Between a Lock and a Dry Place: The Panama Canal Under El Niño

Commentary

Introduction

The Panama Canal remains one of the most strategically important arteries in global trade, facilitating approximately 3%-5% of global maritime commerce and accommodating roughly 14,000 vessel transits annually under normal operating conditions. However, unlike most global infrastructure, the Canal is uniquely dependent on climatic conditions. Its operations rely entirely on freshwater availability, making it highly vulnerable to hydrological shocks. This vulnerability was sharply exposed during the 2023-2024 drought, when the El Niño climate cycle disrupted rainfall patterns across Central America and caused severe constraints on canal operations, causing severe economic implications not only for Panama but for the world.

The Panama Canal as a Hydrological System

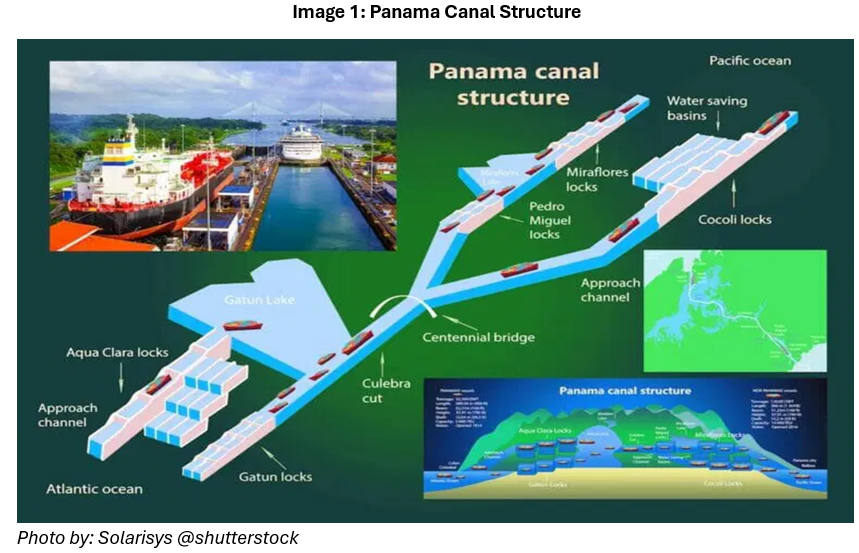

The Panama Canal is built across an isthmus, a thin piece of land that connects two larger land areas and separates two bodies of water. In this case, it connects North and South America while separating the Atlantic and Pacific Oceans, this can be seen in Image 1. Rather than being a flat waterway, the canal uses a system of locks, which are like ‘water elevators’ for ships. These locks raise ships up to Gatùn Lake and then lower them back down to the other side. The entire system depends on freshwater from this lake. Each time a ship passes through, large amounts of water are used to move it through the locks and because of this, rainfall is critical. Under normal conditions, Gatùn Lake reaches about 88ft in height, which allows the canal to operate at full capacity. This level determines both how many ships can pass through each day and how much cargo each ship can carry.

El Niño and Rainfall Suppression

The influence of El Niño on this system operates through a well-established climatic mechanism. El Niño is characterized by the warming of sea surface temperatures in the central and eastern Pacific Ocean, which alters atmospheric circulation patterns and suppresses rainfall across parts of Central America. In 2023, this effect was particularly pronounced. October 2023 alone recorded 41% less rainfall than normal, marking the driest October observed since 1950. This deficit significantly reduced inflows into Gatùn Lake and triggered a rapid deterioration of water availability.

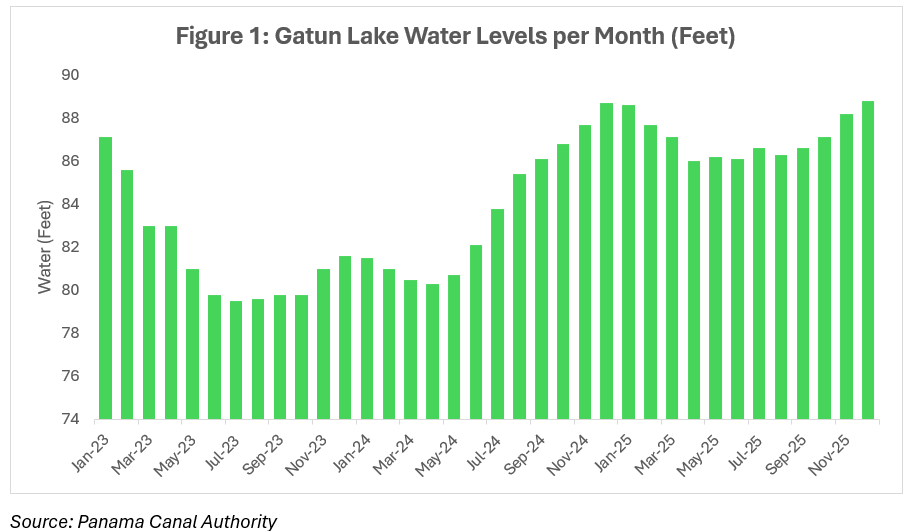

The hydrological impact of this rainfall shortfall was immediate and measurable. In August 2023, water levels in Gatùn Lake fell to 79.6 feet as referenced in Figure 1, well below the typical operational level of approximately 88 feet. On 1 January 2024, lake levels were nearly 6 feet lower than those observed at the same point in 2023, underscoring the severity of the drought. These levels placed the canal system under significant operational stress, forcing authorities to implement restrictions to preserve remaining water reserves.

