An Investor’s Perspective on a Possible AI Bubble

Commentary

Understanding Artificial Intelligence (AI)

Artificial Intelligence (AI) is the capability of computers and machines to perform tasks typically associated with human intelligence such as learning, reasoning and decision-making. It simulates cognitive functions like problem-solving and perception through algorithms and data processing. AI operates by processing vast amounts of data using techniques like machine learning, where algorithms identify patterns without explicit programming for every scenario. Models are trained on datasets, then refined through feedback loops to enhance accuracy in tasks such as image recognition or language understanding.

AI is not a single technology but rather encompasses a broad field that includes several key areas. These include Machine Learning (ML), Deep Learning, Natural Language Processing (NLP) and Computer Vision. Machine Learning involves creating models by training an algorithm to make predictions or decisions based on data. According to Google Cloud, imagine teaching a computer to recognize a bird by showing it thousands of bird pictures; it would then learn what a bird looks like on its own. Next, Deep Learning, which is a subcategory of ML, focuses on utilizing multilayered neutral networks to achieve classification, regression and representation learning with the specific use of performing complex tasks like image and speech recognition. NLP enables computers to understand, interpret, and generate human language. Lastly, Computer Vision is the ability to analyse visual information.

Over the past decade, advancements in machine learning and neural network architectures have transformed AI from a niche research field into a foundational technology reshaping industries from healthcare and finance to manufacturing and retail. The rapid traction of tools like generative AI has accelerated corporate adoption, drawing unprecedented capital into the AI ecosystem.

The AI Bubble

The AI bubble refers to a theorized period of stock market speculative overvaluation in AI-related stocks fuelled by massive investments in AI technology, via both investors in publicly listed tech companies and these same companies in the research and development of their own AI technologies, echoing that of the dot-com era. As with anything else there are technological cycles, where hype and capital influx can outpace real-world revenue generation. In financial economics, a bubble occurs when asset prices significantly exceed their intrinsic value, driven largely by expectations of future growth rather than present earnings, cash flows or realistic growth prospects. Historically, the closest comparison to today’s AI surge is the dot-com bubble (1995 – 2000), when internet-related firms experienced massive valuation spikes before collapsing in early 2002. Importantly, bubbles do not imply that the underlying technology lacks value.

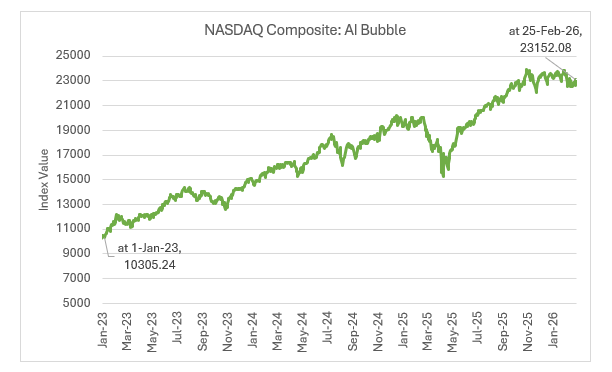

In the context of AI, commentators and market participants began referencing an “AI bubble” following sharp valuation increases in 2024–25, coinciding with outsized speculative bets on AI-related assets and concerns that many firms were yet to demonstrate meaningful revenue tied to their AI initiatives. The AI boom onset in late 2022, followed ChatGPT’s public release in November of that year, which ignited investor fervour. Valuations surged through 2023 – 2025, with the NASDAQ-100 rising over 100% amid AI enthusiasm, peaking concerns by mid-2025 as central banks noted “stretched” metrics reminiscent of the dot-com era.

For example, in early 2025, volatility in stocks like NVIDIA highlighted worries that some parts of the market were pricing in overly aggressive future earnings expectations rather than validated adoption trends. Leading players in the AI space dominate via hardware, cloud, and models. NVIDIA rules chips, Microsoft integrates via Azure and Copilot, Alphabet advances search/cloud AI, Amazon boosts AWS, and Meta invests in open models. NVIDIA, the Graphics Processing Units (GPUs) powerhouse, saw its market capitalization exceed USD3 trillion by late 2025, fuelled by AI chip demand, embodying the “funding feedback” where capital owners reinvest gains.

