Bridge or Backbone? LNG’s Defining Moment in the Caribbean Energy Transition

Commentary

Introduction

The global energy system is undergoing one of the most significant structural transformations in modern economic history as countries pursue net-zero emissions targets while simultaneously confronting energy security risks, affordability challenges, and geopolitical supply uncertainties. Within this transition, liquefied natural gas (LNG) occupies a complex but strategically important position. While renewable energy deployment continues to accelerate globally, LNG remains critical for power generation, industrial use, and grid stabilization, particularly in developing and energy-importing economies. For Trinidad and Tobago, LNG is not simply an export commodity but a cornerstone of economic stability, foreign exchange generation, and industrial competitiveness. As one of the longest-standing LNG exporters globally, Trinidad and Tobago now faces a strategic inflection point which is how to remain competitive in a global energy market increasingly shaped by carbon intensity requirements, environmental transparency, and sustainability-linked financing. Increasingly, LNG is being reframed not only as a bridge fuel, but as a platform for hydrogen development, carbon capture deployment, and low-carbon industrial expansion.

Global LNG Demand Outlook: Structural Growth Despite Climate Commitments

Despite aggressive decarbonization commitments globally, medium-term LNG demand remains resilient due to industrial decarbonization needs and energy security considerations. Global LNG trade reached approximately 411 million tonnes (MT) in 2024 according to the International Gas Union World LNG Report 2025, reflecting continued expansion of global gas trade flows and reinforcing LNG’s role as a key component of the global energy mix. Long-term projections suggest demand could increase significantly, with industry outlooks from Shell estimating that global LNG demand could reach between 630 and 718 MT annually by 2040, representing roughly a 60% increase from current levels. This projected growth is largely driven by Asia’s economic expansion, continued coal-to-gas switching, and the need for lower-emissions fuels in sectors where electrification remains technically or economically challenging. On the supply side, LNG markets are entering another expansion phase, with global supply projected to grow by approximately 5.5% in 2025 and around 7% in 2026 according to the International Energy Agency (IEA) Gas Market Report, marking the fastest supply expansion period since 2019. These dynamics suggest that LNG demand will not disappear during the transition period but will instead shift geographically and technologically, with increasing emphasis on emissions performance and supply chain transparency.

Asia: The Primary Driver of Long-Term LNG Demand Growth

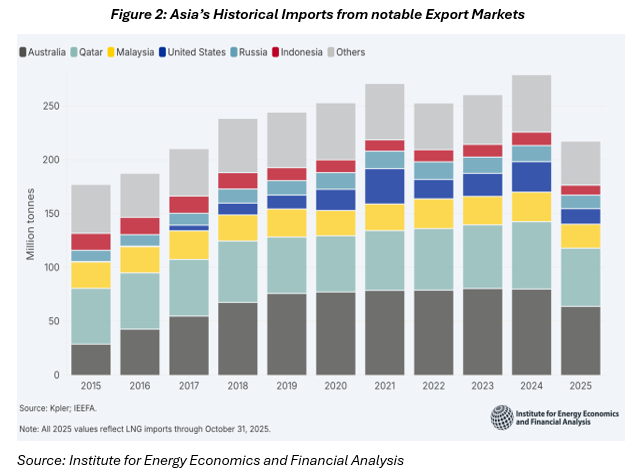

Asia continues to represent the primary engine of LNG demand growth due to structural energy demand drivers and environmental policy shifts. The Asia Pacific region already accounts for the largest share of global LNG imports and is expected to remain the dominant demand centre for at least the next two decades. Demand is supported by continued industrialization, rising urban populations, and government policies aimed at reducing coal consumption to improve air quality. China, India, Japan, and South Korea remain among the largest LNG importers globally, with Southeast Asia emerging as an important secondary demand growth region as countries expand regasification infrastructure. While renewable energy capacity is expanding rapidly across Asia, LNG remains essential for peak demand management, winter heating demand, and industrial feedstock applications. Importantly, Asian LNG demand is becoming more price sensitive and environmentally selective. Buyers are increasingly incorporating lifecycle emissions metrics into procurement decisions, meaning exporters with less carbon-intensive supply chains could gain competitive advantages even if they are smaller producers. For Caribbean exporters, maintaining relevance in Asian markets will require strategic positioning around reliability, pricing flexibility, and environmental performance rather than simply supply availability.

