The Russian Oil Price Cap And Its Impact On The Energy Markets

Insights

Russian forces began their full-scale invasion of Ukraine on 24 February 2022, almost ten months ago. In response to the unprovoked and unjustified attack on Ukraine, several countries including the United States (US), European Union (EU) and the United Kingdom (UK), imposed sanctions against Russia. Sanctions are penalties imposed by one country on another with the aim to stop them from acting aggressively or breaking international law and fall into several categories including economic, diplomatic and sports sanctions. Such actions can be levied against governments, companies and individuals.

The sanctions imposed on Russia thus far targets both its financial and energy sectors. The US effectively barred Russia from making debt payments using foreign currency held in US banks, while major Russian banks were removed from the international financial messaging system- SWIFT. In addition, the UK excluded major Russian banks from its financial system, froze assets of all Russian banks, barred Russian firms from borrowing money and placed limits on deposits Russians can place at UK banks.

As it pertains to individuals, sanctions were imposed on roughly 1,000 Russian individuals and businesses who are thought to be close to the Kremlin. Assets of the President and Foreign Minister were also frozen in the US, EU, UK and Canada.

As it pertains to the energy sector, many western nations have banned or will ban over the short-term the import of Russian oil, gas and refined oil products. The latest sanction was effective from December 2022, with the EU, Australia and the G7 nations implementing an oil price cap on Russian crude oil transported by ships.

How does the Oil price cap work?

On 2 December 2022, the highly anticipated price cap on Russian oil was implemented at USD60 per barrel. The announcement comes after the Group of Seven (G7) countries, which is an intergovernmental political forum consisting of Canada, France, Germany, Italy, Japan, the UK and the US, agreed earlier in September to impose a limit on Russian seaborne crude. This price cap applies to crude oil, petroleum oils, and oils obtained from bituminous minerals which originate in or are exported from Russia.

The oil price cap prevents firms in the participating countries from providing shipping, insurance, trading and brokering shipments of Russian crude oil once sold above the stipulated price. If the crude has been sold above USD60, the companies and countries will be held liable for violating the sanctions.

The capped price is intended to achieve the following: (1) maintain a reliable supply of seaborne Russian crude oil and petroleum products to the global market, (2) reduce upward pressure on energy prices and (3) reduce Russia’s revenues.

The price cap is expected to be reviewed periodically to adapt to the market situation. The functioning of the price cap mechanism will be reviewed every two months to respond to developments in the market, and will be set at least 5% below the average market price for Russian oil and petroleum products. This will be calculated based on data provided by the International Energy Agency. Each change in the cap will be unanimously agreed by all 27 countries of the European Union and then by the G7.

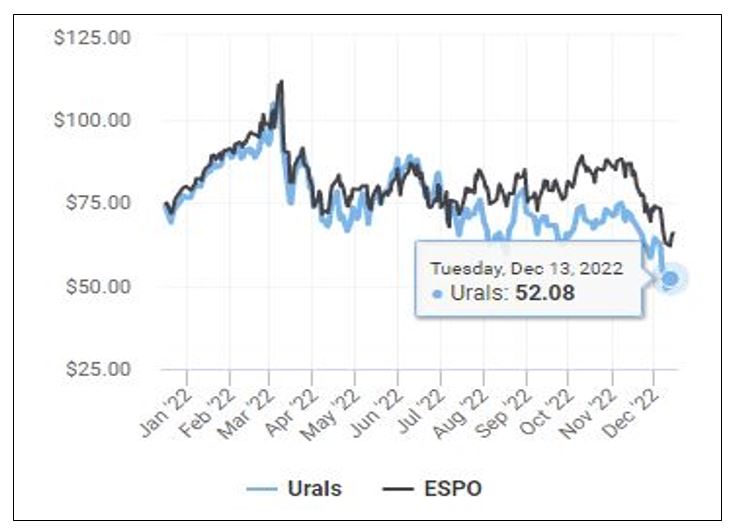

Russia is the world’s second largest producer of crude oil and has stated that it will not sell energy supplies to countries involved in the price cap. Some energy analysts feared that Russia could be forced to cut its oil output if it fails to find alternative buyers of its crude. However, at USD60 a barrel, some analysts have said the cap is too high to have much effect as Russia is already selling most of its crude at a similar price. The two main types of crude oil Russia exports are the Urals and the East Siberia-Pacific Ocean (ESPO) blend crude. As of 13 December 2022, Russian Urals crude oil price fell to around USD52.08 per barrel which is below the oil price cap and the ESPO oil price was around USD64.70 per barrel.

Urals and ESPO oil prices (USD/bbl.)