The “Magnificent Seven” tech giants like Microsoft (via OpenAI stake), Alphabet (Google DeepMind), Amazon (AWS AI services), Meta Platforms, Apple, and Tesla, account for over 30% of S&P 500 by weight, with AI capital expenditure projected at USD200 billion annually until 2030. Startups like Anthropic, xAI, and Databricks raised billions in venture funding, often at unicorn valuations (valuations at extraordinary high values typically greater than USD1 billion) without profits, but backed by enterprise pilots showing 10–40% productivity gains in narrow tasks. Hyperscalers’ (such as large cloud service providers or data centers) circular investments, tech firms buying each other’s AI services, also raise bubble flags as future growth appears to be propped up by mounting expenditures which are yet to be directly reflected in profitability margins.

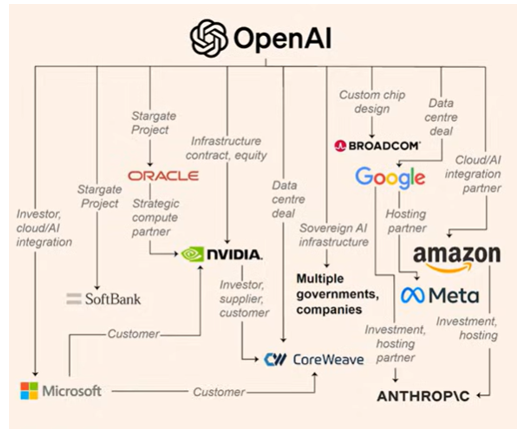

The graphic below illustrates one instance of the close linkages among some top players in the AI space highlighting the possibility of contagion with respect to the financial performances of this corporations

Despite valid concerns by market analysts, several leading companies have continued to deliver strong financial performance:

NVIDIA Corporation stands at the forefront of the AI infrastructure market. In recent reporting, NVIDIA posted very strong steady top-line growth driven by data centre and AI chip demand, with revenues and profits far outpacing broader tech peers.

Other players broadly linked to the AI theme include Broadcom Inc. and Intel Corporation. Broadcom is positioned to benefit from custom silicon growth, while Intel’s AI engine and processor roadmap contributes to durable long-term demand dynamics, albeit with more modest stock performance compared to pure AI hardware specialists

Across the broader market, AI-linked stocks have outperformed traditional indices in recent periods, occasionally delivering multi-hundred-percent returns for standout names. Yet this rapid appreciation underscores why some investment strategists emphasize valuation discipline, when growth expectations are priced too aggressively relative to revenue realization, the risk of a correction increases.

The dot-com Bubble

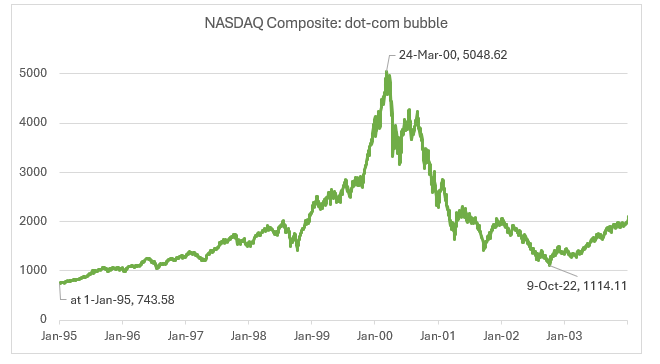

The dot-com bubble refers to the rapid rise and fall of technology stocks, especially internet startups, during the late 1990s. Investors poured money into companies with “.com” in their names, often regardless of whether those businesses had profits, sustainable revenue models, or even finished products. The primary stock index associated with the bubble was the NASDAQ Composite, heavily weighted toward technology companies. Between 1995 and March 2000, the NASDAQ rose nearly 675%. At its peak in March 2000, valuations of many internet startups were astronomical despite minimal earnings.