Congestion and Shipping Delays

The most immediate response was a reduction in daily vessel transits. Under normal conditions, the canal accommodates approximately 36 ships per day. However, by late 2023, this number had been reduced to 22 vessels per day and by early 2024 capacity was further constrained to just 18 vessels per day, representing a reduction of approximately 50% relative to standard operating capacity. In parallel, the Panama Canal Authority imposed draft restrictions, limiting the depth at which vessels could operate. As a result, ships were required to carry less cargo per transit, reducing the efficiency of each voyage and compounding the overall impact on throughput.

These operational constraints quickly translated into congestion within the canal system. At the peak of the 2023 disruption, more than 160 vessels were waiting to transit with delays extending to as much as 21 days in some cases. Under normal conditions waiting times typically range between one and two days, highlighting the scale of the disruption. The backlog created a bottleneck in global shipping networks, forcing carriers to either absorb delays or seek alternative routes.

Trade and Economic Implications

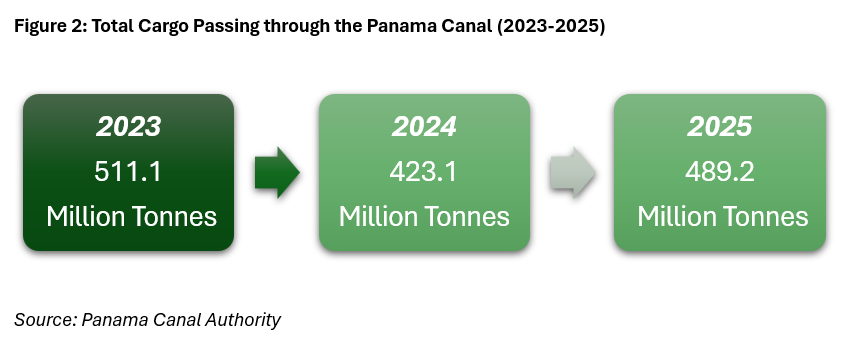

The economic implications of these disruptions were significant. In fiscal year 2024, average transit declined to 27 vessels, down from approximately 36 vessels in the previous year per day. Total cargo throughput fell to 423 million tons in 2024 down from 511.1 million tonnes in fiscal year 2023 as referenced in Figure 1, reflecting the combined effects of reduced transit capacity and draft restrictions. Shipping companies responded by rerouting vessels along longer paths, including around the Cape of Good Hope, which increased transit distance and fuel consumption.

These adjustments raised transportation costs and reduced the efficiency of global trade flows. The impact was not limited to shipping volumes. Draft restrictions meant that vessels could not operate at full capacity, effectively increasing the cost per unit of goods transported. This reduction in efficiency, combined with longer transit routes, contributed to upward pressure on freight costs. In turn, these higher logistics costs had the potential to feed into broader inflationary dynamics, particularly for goods transported along key Asia to North America trade routes.

Conditions began to improve in 2024 as climatic patterns shifted away from El Niño. Increased rainfall replenished Gatún Lake, allowing water levels to recover. By August 2024, water levels had risen to approximately 85.4 feet, and continued precipitation throughout 2025 restored the system to near-normal operating conditions. By early 2026, daily transit capacity had returned to approximately 36 vessels, and full draft levels of 50 feet were reinstated for larger vessels. Canal revenues also rebounded, reaching approximately USD5.71 billion in fiscal year 2025 as traffic volumes recovered as compared to the USD4.97 billion in 2024.

Ongoing Risks and Structural Vulnerabilities

Despite this recovery, the events of 2023 to 2024 highlighted a structural vulnerability within the Panama Canal system. The canal’s reliance on rainfall introduces a direct link between climate variability and global trade capacity. When water levels fall below critical thresholds, operational restrictions are implemented rapidly, resulting in immediate reductions in throughput. This creates a non-linear risk profile, where relatively small changes in rainfall can lead to disproportionately large disruptions in trade flows.

As of May 2026, water levels in Gatún Lake have approached approximately 86.2 feet, indicating a return to stable conditions. However, the underlying risk remains. El Niño events occur periodically every two to seven years, and their impact on rainfall patterns in Central America is well documented. This suggests that similar disruptions could re-emerge in future cycles, particularly in the context of increasing climate variability.

Conclusion

The broader implications for global trade are significant. The Panama Canal serves as a critical chokepoint, and its disruption can have cascading effects across supply chains, shipping costs, and trade flows. Recent tensions affecting other strategic maritime corridors, such as the Strait of Hormuz, further highlight how vulnerable global commerce remains to disruptions in key waterways. Together, these events underscore the extent to which international trade depends on a small number of highly strategic passages, where climate events, geopolitical tensions, or operational disruptions can quickly ripple across the global economy. The experience of the recent drought has prompted a reassessment of logistics strategies, with some firms diversifying routes and incorporating climate risk into operational planning. At the same time, the Panama Canal Authority has begun exploring long-term solutions, including the development of additional water storage infrastructure to mitigate future shortages.

Ultimately, the recent disruption underscores the growing intersection between climate dynamics and economic infrastructure. The Panama Canal is not only an engineering achievement but also a climate-dependent system whose performance is increasingly shaped by environmental conditions. As global trade continues to rely on critical maritime corridors, the ability to manage and adapt to climate-related risks will play an increasingly important role in ensuring the stability and efficiency of international commerce.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.