Barrels on the Brink: How Geopolitical Shifts are influencing Prices

Commentary

Why Oil Prices Matter More Than Ever

Oil has shaped the global economy for more than a century. It fuels the cars people drive, the planes that connect continents, and the ships that transport goods across oceans. Even as the world gradually moves toward renewable energy, oil remains deeply embedded in modern life. Because of this, changes in oil prices affect far more than the energy sector. They influence transportation costs, food prices, inflation and ultimately the pace of global economic growth.

In recent months, oil markets have entered another period of uncertainty. Brent crude, the global benchmark for oil prices, has risen toward USD90 per barrel, while West Texas Intermediate (WTI), the U.S. benchmark, has traded above USD80 per barrel. These price movements are not the result of a single event. Instead, they reflect a complex set of developments happening across the global energy system at the same time, with recent gains of approximately 10%–15% over the past few months.

Geopolitical tensions in the Middle East, disruptions to major shipping routes, the ongoing consequences of the Russia-Ukraine war, production decisions by the Organization of the Petroleum Exporting Countries (OPEC), and the possible return of additional oil supply from countries such as Venezuela are all influencing the balance between global supply and demand. Together, these geopolitical shifts are playing a central role in determining the direction of oil prices and the future stability of global energy markets.

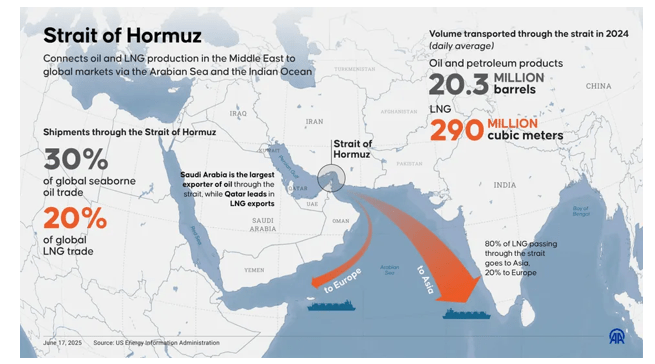

The Strait of Hormuz: The World’s Most Important Oil Route

At the centre of today’s energy tensions lies a narrow stretch of water known as the Strait of Hormuz. Located between Iran and Oman, the strait connects the Persian Gulf to the open ocean. Despite being only a few dozen kilometres wide at its narrowest point, it serves as one of the most critical arteries in the global energy system.

Every day, roughly 20% of the world’s oil supply (approximately 17–20 million barrels per day) passes through this passage. Oil tankers carrying crude from major producers such as Saudi Arabia, Iraq, Kuwait, and the United Arab Emirates must travel through the Strait of Hormuz before reaching international markets. The strait also handles a large share of global shipments of liquefied natural gas (LNG).

Due to such a large portion of the world’s energy supply flowing through a single location, any disruption to shipping in the Strait can quickly send shockwaves through global markets. Even the possibility of disruption can push oil prices higher. Traders often react immediately when tensions rise in the region because they fear that millions of barrels of oil per day could be temporarily removed from global supply. This vulnerability explains why the Strait of Hormuz has long been considered one of the most strategically sensitive locations in the global energy system.

The Iran Conflict and the Risk to Global Supply

Recent tensions involving Iran have brought renewed attention to the risks surrounding the Strait of Hormuz. Military activity and rising regional tensions have raised concerns that oil shipments through the Persian Gulf could be disrupted. Even without an actual shutdown of shipping routes, markets often react strongly to the possibility that supply could be affected. Oil prices frequently rise during periods of heightened geopolitical tension because traders anticipate potential shortages. Analysts studying the current situation suggest that markets have already built a geopolitical risk premium of approximately USD5–USD10 per barrel into oil prices. In other words, part of the recent increase in prices reflects fears about what might happen rather than actual supply disruptions.

The disruption in the Strait of Hormuz has extended beyond energy markets, evolving into a broader supply challenge, particularly within the global fertilizer market. A critical input in fertilizer production is liquefied natural gas (LNG), which is used to produce ammonia and, ultimately, urea, one of the main components of nitrogen-based fertilizers. According to the International Fertilizer Association, approximately 34% of global urea trade and 23% of ammonia trade passed through the Strait in 2024, largely from key exporters such as Iran, Qatar, Saudi Arabia, the UAE, and Bahrain.

Figure 1: The Strait of Hormuz Oil and LNG Flow (Source: Forbes)

The near closure of this vital shipping route is especially disruptive for fertilizers because, unlike oil, there are no significant stockpiles to cushion supply shocks. The industry operates largely on a just-in-time basis, with production and distribution closely aligned to planting cycles. As a result, inventories are not designed to absorb prolonged geopolitical disruptions. With constrained access to key inputs, several producers have begun scaling back output, placing upward pressure on urea prices and, by extension, global food prices.