Europe: Security-Driven LNG Demand and Environmental, Social and Governance (ESG) Procurement Shifts

European LNG demand has become increasingly shaped by energy security considerations following disruptions to traditional pipeline gas supply routes. Although LNG imports declined somewhat in 2024 due to high storage levels and improved pipeline supply availability, LNG remains critical for seasonal balancing, industrial energy supply, and grid reliability during periods of renewable intermittency. European buyers continue to pursue long-term LNG contracts to diversify supply sources and reduce geopolitical exposure. At the same time, Europe is emerging as one of the most ESG-focused LNG markets globally. Procurement decisions increasingly incorporate methane emissions monitoring, lifecycle carbon accounting, and environmental certification standards. This shift is transforming LNG into a differentiated commodity market where environmental performance directly influences contract access and pricing structures. For Trinidad and Tobago and other smaller exporters, access to premium European markets will increasingly depend on demonstrating low-carbon production processes and robust emissions monitoring frameworks.

Global LNG Supply Competition: The Rise of Mega-Scale Producers

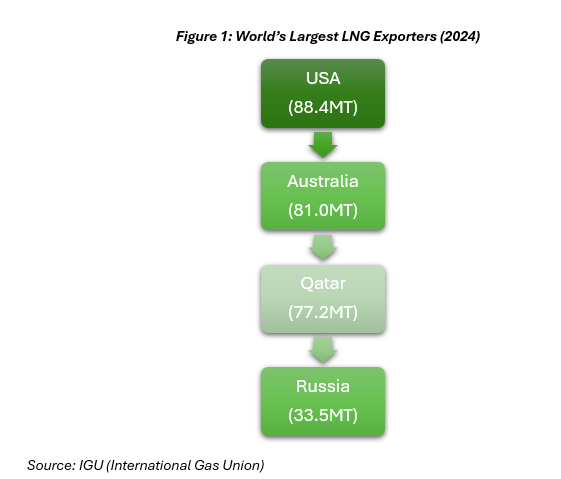

The global LNG supply landscape is becoming increasingly competitive due to large-scale capacity expansions from major producers. Qatar is expected to increase LNG production capacity by approximately 64% to around 126 million tonnes annually by 2027, reflecting the scale advantages of large reserve holders with integrated infrastructure systems. Similarly, North American LNG capacity is expanding rapidly due to new export projects, supported by abundant shale gas supply and flexible destination contracts. These mega-producers benefit from lower production costs, stronger financing access, and economies of scale. For smaller exporters such as Trinidad and Tobago, long-term competitiveness will likely depend less on production volume and more on operational reliability, carbon performance, and supply chain innovation. In the future LNG market, exporters that can demonstrate low methane leakage rates, efficient production systems, and alignment with global sustainability frameworks may remain competitive despite scale disadvantages.

