising inflation, and potential disruptions to global trade through the Strait of Hormuz. Emerging markets have recorded even larger losses, down 8% since the end of February, reflected in the decline of the MSCI Emerging Markets Index.

Geography also plays an important role in how markets react. Countries closer to the conflict or more economically exposed often experience sharper initial shocks. For example, European markets reacted strongly at the start of the Russia–Ukraine war before gradually stabilizing. A similar pattern is evident in the current situation, where U.S. markets, given their direct involvement in the conflict, have experienced larger declines compared with markets in Asia and some parts of Europe.

Historical experience suggests that many geopolitical shocks eventually create opportunities for long-term investors. Once uncertainty begins to ease, markets often recover within three to six months. For instance, the S&P 500 fell about 8% following Russia’s invasion of Ukraine in 2022 but later rebounded as energy markets adjusted and economic conditions stabilized. While major conflicts can produce deeper and longer-lasting market declines, global trade and financial linkages mean that economic spillovers can still affect markets far beyond the immediate region of the conflict.

Figure 2: S&P 500 Index vs MSCI Emerging Market Index

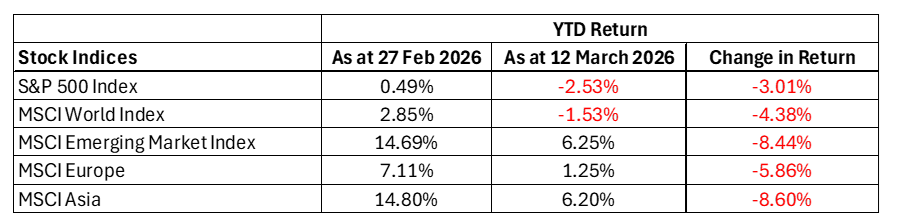

Table 1: Major Stock Indices YTD Return

U.S Treasuries

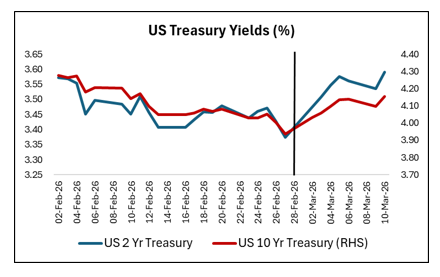

U.S. Treasury securities are widely regarded as safe-haven assets and often attract strong investor demand during periods of geopolitical uncertainty. In times of crisis, investors typically reduce their exposure to riskier assets like equities and shift funds into instruments that are considered more stable and reliable. U.S. Treasuries are viewed as particularly secure because they are backed by the full faith and credit of the U.S. government.

As investors increase their holdings of U.S Treasuries, this surge in demand pushes bond prices higher. Given the inverse relationship between bond prices and yields, as bond prices rises in response to heightened demand, bond yields fall.

Figure 3: US Treasuries (Source: Bloomberg)

Commodities

Energy Sector

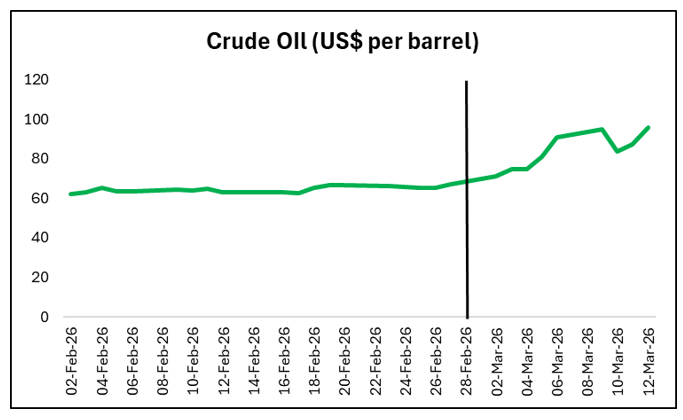

The conflict presents a serious risk to global energy markets. The Strait of Hormuz is one of the world’s most important oil chokepoints, as a large share of global crude oil exports passes through this narrow waterway. According to data from the U.S. Energy Information Administration (EIA), the U.S. government agency that tracks energy markets, oil shipments through the Strait of Hormuz averaged 20.1 million barrels per day in the first quarter of 2025, of which about 14.2 million barrels were crude oil.

Iran has already targeted oil tankers and warned ships against passing through the strait. As a result, several vessels have begun rerouting or avoiding the area, causing shipping traffic to slow dramatically. Reports suggest that movement through the strait has nearly come to a halt. If sustained, this would mark the first effective closure of the Strait of Hormuz in history.

The closure has significant implications for oil-producing countries in the Persian Gulf. Many of these producers rely heavily on the strait to export their crude oil. Without access to this route, they have limited alternatives to move their oil to international markets. If the disruption persists, it could significantly reduce oil supplies from major exporters such as Saudi Arabia, Iraq and the United Arab Emirates, placing upward pressure on global oil prices.

Figure 4: Crude Oil

Gold

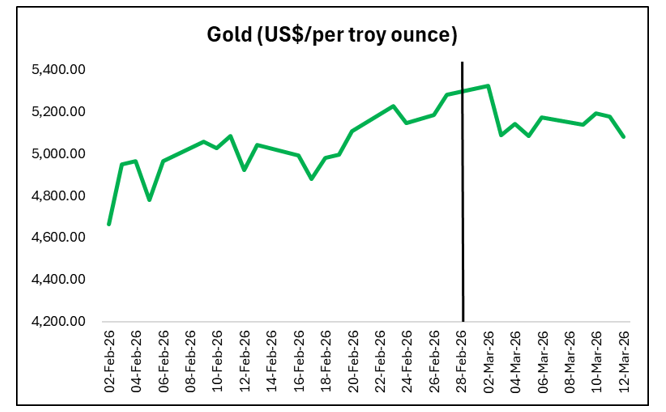

Commodities often serve as safe-haven assets during periods of geopolitical or economic stress. Unlike stocks or bonds, which are financial claims tied to companies or governments, commodities represent physical goods such as gold and silver that hold intrinsic value. Since they are tangible resources that must be mined, refined, or extracted, they tend to retain value even when financial markets become unstable.

During times of conflict or economic uncertainty, investors frequently increase their exposure to commodities as a form of protection. In the current U.S.–Iran conflict, this shift in investor behaviour has contributed to rising commodity prices as demand grows for assets perceived to be more stable. Gold typically leads this movement, as it has long been viewed as a store of value and is often less correlated with stock markets. Silver and platinum may also benefit due to their industrial uses. Together, these assets can help investors preserve value during periods when confidence in financial markets weakens.

Figure 5: Gold Spot Price

Outlook

Historical experience suggests that market declines triggered by geopolitical tensions can often create opportunities for long-term investors. In many cases, markets initially react negatively as uncertainty rises, but once the situation becomes clearer, prices tend to recover over time. As a result, temporary downturns associated with geopolitical events have frequently provided attractive entry points for disciplined investors.

In the near term, however, volatility across both equity and bond markets is likely to remain elevated. Rising inflation, often driven by higher energy prices during periods of conflict, can reduce the real value of the future payments that bonds provide. As a result, investors may demand higher yields to compensate for this inflation risk.

Maintaining a well-diversified portfolio remains essential during uncertain periods. Diversification across regions, sectors, and asset classes helps reduce exposure to sudden shocks in financial markets or the broader economy. Exposure to commodities can also provide a degree of protection against persistent inflationary pressures. At the same time, investors may wish to focus on companies with strong balance sheets, moderate levels of debt, and solid competitive positions within their industries—qualities that better position firms to withstand economic volatility and potential supply-chain disruptions.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus., offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.