Should tensions escalate further and restrict shipping for an extended period, the effects could be far-reaching. Energy analysts suggest that a sustained disruption could push oil prices above USD100 per barrel, particularly if a meaningful portion of global supply is removed from the market. This highlights a fundamental characteristic of oil markets: prices respond not only to actual supply shortages, but also to the perceived risk of disruption.

LNG and the Growing Interconnection of Energy Markets

Another major development shaping the global energy landscape is the growing role of liquefied natural gas (LNG) as a bridge fuel in times of geopolitical upheavals. When geopolitical tensions disrupt natural gas supplies, such as during the Russian invasion of Ukraine. countries often turn to LNG markets to secure alternative fuel supplies.

This shift was starkly evident in Russian invasion of the Ukraine as this conflict significantly disrupted the global natural gas market. Before the war, many European countries relied heavily on pipeline gas from Russia to power homes, industries, and electricity generation. When the conflict began, sanctions and political tensions led to sharp reductions in Russian gas flows through key pipelines such as Nord Stream 1.

This created an urgent energy supply gap across Europe and nations turned to LNG tankers from the U.S, Qatar and Australia. As a result, European nations began importing record volumes of LNG, with imports increasing by over 60%–70% and invested heavily in new LNG terminals and floating storage facilities to increase their capacity to receive these shipments.

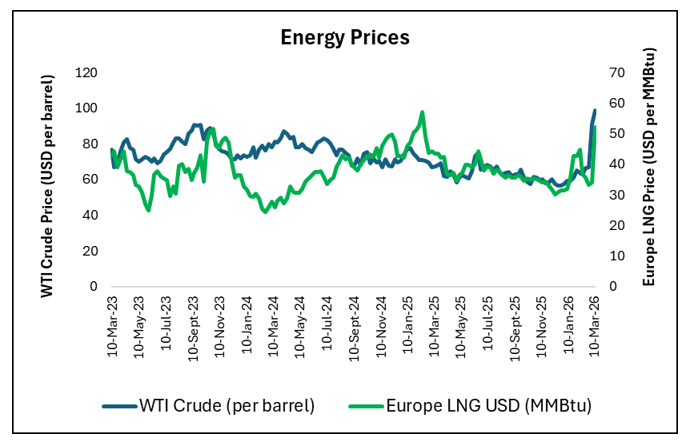

This sudden increase in demand for LNG created spillover effects into oil markets. As Europe rushed to replace Russian gas with LNG imports, global natural gas prices rose significantly. This surge in prices prompted fuel switching to oil to power plants and industries, which tightened oil supply and lifted prices further. Given the ripple effect, LNG contracts are often tied to oil prices and geopolitical tremors in one usually stirs volatility across the entire energy sector.

As shown in Figure 3, both crude oil and LNG prices rose following the outbreak of conflict in late February. This increase in LNG prices has been further supported by stronger demand from the fertilizer industry, adding additional upward pressure on prices.

Figure 2: Crude Oil Prices vs LNG Prices

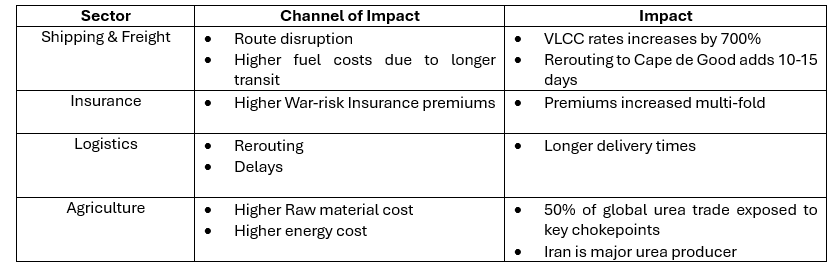

Spillover effects of the Conflict on Consumer Prices

The supply shocks triggered by the U.S.-Iran conflict could increase consumer prices around the world and temper global economic growth. According to the International Monetary Fund (IMF), a 10% rise in energy prices can push up global inflation by 40 basis points and slow global economic growth by 0.10% to 0.20%.

The U.S.–Iran conflict and the disruption of the Strait of Hormuz place immediate upward pressure on oil prices, as a significant share of global energy supply flows through this critical route. Any constraint, whether real or perceived, tightens supply and pushes prices higher. This increase feeds directly into inflation, as higher fuel costs raise transportation, electricity, and production expenses across the economy. Businesses, in turn, pass these higher costs on to consumers, resulting in broad-based price increases.