Impact on the Energy Market

Some energy analysts have warned that the G7 countries will need support from other major buyers like China and India if the cap is to be effective. These countries have increased their purchases of Russian oil following the invasion of Ukraine to benefit from discounted rates offered by Russia.

In December 2022, the Organization of Petroleum Exporting Countries (OPEC) left its forecasts for oil-supply growth to non-OPEC countries largely unchanged at 1.9 million barrels per day in 2022 and 1.5 million barrels per day in 2023. They also decided that a two million barrel per day cut in output agreed in October 2022 for implementation from November 2022 will at least for now, remain in place until the end of 2023. This decision was based on OPEC’s concerns about the health of global oil demand given economic headwinds, geopolitical tensions and China’s Covid-19 restrictions.

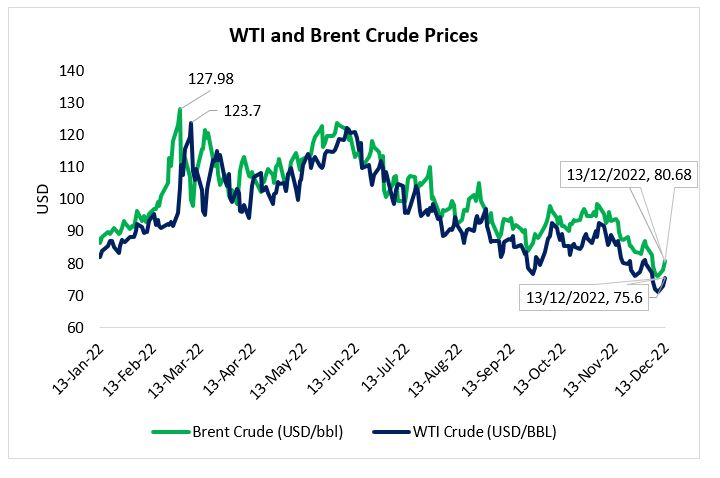

Following Russia’s invasion of Ukraine, oil prices trended up with WTI oil prices reaching as high as USD123.7 per barrel and Brent oil prices reaching as high as USD127.98 per barrel. Oil prices have since trended down even with the implementation of the oil price cap on Russia. As of 13 December 2022, WTI oil price was USD75.6 per barrel, a 38.8% decline from the highs experienced in March 2022.

What to expect going forward

Russia is expected to lose access to most of the European market as a result of a ban implemented in early December. This forces Russia to search for buyers for about 800,000 barrels of crude each day. Finding new markets for the excess supply will be difficult if Russian producers lose access to the G7 countries’ shipping, insurance and banking systems. They may also face challenges if they refuse to abide by the price cap of USD60. According to the Wall Street Journal, producers in Russia may most likely try to use tankers that previously moved sanctioned Iranian crude, known in the industry as the shadow fleet.

The Energy Information Administration (EIA) anticipated that most of Russia’s crude oil exports that will no longer go to Europe will find a destination elsewhere. However, they expect Russia’s oil production will continue to decline in 2023, largely because a number of countries will decrease their imports of crude oil and petroleum products from Russia. Despite the recent drop in crude oil prices, the EIA expects that falling global inventories of oil in early 2023 will push oil prices back up by the beginning of the second quarter of 2023.

Given the volatility in the global energy market with the sanctions placed on Russia, investors can reduce their risk by diversifying their portfolio across regions, sectors and asset classes.

DISCLAIMER

First Citizens Bank Limited (hereinafter “the Bank”) has prepared this report which is provided for informational purposes only and without any obligation, whether contractual or otherwise. The content of the report is subject to change without any prior notice. All opinions and estimates in the report constitute the author’s own judgment as at the date of the report. All information contained in the report that has been obtained or arrived at from sources which the Bank believes to be reliable in good faith but the Bank disclaims any warranty, express or implied, as to the accuracy, timeliness, completeness of the information given or the assessments made in the report and opinions expressed in the report may change without notice. The Bank disclaims any and all warranties, express or implied, including without limitation warranties of satisfactory quality and fitness for a particular purpose with respect to the information contained in the report. This report does not constitute nor is it intended as a solicitation, an offer, a recommendation to buy, hold, or sell any securities, products, service, investment or a recommendation to participate in any particular trading scheme discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. The information in this report is not intended, in part or in whole, as financial advice. The information in this report shall not be used as part of any prospectus, offering memorandum or other disclosure ascribable to any issuer of securities. The use of the information in this report for the purpose of or with the effect of incorporating any such information into any disclosure intended for any investor or potential investor is not authorized.

DISCLOSURE

We, First Citizens Bank Limited hereby state that (1) the views expressed in this Research report reflect our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.