Trinidad and Tobago: LNG as an Economic Anchor and Transition Opportunity

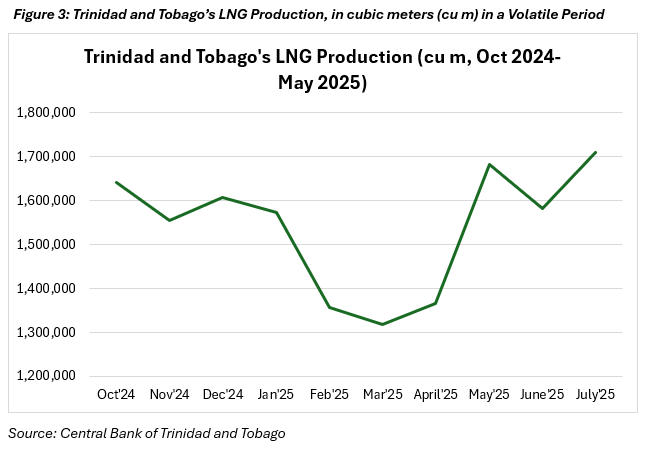

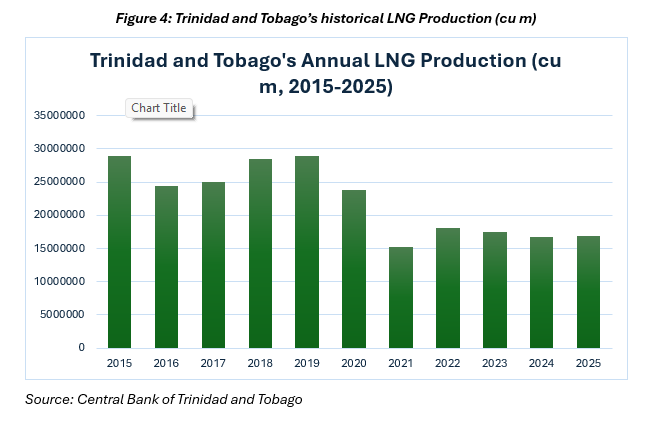

Trinidad and Tobago remains the largest LNG exporter in Latin America, with Atlantic LNG representing the country’s primary export facility and possessing nameplate capacity of approximately 12 million tonnes per annum. However, recent export data highlights structural supply challenges. Atlantic LNG exported approximately 9 million tonnes in 2025, reflecting upstream gas supply constraints and periodic maintenance shutdowns. Monthly production volatility has also been evident, with month-to-month swings exceeding 40% at times, as seen in Figure 3 for the period October 2024- July 2025 where the peak period is May 2025. These fluctuations highlight the importance of upstream gas supply stability, investment in production efficiency, and infrastructure maintenance. From a macroeconomic perspective, LNG remains central to Trinidad and Tobago’s foreign exchange earnings, fiscal revenue generation, and industrial employment. Maintaining LNG export competitiveness is therefore not only an energy policy priority but also a macroeconomic stability imperative.

ESG Pressures: The New Determinant of LNG Market Access

Environmental performance is rapidly becoming a core determinant of LNG competitiveness. Methane emissions monitoring has become a central focus for regulators and LNG buyers due to methane’s significantly higher short-term global warming potential compared to carbon dioxide. Lifecycle carbon accounting is also becoming a standard procurement requirement, with buyers evaluating emissions across the full supply chain, including upstream production, liquefaction, shipping, and regasification. In parallel, access to sustainable finance is increasingly linked to emissions performance metrics. For Caribbean LNG exporters, ESG compliance is transitioning from a reputational consideration to a market access requirement. Exporters that fail to align with emerging environmental standards risk gradual displacement from premium LNG markets even if global gas demand remains stable.

LNG as a Platform for Caribbean Energy Transition and Industrial Diversification

Rather than viewing LNG as a declining industry, Caribbean policymakers are increasingly viewing LNG as a transition anchor capable of financing new energy sectors. LNG revenues can support investment in hydrogen production, renewable integration, carbon capture infrastructure, and low-carbon industrial clusters. This transition model allows hydrocarbon exporters to gradually diversify their energy mix while maintaining economic stability and fiscal resilience. For the Caribbean, LNG infrastructure could evolve into multi-purpose energy hubs supporting hydrogen exports, carbon management services, and renewable-gas hybrid energy systems.

Strategic policy priorities may include developing carbon pricing readiness frameworks, providing incentives for Carbon Capture and Storage (CCS) pilot projects which refers to climate technology used to reduce emissions from natural gas and LNG production, strengthening methane monitoring regulations, and supporting low-carbon industrial investment. Workforce transition planning will also be critical as future energy systems require new technical skills across hydrogen production, carbon capture operations, and renewable energy integration. Public-private partnerships will likely play an important role in financing transition infrastructure and accelerating technology deployment.

Conclusion

LNG will likely remain a core component of the global energy mix throughout the transition period, particularly for regions requiring reliable and flexible fuel supply. However, the definition of LNG competitiveness is evolving. Carbon performance, environmental transparency, and technological adaptability are becoming as important as cost and supply reliability. For Trinidad and Tobago and the wider Caribbean, LNG represents both a strategic risk and a significant opportunity. If leveraged strategically, LNG can evolve from a bridge fuel into a catalyst for energy innovation, supporting hydrogen exports, carbon management industries, and low-carbon industrial development. In a decarbonizing global economy, the most successful energy exporters will not necessarily be those that produce the most gas, but those that most effectively integrate hydrocarbons into broader clean energy ecosystems. For the Caribbean, LNG offers not only continuity but also a pathway toward long-term economic transformation and energy transition leadership.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.