At the same time, the disruption extends into the fertilizer market, where liquefied natural gas (LNG) is a key input for producing ammonia and urea. Reduced availability of LNG drives up fertilizer production costs, leading to higher prices for farmers. As agricultural producers face rising input costs, food prices begin to increase, contributing to a more persistent and widespread form of inflation that directly affects households.

Table 1: Business Impact Overview

Compounding these pressures are rising maritime and shipping costs. Heightened geopolitical risk increases insurance premiums, fuel expenses, and the likelihood of rerouting vessels, all of which raise the cost of global trade. This leads to more expensive imports and supply chain delays, further adding to inflationary pressures. Together, higher energy prices, rising food costs, and increased shipping expenses create a powerful combination that drives inflation across multiple sectors of the global economy.

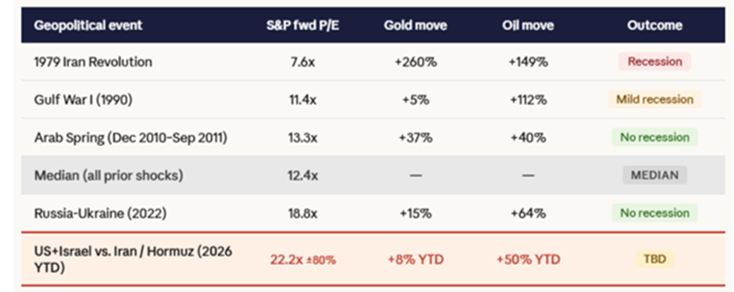

Historical Context: How Markets Have Reacted to Oil Shocks

Past oil shocks have produced varying economic outcomes depending largely on starting market conditions, particularly valuation levels and the scale of the price shock.

Historical episodes such as the 1979 Iran Revolution and the Gulf War (1990) were characterized by sharp oil price increases of approximately +149% and +112%, respectively, and were followed by recessionary or near-recessionary outcomes. Notably, these events occurred when equity market valuations were relatively low, with forward P/E ratios ranging between 7.6x and 11.4x.

More recent events, including the Arab Spring and the Russia-Ukraine conflict, saw more moderate oil price increases of ~40% to 64%, with no recessionary outcome. These periods also coincided with higher starting valuations, suggesting that the magnitude of the shock and the resilience of global demand both play a role in determining outcomes.

However, current conditions appear more stretched. Equity markets are now trading at approximately 22.2x forward earnings, around 80% above historical starting points, while oil prices have already increased by roughly +50% year-to-date. Gold prices have also risen modestly, reflecting growing demand for safe-haven assets.

This combination of elevated valuations and rising energy prices suggests that markets may be more vulnerable to sustained shocks than in previous cycles. Unlike earlier periods, where lower valuations provided a buffer, the current environment leaves less room for absorption, increasing the risk that prolonged energy price pressures could translate into broader financial and economic strain.

Figure 3: Historic Geopolitical events and the outcome

What Could Happen Next: Possible Oil Price Scenarios

Looking ahead, the future direction of consumer prices will depend largely on how the current geopolitical tensions and supply dynamics evolve. Energy markets are currently navigating a delicate balance between supply risks and the possibility of new production entering the market. With oil demand remaining relatively strong worldwide, even small disruptions or supply increases can have a noticeable impact on prices.

One possible outcome is that geopolitical tensions ease and operations in the Strait of Hormuz normalizes, easing supply pressures. In such a scenario, steady production from OPEC+ together with continued output from the U.S. and other major producers could help maintain a balanced market. If global economic growth remains moderate and demand expand steadily, oil prices may stabilize at levels that support producers (~$75-$90 per barrel), while avoiding excessive pressure on consumers.

Another scenario involves continued instability in key energy-producing regions. If tensions in the Middle East intensify or shipping through the Strait of Hormuz remains restricted over an extended period of time, global oil supply could tighten quickly, which will also impact the agriculture sector. Since a significant share of the world’s oil passes through this corridor, even temporary disruptions could cause prices to rise sharply as markets react to the risk of shortages.

If the U.S-Iran conflict persist, there is a high likelihood that oil, fertilizer, shipping, and insurance costs will remain elevated and global economic growth may face increasing headwinds in the medium term.

In such an environment, investors should focus on building resilient portfolios that can withstand both inflationary pressures and heightened volatility. Diversification across asset classes, regions, and sectors becomes critical, as different assets respond differently to rising costs and geopolitical risks. Exposure to real assets, such as commodities and energy, can provide a natural hedge against inflation, while investments in companies with strong pricing power and resilient balance sheets may better navigate rising input costs. At the same time, maintaining a prudent allocation to high-quality fixed income can help cushion portfolios against potential economic slowdowns and market dislocation.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus., offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.