The bubble roughly lasted from 1995 to 2000, with the collapse beginning in March 2000 and continuing through 2001–2002. The broader economic fallout overlapped with a mild recession in 2001. This era coincided with rapid public adoption of the internet, personal computers, and e-commerce. The excitement around a “new digital economy” led many to believe traditional business fundamentals no longer applied.

Rising U.S. interest rates in 1999-2000 made borrowing costlier, drying up cheap money. Many firms reported first losses, revealing unprofitable models reliant on endless funding. Panic selling hit after the NASDAQ peak, amplified by profit warnings from leaders like Microsoft. By 2002, over USD5 trillion in market value evaporated with hundreds of dot-coms vanishing – over half of public internet firms ceased trading by 2001, bankrupt or acquired for scraps. Pets.com, Webvan, and Boo.com became cautionary tales of overexpansion.

Amazon survived near-death, pivoting to profitability by 2003. The crash spurred a recession, job losses in tech (especially Silicon Valley), and stricter investor scrutiny on fundamentals. However, the collapse also cleared the field for stronger businesses weeding out weak players, paving the way for Web 2.0 giants like Google and sustainable e-commerce. Companies like Amazon and eBay survived by refining their operations and focusing on profitability. Surviving infrastructure firms like Cisco endured major stock declines but remained operational.

In the long run, the internet revolution did materialize, but more slowly and sustainably than investors had imagined. The dot-com bubble became a cautionary tale about speculation, overvaluation, and the importance of business fundamentals.

Investor Pros and Cons: How to take advantage of the bubble?

Navigating the current AI boom requires managing asymmetric risk in a hype‑driven and highly uncertain environment. If the AI expansion since 2022 does contain bubble‑like characteristics, history shows that investors can still benefit provided their approach is disciplined, diversified and grounded in fundamentals rather than speculative momentum.

One effective method is prioritizing the “picks and shovels” segment, where infrastructure firms such as NVIDIA, Advanced Micro Devices (AMD) and cloud hyperscalers like Microsoft and Amazon generate more durable demand than speculative AI‑application startups. These companies serve the entire ecosystem and are therefore less dependent on the success of any single model, offering a more resilient exposure even at elevated valuations.

Momentum‑based strategies also appeal to quantitative investors, who seek to ride upward trends while controlling downside risk through trailing stop‑loss triggers or reducing exposure during periods of heightened volatility. Though this cannot predict the top of a bubble, it enables participation in gains while imposing structural guardrails against rapid reversals. Complementing this, pairing high‑growth AI assets with defensive holdings such as cash, treasuries, or value stocks, a strategy referred to as a barbell allocation, helps balance upside potential with stability, reflecting portfolio‑theory principles that favour diversification over concentration in volatile sectors.

Crucially, investors who focus on cash flow rather than market sentiment tend to fare better during market corrections. Companies with strong balance sheets, positive free cash flow, and clear revenue pathways historically survived cycles like the dot‑com bust, even when their stock prices temporarily collapsed. Applying this lens to AI involves scrutinizing data‑center capital expenditure sustainability, margins on AI services, revenue concentration, and customer‑retention metrics all of which are factors that indicate whether growth is supported by real economics.

Finally, recognising that AI, like railroads, electricity, or the internet, may experience a long productivity lag can help investors maintain balanced exposure. Rather than making all‑or‑nothing bets, gradually adjusting allocations allows participation in long‑term structural gains while mitigating vulnerability to a sudden correction. Monitoring slowing revenue growth, declining data‑center orders, regulatory shocks, or AI‑service price compression provides early warning signals. Ultimately, the objective is not perfect market timing but resilient positioning in an evolving and potentially volatile technological cycle.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment, or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.